Official Promissory Note Form for the State of West Virginia

In the picturesque landscapes of West Virginia, navigating financial transactions with clarity and security is paramount, especially when it involves lending or borrowing money. The West Virginia Promissory Note form serves as a critical tool in these circumstances, offering a structured and legally binding agreement between parties. This document not just outlines the amount of money borrowed and the repayment terms, including interest rates and payment schedules, but also acts as a tangible reassurance to the lender that the borrower is committed to repaying the loan as agreed. Moreover, it simplifies the legal process in the unfortunate event of a dispute, ensuring both parties have a clear understanding of their obligations. For residents of West Virginia looking to secure or provide a loan, familiarizing oneself with the nuances of this form is a step towards fostering trust and ensuring a smooth financial transaction.

West Virginia Promissory Note Example

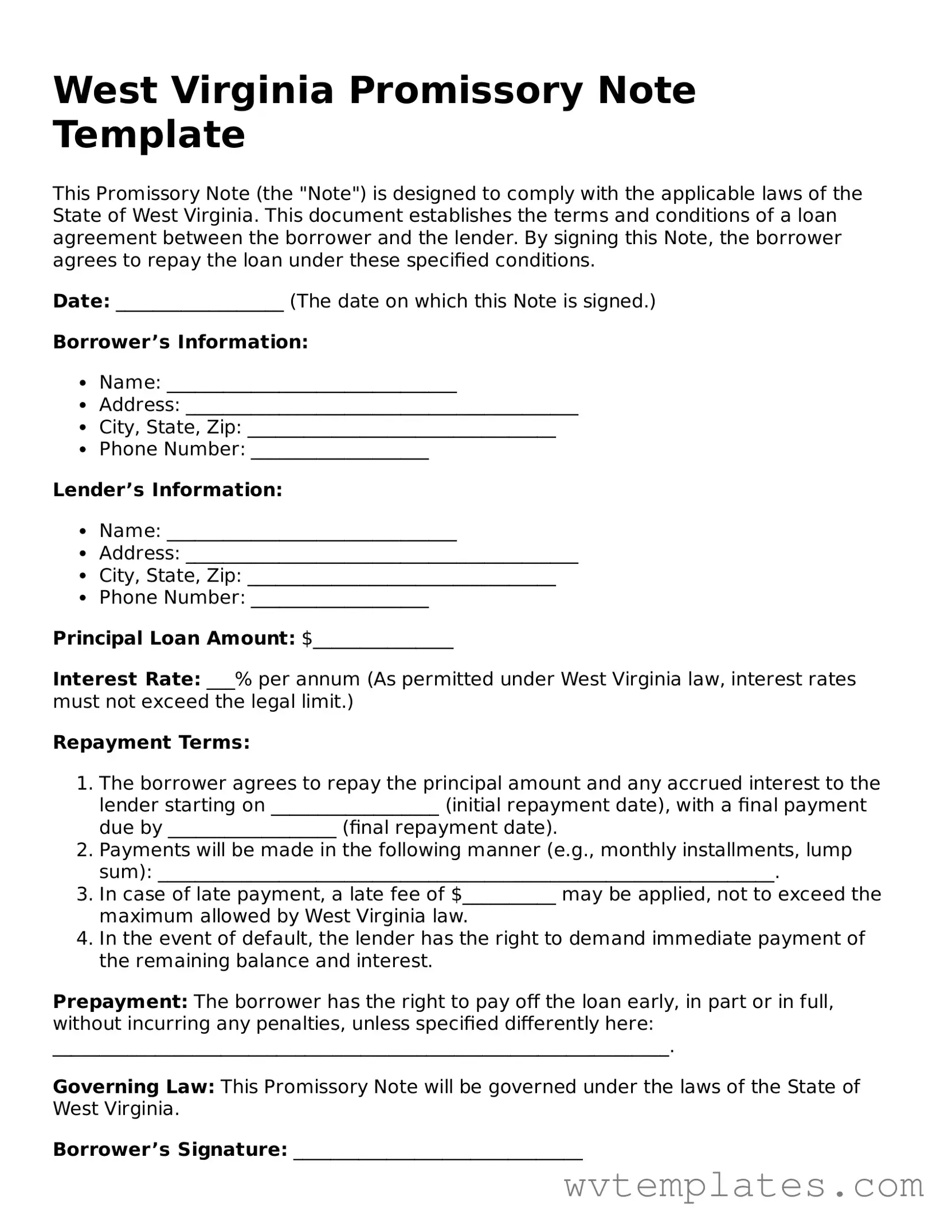

West Virginia Promissory Note Template

This Promissory Note (the "Note") is designed to comply with the applicable laws of the State of West Virginia. This document establishes the terms and conditions of a loan agreement between the borrower and the lender. By signing this Note, the borrower agrees to repay the loan under these specified conditions.

Date: __________________ (The date on which this Note is signed.)

Borrower’s Information:

- Name: _______________________________

- Address: __________________________________________

- City, State, Zip: _________________________________

- Phone Number: ___________________

Lender’s Information:

- Name: _______________________________

- Address: __________________________________________

- City, State, Zip: _________________________________

- Phone Number: ___________________

Principal Loan Amount: $_______________

Interest Rate: ___% per annum (As permitted under West Virginia law, interest rates must not exceed the legal limit.)

Repayment Terms:

- The borrower agrees to repay the principal amount and any accrued interest to the lender starting on __________________ (initial repayment date), with a final payment due by __________________ (final repayment date).

- Payments will be made in the following manner (e.g., monthly installments, lump sum): __________________________________________________________________.

- In case of late payment, a late fee of $__________ may be applied, not to exceed the maximum allowed by West Virginia law.

- In the event of default, the lender has the right to demand immediate payment of the remaining balance and interest.

Prepayment: The borrower has the right to pay off the loan early, in part or in full, without incurring any penalties, unless specified differently here: __________________________________________________________________.

Governing Law: This Promissory Note will be governed under the laws of the State of West Virginia.

Borrower’s Signature: _______________________________

Lender’s Signature: _______________________________

Witness (if required): _______________________________

This Promissory Note confirms the understanding and agreement between the borrower and the lender. It serves as a legal document evidencing the borrower's obligation to repay the loan as described above. Both parties should keep a copy of this Note for their records.

PDF Attributes

| Fact Number | \tDetail |

|---|---|

| 1 | \tWest Virginia promissory notes are legal agreements used for the borrowing and lending of money within the state. |

| 2 | \tThese notes can be categorized into two types: secured and unsecured. Secured promissory notes require collateral, while unsecured notes do not. |

| 3 | \tInterest rates on these notes must comply with West Virginia's usury laws to avoid being considered predatory. |

| 4 | \tThe legal maximum interest rate, unless specified otherwise in a contract, is determined by West Virginia law. |

| 5 | \tFor a promissory note to be considered valid in West Virginia, it must include the amount of money lent, interest rate, repayment schedule, and signatures of both the borrower and lender. |

| 6 | \tThe West Virginia Uniform Commercial Code (UCC) applies to transactions involving promissory notes, providing a framework for their enforcement and interpretation. |

| 7 | \tIn the event of default, West Virginia law outlines specific remedies and actions lenders may take to recover owed funds, emphasizing the need for a clear definition of "default" within the note itself. |

Guide to Filling Out West Virginia Promissory Note

When it comes to legal paperwork, accuracy and attention to detail are crucial, particularly with forms like the West Virginia Promissory Note. This document is a formal promise of repayment from a borrower to a lender, setting the terms under which a loan will be repaid. Filling it out correctly ensures that both parties clearly understand their obligations. Follow these steps meticulously to complete the form properly.

- Begin by entering the date on which the Promissory Note is being executed, at the top of the document.

- Write the full legal name of the borrower, followed by their full address, including city, state, and zip code.

- Enter the full legal name of the lender, along with their complete address, ensuring consistency with the details provided for the borrower.

- Specify the principal amount of the loan in US dollars.

- Detail the interest rate per annum that applies to the principal amount, ensuring it complies with West Virginia's applicable laws.

- Choose the method of repayment: lump sum, installments, or upon demand. Clearly outline the details of the chosen repayment method, including the due date for a lump sum or the schedule for installments.

- If applicable, include any agreed-upon security or collateral that the borrower is providing to secure the loan.

- Both the borrower and the lender must sign and print their names at the bottom of the form, making the document legally binding. Ensure the signatures are witnessed, if required by the state law.

- Date the signatures to confirm when the agreement was signed.

- Lastly, if the document requires notarization, make sure it is presented before a Notary Public for official notarization.

Once the West Virginia Promissory Note is fully completed and signed by all parties involved, it becomes a legally binding agreement that outlines the loan's terms and conditions. It's important for both the borrower and the lender to keep a copy of this document for their records. This ensures that all parties have a reference to the agreed-upon details of the loan, should any questions arise during the repayment period.

Things You Should Know About West Virginia Promissory Note

What is a West Virginia Promissory Note?

A West Virginia Promissory Note is a legal document where a borrower promises to repay a loan to a lender according to agreed terms. This note includes important details such as the loan amount, interest rate, repayment schedule, and any collateral securing the loan. It serves as a formal commitment by the borrower and is enforceable under West Virginia law.

Do I need to notarize my West Virginia Promissory Note?

No, notarization is not required for a West Virginia Promissory Note to be legally valid. However, having the note notarized can add an extra layer of security, proving that the signatures on the document are genuine. This could be helpful if there's ever a dispute about the note's authenticity.

Can I charge any interest rate on a loan in West Virginia?

West Virginia law specifies maximum interest rates that can be charged. The legal limit for personal loans is generally 6% per annum if not specified in the agreement. However, parties can agree to a higher rate, up to 8%, if it's clearly stated in the promissory note. Charging interest above these rates could result in penalties, including being charged with usury, which is illegal.

What happens if the borrower fails to repay the loan as agreed?

If a borrower fails to repay the loan according to the terms of the promissory note, the lender has the legal right to pursue collection. This could involve initiating a lawsuit to recover the outstanding debt. Additionally, if the promissory note is secured by collateral, the lender may have the right to seize that collateral to satisfy the debt.

Is it required to have witnesses when signing a West Virginia Promissory Note?

While West Virginia law does not specifically require witnesses for the signing of a promissory note, having at least one witness can increase the document's credibility. Witnesses can provide verifiable accounts of the agreement, making it easier to enforce the note's terms if there's a dispute. Nonetheless, the most important aspect for legal enforceability is the clear consent and signature of both the borrower and the lender.

Common mistakes

Filling out a West Virginia Promissory Note form properly is crucial for ensuring the agreement is legally binding and enforceable. Unfortunately, people often make several common mistakes during this process, which can lead to disputes or legal challenges down the line. Learning about these errors in advance can help parties avoid them and secure their financial arrangement more effectively.

- Not Including Specific Terms About Interest Rates: One of the most frequent oversights is failing to clearly state the interest rate. It's vital to specify not just the rate but also its accrimation method and frequency. Without this detail, the enforceability of the promissory note may be compromised, and it might not comply with state usury laws.

- Omitting Key Details About the Parties Involved: Another common error is not properly identifying all parties involved by their full legal names and addresses. This omission can create confusion about who is obligated to repay the loan and under what circumstances, making the document difficult to enforce.

- Misunderstanding the Legal Requirements: The legal requirements for a promissory note in West Virginia may differ from other jurisdictions. Some individuals neglect to review state-specific laws, leading to the creation of a document that doesn’t meet all legal standards in West Virginia, such as the necessary witness or notarization procedures.

- Failure to Define the Repayment Schedule: Clearly outlining how and when the loan will be repaid is essential. This includes setting precise dates for payments and, if applicable, specifying any grace periods for late payments. Without this information, it's difficult to enforce the terms of repayment, and misunderstandings can easily arise.

- Forgetting to Address Default Terms: What happens in the event of a default is often overlooked. Defining the consequences, including any late fees, accelerations of the debt, or legal actions, is critical. Without this, recovering the owed amount in case of non-payment becomes more complicated.

- Ignoring the Need for Witness or Notarization: While not always mandatory, having the promissory note witnessed or notarized can add an extra layer of authenticity and may be required for certain amounts. Failing to include this can challenge the document's legitimacy and enforceability.

Carefully filling out a promissory note and avoiding these mistakes not only helps in safeguarding the interests of both the lender and the borrower but also ensures the ease of enforcing the document. It is often beneficial to seek legal advice or assistance when drafting or reviewing a promissory note to ensure all legal requirements are met and the document is free from errors that could lead to future disputes.

Documents used along the form

When entering into a loan agreement in West Virginia, a Promissory Note form is a vital document, but it seldom stands alone. To ensure a comprehensive and secure transaction, several other documents should accompany it. These complementary forms fortify the agreement, provide legal security, and help to clarify the terms and expectations of all parties involved. Below is a list of documents that are frequently used alongside the West Virginia Promissory Note form.

- Loan Agreement: This document outlines the full terms and conditions of the loan, including interest rates, repayment schedule, and the obligations of both parties. It acts as the main agreement into which the promissory note ties.

- Security Agreement: If the loan is secured, a Security Agreement specifies the collateral held against the loan. This document is essential for detailing what is at stake should the borrower default on the loan.

- Mortgage Agreement: In real estate transactions, a Mortgage Agreement is used alongside a promissory note to secure the loan against the property being purchased.

- Deed of Trust: Similar to a Mortgage Agreement, a Deed of Trust involves a third party who holds the title of the property until the loan is paid in full. This is another form of security for real estate loans.

- Guaranty: This document is a pledge by a third party to repay the loan if the original borrower fails to do so, adding an extra layer of security for the lender.

- Amendment Agreement: Should the terms of the original loan agreement change, an Amendment Agreement is used to document these changes formally.

- Release of Liability: Once the loan is fully repaid, a Release of Liability verifies that the borrower has fulfilled their obligations and releases them from further responsibility.

- Late Payment Notice: If the borrower fails to make a payment on time, this document formally notifies them of the missed payment and any applicable late fees.

- Default Notice: This notice is a formal declaration from the lender that the borrower has defaulted on their loan, outlining any potential legal actions and consequences.

In conclusion, while the Promissory Note serves as the foundation of a loan transaction, these associated documents play crucial roles in detailing the agreement's terms, securing the loan, and ensuring legal protections for both lender and borrower. Ensuring all necessary paperwork is in order can prevent misunderstandings and legal disputes, safeguarding the financial interests of all parties involved.

Similar forms

The West Virginia Promissory Note form shares similarities with the Mortgage Agreement, primarily in the way both outline the terms of a loan. Like a promissory note, a mortgage agreement serves as a vow by the borrower to repay a sum of money borrowed to purchase property or real estate. Both documents detail the loan amount, interest rate, repayment schedule, and the consequences of default. However, the mortgage agreement also secures the loan with the property itself, offering the lender legal recourse to foreclose on the property if the borrower fails to meet their repayment obligations.

Similarly, the Loan Agreement is another document closely related to the West Virginia Promissory Note. Both serve the purpose of recording the details of a loan between two parties, including the loan amount, repayment conditions, and interest rates. The distinction primarily lies in the complexity and formality; loan agreements often entail more detailed provisions concerning the obligations of both lender and borrower and are typically used for more substantial sums and formal lending situations, whereas promissory notes are simpler, more concise documents.

The IOU (I Owe You) document is a less formal cousin of the promissory note. It simply acknowledges that a debt exists and specifies who owes whom, but lacks detailed terms of repayment, interest rates, and deadlines that you would find in a promissory note. An IOU is more informal and might not hold up as well in court, whereas a promissory note is designed to be a legally binding agreement, providing more security and clarity for both parties involved.

The Student Loan Agreement shares a particular purpose with the promissory note in the context of borrowing money for education. Both documents spell out the amount borrowed, the interest rate, and repayment terms. However, student loan agreements often come with specific conditions related to the borrower's educational status, potential deferment periods, and forgiveness options that are not typically part of a generic promissory note.

Equity Lines of Credit agreements bear resemblance to promissory notes in that they establish an agreement to borrow funds up to a certain limit, detail repayment obligations, and state the interest rate. Nevertheless, equity lines of credit are revocable and can be drawn upon repeatedly up to the credit limit, contrasting with promissory notes which specify a fixed loan amount to be repaid over a defined period.

The Personal Guarantee is a document that is often used in conjunction with promissory notes, especially in business lending. It is a legal commitment by an individual (usually a business owner) to repay a loan if the original borrower defaults. While the promissory note details the terms of the loan itself, a personal guarantee provides additional security to the lender by holding another party personally liable if the terms of the note are not met.

The Bill of Sale is akin to a promissory note in the way that both can signify the transfer of property or obligation from one party to another. However, a bill of sale is typically used to document the transfer of ownership of goods or assets, often with the full payment made at the time of transfer. In contrast, a promissory note outlines a promise to pay at a future date, frequently without an immediate exchange of tangible property.

Payment Plans are related to promissory notes through their shared focus on detailing the repayment terms of a debt. Both layout how a borrower will repay the lender over time, including the payment schedule and amounts. The difference often lies in the flexibility; payment plans can be adjusted or renegotiated more freely, while promissory notes usually outline a fixed agreement that is less susceptible to change without drafting a new note.

Finally, the Debt Settlement Agreement is similar to a promissory note in that it involves a form of debt repayment. However, a debt settlement agreement is specifically used to renegotiate terms of an outstanding debt, often allowing the borrower to pay less than the original amount owed. This contrasts with promissory notes, which clearly state the borrower's obligation to repay the full amount plus any agreed-interest rates and fees.

Dos and Don'ts

When filling out the West Virginia Promissory Note form, there are specific actions that should be taken to ensure the document is legally sound and effectively protects the interests of both parties involved. Equally, there are actions you should avoid to prevent complications or legal issues arising from this financial agreement.

Things You Should Do:

- Ensure all involved parties are clearly identified by their full legal names, including the lender, borrower, and any co-signers, to avoid any ambiguity regarding the parties' identities.

- Clearly specify the loan amount in words and numbers to prevent any misunderstandings about the loan size.

- Detail the repayment schedule, including due dates, interest rates, and any late fees, to set clear expectations about the loan's repayment.

- Include signatures from all parties involved, and consider having the document notarized to add an additional layer of authenticity and enforceability.

Things You Shouldn't Do:

- Leave any sections blank, as incomplete information can lead to disputes or a failure of the agreement to be legally binding.

- Sign the document without fully understanding every term and condition, as this could lead to agreeing to unfavorable terms unknowingly.

- Forget to specify whether the note is secured or unsecured. Failing to clarify this could affect the lender's options for recourse if the borrower defaults on the loan.

- Ignore state laws that may impact the promissory note. West Virginia has specific regulations that govern the execution of promissory notes, and non-compliance could invalidate the agreement.

Misconceptions

When it comes to drafting or understanding a West Virginia Promissory Note, it's easy to fall into the trap of misconceptions. This financial document, which promises that a borrower will repay a sum of money to a lender, is surrounded by a number of misunderstandings that can complicate its use. Let's debunk some of these misconceptions to ensure that you're on the right track.

- It Needs to Be Extremely Detailed: One common misconception is that a Promissory Note in West Virginia, or anywhere else for that matter, requires an overwhelming amount of detail to be valid. While it is important to include crucial elements like the amount borrowed, the interest rate, repayment schedule, and both parties' information, adding excessive detail beyond what is necessary can sometimes create confusion rather than clarity.

- Any Form Will Do: Simply pulling a generic promissory note form from the internet and filling in the blanks might seem like an easy solution, but it may not meet all legal requirements specific to West Virginia. State-specific legal nuances can mean the difference between enforceability and a document that holds no weight in legal proceedings.

- No Need for a Witness: Many people believe that as long as both parties sign the promissory note, it's good to go. However, having a witness sign or even getting the document notarized can add an extra layer of authenticity and protection, particularly in disputes over the validity of signatures.

- Interest Rates Are Optional: While not all promissory notes include interest rates, failing to specify one in a loan agreement could lead to misunderstandings or legal complications, especially if there's a disagreement about implied interest. Furthermore, West Virginia has laws governing the maximum allowable interest rates, and failing to adhere to these can void the interest terms.

- They're Only for Banks and Large Financial Transactions: This is a classic misunderstanding. Promissory notes can be used for a variety of lending situations, not just those involving banks or large sums of money. They're a handy tool for personal loans between family members or friends, as well as for more formal financial transactions.

- Signing Equals Immediate Legal Obligation: While signing a promissory note does create a legal obligation, the specifics of the obligation, such as start dates for repayment or conditions precedent (actions that must happen before the promissory note takes effect), can significantly alter when that obligation truly begins.

- Oral Agreements Are Just as Binding: While oral contracts can be legally binding, a written promissory note is far easier to enforce in court. The clarity that comes with a written agreement, detailing the exact terms and conditions, can prevent many disputes before they start.

- A Promissory Note is the Same as a Loan Agreement: Although they both relate to borrowing and lending money, a promissory note is a simpler document that outlines the promise to pay back a sum of money. A loan agreement is typically more comprehensive, covering more extensive terms of the loan, including collateral, covenants, and default terms. Both can serve important roles, but they are not interchangeable.

Clarifying these misconceptions about West Virginia Promissory Notes ensures that both lenders and borrowers understand their rights and obligations, paving the way for smoother financial transactions and relationships. Armed with the right information, you can navigate the complexities of promissory notes with confidence.

Key takeaways

Filling out and using the West Virginia Promissory Note form involves several key considerations to ensure clarity, legality, and enforceability. With attention to detail, individuals can successfully navigate the process of creating a promissory note that meets their needs. Below are eight key takeaways to guide you through this process:

- The amount borrowed must be clearly stated in the West Virginia Promissory Note form. It’s crucial to spell out the total amount of money being loaned to avoid any confusion or misunderstandings.

- Interest rates should comply with West Virginia’s legal requirements. Ensure you understand the maximum rate allowed to avoid charging illegal interest, which could void the note.

- Clearly outline repayment terms, including the repayment schedule, due dates, and any other conditions related to how the borrower should repay the loan. This helps both parties understand the expected timeline for repayment.

- Include information about late fees and penalties for missed payments. These details help enforce the note and provide clear consequences for failure to meet the agreed-upon repayment terms.

- The promissory note must be signed by both the borrower and the lender. Signatures legally bind both parties to the agreement and confirm their acknowledgment and consent to the terms outlined.

- Clearly identify the parties involved, using full names and addresses for the borrower and the lender. This clarifies who is obligated to repay the loan and to whom the loan must be repaid.

- If collateral is involved, describe the collateral detailed in the agreement. This secures the loan and should be adequately described so there’s no ambiguity about what is being used as security for the loan.

- Consider having the note notarized or witnessed to further authenticate the document. While not always a requirement, this step can add a layer of verification and help protect both parties.

Other Popular West Virginia Forms

How to Get Financial Power of Attorney - Designate an agent to legally handle specific responsibilities for your child, ensuring their continued wellbeing.

West Virginia Marital Separation Contract - It enables couples to manage the division of shared pets, ensuring that the companionship and care of animals are taken into consideration.