Free West Virginia Cd 3 Form

Embarking on the journey to resolve tax liabilities with the state can often be a daunting task for many taxpayers, yet West Virginia’s Offer in Compromise Form CD-3 (Revised 4/05) stands out as a beacon of hope for those seeking to find a manageable path through their financial obligations to the State Tax Department. Designed with the intent to offer a structured way to negotiate tax debts, this form encapsulates a process whereby taxpayers can propose to settle their state tax liabilities at an amount different from what is owed. The form meticulously outlines the necessary particulars, such as the identification of the taxpayer and any representative, the detailed breakdown of the tax periods, types, and the total amount owed, including interest and penalties. Moreover, it delineates the terms under which an offer can be made, including initial and subsequent payment arrangements, and the conditions tied to the State’s acceptance of the offer. Importantly, it underscores the taxpayers' commitment to adhere to future tax laws and filing requirements as a condition for compromise acceptance, placing a strong emphasis on financial disclosure and accountability on part of the taxpayer. By facilitating a dialogue between the taxpayer and the State Tax Commissioner, the CD-3 form essentially provides a structured yet flexible framework intended to serve the interests of both parties, aiming to foster compliance and resolution in the most equitable manner possible.

West Virginia Cd 3 Example

|

West Virginia State Tax Department |

|

|||

|

Offer In Compromise |

|

|

|

|

|

Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Names and Address of Taxpayer |

|

|

Taxpayer Representative |

|

|

|

|

|

Name: |

|

|

|

|

|

Address |

|

|

|

|

|

Phone |

|

|

Social Security or Tax Identification Number |

|

||||

|

|

|

|||

|

|

|

|

|

|

To: State Tax Commissioner |

|

Date |

Amount of Offer |

|

Total Liability |

|

|

|

$ |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

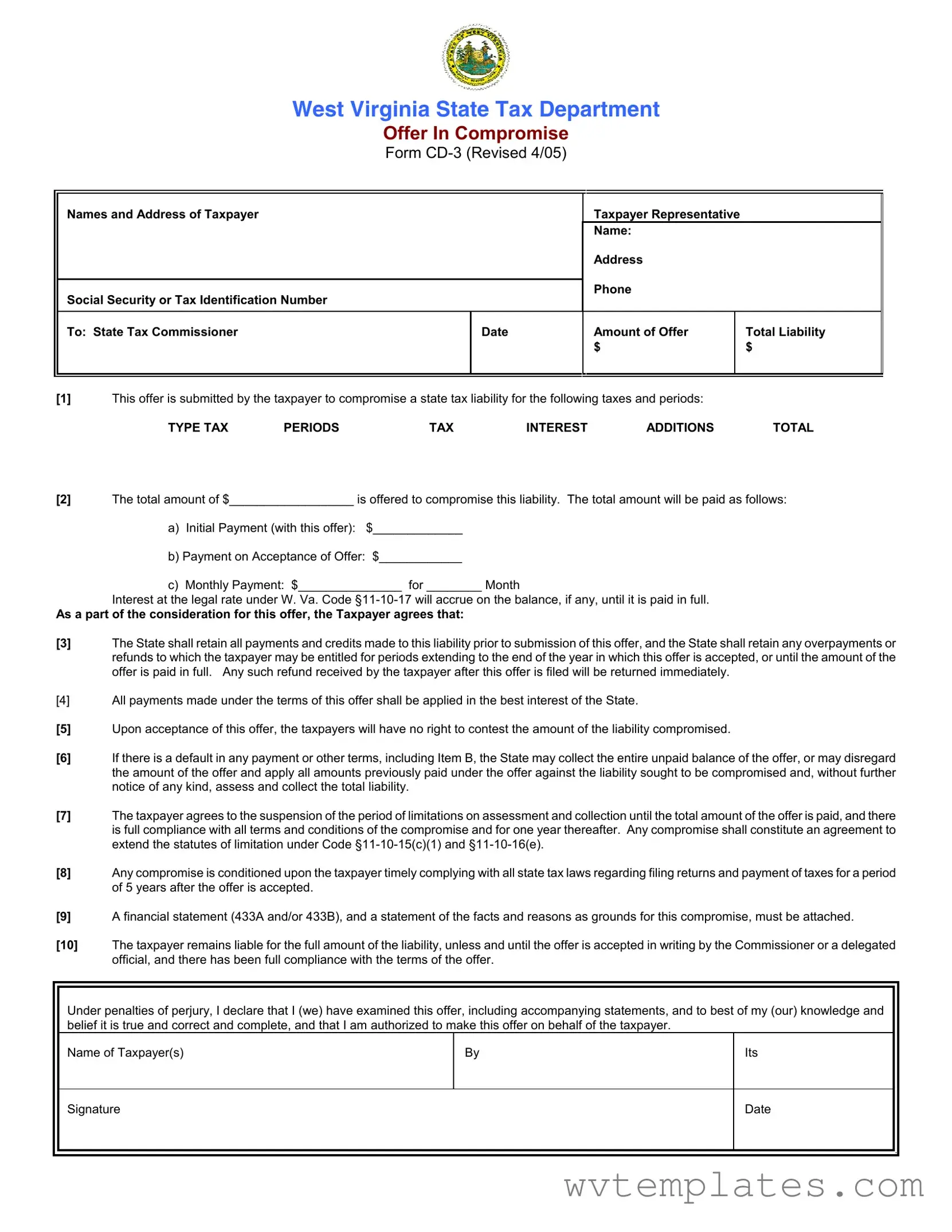

[1]This offer is submitted by the taxpayer to compromise a state tax liability for the following taxes and periods:

TYPE TAX |

PERIODS |

TAX |

INTEREST |

ADDITIONS |

TOTAL |

[2]The total amount of $__________________ is offered to compromise this liability. The total amount will be paid as follows:

a)Initial Payment (with this offer): $_____________

b)Payment on Acceptance of Offer: $____________

c)Monthly Payment: $_______________ for ________ Month

Interest at the legal rate under W. Va. Code

As a part of the consideration for this offer, the Taxpayer agrees that:

[3]The State shall retain all payments and credits made to this liability prior to submission of this offer, and the State shall retain any overpayments or refunds to which the taxpayer may be entitled for periods extending to the end of the year in which this offer is accepted, or until the amount of the offer is paid in full. Any such refund received by the taxpayer after this offer is filed will be returned immediately.

[4]All payments made under the terms of this offer shall be applied in the best interest of the State.

[5]Upon acceptance of this offer, the taxpayers will have no right to contest the amount of the liability compromised.

[6]If there is a default in any payment or other terms, including Item B, the State may collect the entire unpaid balance of the offer, or may disregard the amount of the offer and apply all amounts previously paid under the offer against the liability sought to be compromised and, without further notice of any kind, assess and collect the total liability.

[7]The taxpayer agrees to the suspension of the period of limitations on assessment and collection until the total amount of the offer is paid, and there is full compliance with all terms and conditions of the compromise and for one year thereafter. Any compromise shall constitute an agreement to extend the statutes of limitation under Code

[8]Any compromise is conditioned upon the taxpayer timely complying with all state tax laws regarding filing returns and payment of taxes for a period of 5 years after the offer is accepted.

[9]A financial statement (433A and/or 433B), and a statement of the facts and reasons as grounds for this compromise, must be attached.

[10]The taxpayer remains liable for the full amount of the liability, unless and until the offer is accepted in writing by the Commissioner or a delegated official, and there has been full compliance with the terms of the offer.

Under penalties of perjury, I declare that I (we) have examined this offer, including accompanying statements, and to best of my (our) knowledge and belief it is true and correct and complete, and that I am authorized to make this offer on behalf of the taxpayer.

Name of Taxpayer(s)

By

Its

Signature

Date

OFFERS IN COMPROMISE - INSTRUCTIONS

Authority

W. Va. Code

Reason for Compromise

We are allowed to compromise a liability for one or both of the following two (2) reasons: (1) doubt as to whether the taxpayer owes the liability; (2) doubt that we can collect the full amount of the liability. This form and instructions is only used in cases of doubt as to collectibility.

Policy

We will accept an offer in compromise when it is unlikely that we can collect the tax liability in full, and the amount offered reasonably reflects the amount we can collect. An offer in compromise is a legitimate alternative to declaring a case as currently not collectible or to a

The success of the compromise will be assured only if taxpayers make adequate compromise proposals consistent with their ability to pay the State. Taxpayers are expected to provide reasonable documentation to verify their ability to pay. The goal is a compromise which is in the best interest of both the taxpayer and the State. Where an offer in compromise appears to be a workable solution, the employee assigned the case will discuss the compromise with the taxpayer and, when necessary, assist in preparing the required forms. The taxpayer will be responsible for making the first offer for compromise.

Practical Consideration

It is the taxpayer's responsibility to show us why it would be in our best interest to accept your proposal. When we consider your offer we ask the following questions: (1) Could we collect the amount owed through liquidation of your assets or through an installment agreement? (2) Could we collect more from your assets and future income than is offered? (3) Would collection in the future result in more payment than is offered? (4) Would the public believe that the acceptance of your offer was a reasonable action?

The fact that you have no assets or income at this time from which the State could collect the liability does not mean that the State should simply accept any offer because it is all we can collect now. It would generally be better for us to reject a nominal amount and wait to see what collection potential would arise during the remainder of our

Additional Consideration

We believe that you benefit if we accept your offer because you can manage your finances without the burden of a tax liability. Therefore, we may require either: (1) A written agreement that will require you to pay a percentage of future earnings; and/or (2) A written agreement to give up present or future tax refunds.

Tax Compliance

(1)We will not accept your offer if you have not filed all tax returns. (2) We will also require that the taxpayer comply with all future filing and payment requirements. The terms of the offer require future compliance for a period of five (5) years.

Collection and Payments

The submission of an offer does not automatically suspend collection. If it appears the offer was filed to delay collection of the tax or that delay would hinder our ability to collect the tax, we will continue collection efforts. If you have agreed to make installment payments before you made the offer, those payments should continue.

Special Instructions for Offer in Compromise Form

(1)The Offer in Compromise form must be used to submit an offer. The form must be filed with the Compliance Division. If you have been working with a specific employee on your case, file the offer with that employee.

(2)Your full name, address and taxpayer identification number(s) must be entered at the top of the Offer form. If this is a joint liability (husband and wife) and both wish to make an offer, both names must be shown. If you are individually liable for a liability and are also jointly liable for another liability, and only one person is submitting an offer, only one offer must be submitted. If you are individually liable for one liability and jointly liable for another and both joint parties are submitting an offer, two (2) Offers must be submitted, one (1) for separate liability and one (1) for the joint liability.

(3)You must list all liabilities to be compromised in item (1). The types of tax, the periods, and the amounts must be specifically identified.

(4)The total amount you offer must be entered in item (2). The amount must not include any amount which has already been paid or collected on the liability. The amount submitted with the offer is entered in 2(a); the amount is to be paid on acceptance of the offer is entered in (2) (b) and any amount to be paid in installments, is entered in 2(c) in item 2. You should pay the amount of the offer in the shortest time possible, or we will reject your offer. Under no circumstances should the payment extend beyond two (2) years. Interest is due at the legal rate from the date of acceptance to the date of full payment.

(5)You must state in detail in item (9) why the State should accept your offer. Attach additional pages as necessary. Describes in detail why you believe the State cannot collect more than offered from your assets and your present and future income.

(6)The taxpayer(s) must sign and date the offer. If a person other than the taxpayer signs the offer, a power of attorney must be submitted with the offer.

(7)Form

What You Are Agreeing To

Please read the Offer in Compromise Form carefully so that you understand that you are agreeing to:

(1)The period for collection is suspended while the offer is pending, while any amount offered remains unpaid, and for one (1) year after all terms and conditions of the offer are fulfilled.

(2)You won't contest or appeal the amount of the liability if your offer is accepted.

(3)You give up of overpayments (refunds) for all tax periods through the year the offer is accepted, and until the amount of the offer is paid in full.

(4)The collection of the entire tax liability, if you do not comply with all the terms of the offer, i.e. payment, future compliance.

Form Specifications

| # | Fact |

|---|---|

| 1 | The form is used to propose a settlement to the West Virginia State Tax Department for less than the total amount owed in taxes. |

| 2 | Governing law for the Offer in Compromise includes W. Va. Code §11-10-5q(c), which authorizes the Tax Commissioner to compromise a tax liability. |

| 3 | Liabilities eligible for compromise include all taxes, penalties, interest, or additions to tax. |

| 4 | The offer requires a detailed listing of the specific types of tax, periods, and amounts being compromised. |

| 5 | Payment terms under the offer can include an initial payment, payment upon acceptance, and/or monthly payments, with legal interest rates applied to unpaid balances. |

| 6 | Acceptance of the offer means the taxpayer cannot contest the compromised amount and agrees to lose any refunds or overpayments for specified periods. |

| 7 | Failure to comply with the terms of the offer could result in the State collecting the full unpaid balance or dismissing the offer altogether. |

| 8 | The taxpayer must comply with all state tax laws and filing/payment requirements for five years following acceptance of the offer. |

| 9 | Submission of an Offer in Compromise does not automatically suspend collection actions; collection may continue if the offer is deemed to delay payment unduly. |

| 10 | A financial statement, Form 433-A for individuals and/or Form 433-B for businesses, must accompany the Offer in Compromise, detailing the taxpayer’s financial situation to justify the proposed compromise. |

Guide to Filling Out West Virginia Cd 3

Filling out the West Virginia CD-3 form is a necessary step for taxpayers seeking to compromise a state tax liability through an Offer in Compromise with the West Virginia State Tax Department. This process allows individuals to potentially settle tax debts for less than the full amount owed under certain circumstances. Careful attention to detail and completeness is crucial in preparing and submitting this form to ensure a smooth review process by tax officials. Following are the step-by-step instructions for filling out the form effectively.

- Start by entering the full names and address of the taxpayer(s) at the top section of the form.

- Provide the name, address, and phone number of the taxpayer representative, if applicable.

- Fill in the Social Security or Tax Identification Number associated with the tax liability.

- Specify the date on which the form is filled out.

- Enter the total amount of the offer you are submitting in the space provided. This amount should reflect what you realistically can pay, not the full amount owed.

- Under item (1) on the form, list the type of taxes, periods affected, and the amounts for tax, interest, additions, and the total liability you are seeking to compromise.

- In item (2), clearly outline the payment arrangement you are proposing, including:

- a) The initial payment you will make with this offer

- b) The payment amount upon acceptance of the offer

- c) Monthly payment amounts, including the duration (number of months) these payments will be made

- Understand that interest will continue to accrue at the legal rate until the offered amount is paid in full, as per West Virginia Code §11-10-17.

- Read through items (3) through (10), acknowledging the conditions associated with the offer, including the state’s retention of payments and credits, the application of payments in the state’s best interest, and the suspension of the limitation period on assessment and collection, among others.

- Complete a financial statement (Form 433A and/or 433B) and attach it to the offer, along with a detailed statement of the facts and reasons supporting the grounds for your compromise request.10. The taxpayer(s) must sign and date the offer at the bottom of the form. If submitting on behalf of a taxpayer, include a suitable Power of Attorney.

- Double-check the form for completeness and accuracy to ensure all necessary documentation and accompanying statements are attached before submission.

- Submit the completed form, along with Forms 433-A and/or 433-B and any other required documents, to the West Virginia State Tax Department’s Compliance Division.

After submitting the Offer in Compromise form and the required documentation, the West Virginia State Tax Department will review the offer. The process involves verifying the information provided, assessing the taxpayer's ability to pay, and determining whether accepting the offer is in the best interest of the state. Taxpayers are encouraged to continue making any previously agreed-upon payments while their offer is under review to avoid additional interest and penalties. It is essential to provide accurate and comprehensive information in the submission to facilitate a fair evaluation by the tax department.

Things You Should Know About West Virginia Cd 3

What is the West Virginia State Tax Department Offer in Compromise Form CD-3?

The West Virginia State Tax Department Offer in Compromise Form CD-3 is a document used by taxpayers to propose a lower payment than the total tax liability they owe. It's a way for individuals or businesses to reduce their tax debts when they cannot afford to pay the full amount.

Who can file a Form CD-3?

Individuals or businesses in West Virginia with outstanding tax liabilities they cannot fully pay may file the Form CD-3. However, they must provide substantial proof of their inability to pay the full amount and comply with specific requirements and conditions.

What are the reasons for submitting an Offer in Compromise?

An Offer in Compromise can be submitted for two main reasons: if there's doubt regarding the accuracy of the tax liability amount (doubt as to liability) or if there's doubt that the taxpayer can pay the full amount (doubt as to collectibility). This form specifically addresses cases where there's doubt as to collectibility.

What conditions must be met for the offer to be accepted?

For an offer to be considered, taxpayers must be current with all filing requirements and agree to comply with all state tax laws for five years after the acceptance of the offer. The proposed amount should also reflect the maximum amount the state believes it can collect within a reasonable period.

How should the offer amount be determined?

The offer amount should be determined based on the taxpayer's ability to pay. It includes considering assets, income, expenses, and future earning potential. The taxpayer must convincingly argue that the offer amount is the most the state can expect to collect.

Are there any payments required when submitting the form?

Yes, when submitting Form CD-3, taxpayers must include an initial payment. If the offer is accepted, further payments may be arranged as a lump sum or in monthly installments, as outlined in the offer's terms.

What happens if the offer is accepted?

Upon acceptance of the offer, taxpayers must comply with all terms, including future tax compliance for five years. The state retains all payments made toward the liability, and the taxpayer can no longer contest the compromised tax amount.

What happens if a taxpayer does not adhere to the offer's terms?

If a taxpayer defaults on any terms of the offer, such as missing payments, the state may revoke the offer and proceed to collect the full unpaid balance or apply any payments made towards the liability without considering the compromise.

How does the submission of Form CD-3 affect collection actions?

Submitting Form CD-3 does not automatically halt collection activities. If it's perceived that the offer is submitted solely to delay collection, or if delaying would jeopardize the state's ability to collect, collections efforts may continue. It is vital to maintain any agreed-upon installment payments while the offer is being considered.

Common mistakes

Filling out the West Virginia CD-3 form for an Offer in Compromise can be complex, and errors can result in delays or rejection of the offer. Below are ten common mistakes to avoid:

- Not fully completing the tax, interest, additions, and total amounts for each type of tax and period specified in the offer. This comprehensive breakdown is crucial for clarity and accuracy.

- Failing to include the correct total offer amount in section (2) or misrepresenting this figure. This total should reflect only what you are proposing to pay to settle the entire liability, excluding any amounts already paid.

- Incorrect or incomplete payment details, including initial, acceptance, and monthly payment amounts and terms. It’s vital to specify how and when you intend to pay the offer amount proposed.

- Neglecting to attach a required financial statement (Form 433A and/or 433B) and a detailed explanation of the facts and reasons justifying the offer. These documents are essential for the State to assess the feasibility of your offer.

- Failure to adhere to the special instructions for submitting the Offer in Compromise form, including proper filing with the Compliance Division or a specific employee if already in discussion.

- Omitting taxpayer identification number(s), full name, and address at the top of the form. These identifiers are fundamental for processing your offer.

- Submitting the offer without clarifying whether it concerns a joint liability or separate liabilities. Differentiation helps in accurately applying the offer to the correct tax liability.

- Forgetting to sign and date the offer or, if submitting on behalf of the taxpayer, failing to include a power of attorney. A valid signature grants authenticity and approval to proceed with the offer.

- Not providing a comprehensive explanation in item (9) as to why the State should accept your offer. A detailed justification is required to support the offered compromise’s validity.

- Overlooking the agreement terms regarding the suspension of the collection period and the renunciation of any right to dispute the compromised amount once the offer is accepted.

It is crucial to approach the form with attention to detail and provide all requested information precisely. Moreover, understanding and abiding by the terms set forth by the West Virginia State Tax Department can significantly increase the likelihood of a favorable outcome. For assistance, it may be beneficial to consult with a tax professional or legal advisor familiar with tax compromise processes.

Documents used along the form

When dealing with financial and tax matters, particularly when reaching an agreement with the state tax authorities in West Virginia, it is important to be fully prepared. The West Virginia State Tax Department Offer In Compromise Form CD-3 is a critical document for taxpayers seeking a compromise on their state tax liabilities. However, this form doesn't stand alone. There are several other forms and documents often used in conjunction with the CD-3 form to ensure a comprehensive approach to addressing tax liabilities. Understanding each of these documents can help taxpayers and their representatives navigate the complexities of tax resolution processes more effectively.

- Form 433-A (Collection Information Statement for Wage Earners and Self-Employed Individuals) - This form is crucial for individuals. It provides the tax authorities with detailed information about the taxpayer's financial situation, including income, expenses, assets, and liabilities.

- Form 433-B (Collection Information Statement for Businesses) - Similar to Form 433-A, but specifically designed for businesses, this form outlines the financial status of a business, detailing its assets, liabilities, monthly income, and expenditures.

- Power of Attorney and Declaration of Representative (Form WV-2848) - This document authorizes an individual, such as a tax professional, to represent a taxpayer before the West Virginia State Tax Department, allowing them to make inquiries, present documentation, and negotiate on the taxpayer's behalf.

- Installment Agreement Request (Form CD-5) - Taxpayers who cannot pay their liabilities in full may use this form to request a payment plan, breaking down the large sum into more manageable monthly payments.

- Financial Statement for Individuals (Form CD-1A) - Similar in function to Form 433-A, this document is used within the state to give a detailed account of an individual's financial situation, supporting their offer in compromise or payment plan proposal.

- Financial Statement for Businesses (Form CD-1B) - This form serves the same purpose as Form CD-1A but is tailored for businesses, providing a comprehensive overview of a business's financial health.

- Application for Tax Clearance Certificate (Form CCTA-1) - Businesses looking to dissolve, withdraw, or transfer their registration to another state must ensure they have no outstanding tax liabilities. This form helps confirm their tax status.

- Non-filer Compliance Form - Individuals or businesses not in compliance with filing requirements may need to submit this form as part of rectifying their tax situation before or during the offer in compromise process.

- Proof of Tax Payments - While not a formal form, providing documentation and receipts of previous tax payments or agreed upon installments underlines good faith efforts to comply with tax responsibilities, supporting the case for an offer in compromise.

Together, these forms and documents create a comprehensive package supporting an Offer in Compromise with the West Virginia State Tax Department. By preparing and submitting the appropriate documentation, individuals and businesses can effectively present their financial situation, negotiate terms, and work towards a resolution that is agreeable to both parties. It’s about making a complex process a bit more navigable, with the right form for every step of the journey.

Similar forms

The West Virginia CD-3 form for an Offer in Compromise shares similarities with the IRS Form 656, Offer in Compromise. Both forms are used by taxpayers to propose a settlement for less than the total amount owed in taxes, penalties, interest, and additional charges due to financial hardship or doubt as to liability. They require detailed financial information and a clear statement of reasons for the compromise, aiming to establish a realistic agreement between the taxpayer and the tax authority. Additionally, accepting these offers halts collections and waives the right to contest the agreed-upon amounts.

Another document closely related to the West Virginia CD-3 form is Form 433-A, Collection Information Statement for Individuals, and 433-B for Businesses. These forms are often required as attachments to the Offer in Compromise applications both at the federal (with IRS) and state levels. They provide a comprehensive snapshot of an individual's or business's financial situation, including asset, debt, income, and expense information. This detailed financial data helps the tax authorities determine the taxpayer's ability to pay the existing tax liability.

The Installment Agreement Request forms, such as IRS Form 9465, share similarities with the CD-3 form in that both provide taxpayers with alternatives to paying their liabilities in full due to financial challenges. While the CD-3 form is aimed at reducing the total tax bill, installment agreement forms are used to request a payment plan for the debt's balance. These forms recognize the taxpayers' financial limitations and seek to establish a manageable payment method without immediate full collection.

The Application for Taxpayer Assistance Order (ATAO), known at the federal level as IRS Form 911, similarly assists taxpayers facing significant hardships, though its function diverges slightly from the Offer in Compromise. The ATAO helps resolve specific issues with the tax authority that are not necessarily about reducing the tax bill but might include such actions in certain circumstances. Like the CD-3 form, it recognizes when a taxpayer's situation necessitates special consideration due to hardship or systemic issues in tax processing or collection.

State-specific Penalty Abatement Request forms serve a similar purpose to the Offer in Compromise in that they provide a means for taxpayers to reduce their tax liabilities, albeit more focused on penalties. They require similar justification for why the penalties should not apply, often including financial hardship or misunderstanding of tax laws. These forms, in spirit, acknowledge that circumstances can prevent taxpayers from full compliance and offer a remedial pathway.

The Innocent Spouse Relief Request forms, like the IRS Form 8857, also relate to the Offer in Compromise form by allowing taxpayers to seek relief from joint tax liabilities under specific conditions. While the purpose and details of these forms differ—focusing on relief due to the actions of a spouse or former spouse—they similarly provide taxpayers with an avenue to argue for a reduction or elimination of their tax liability based on fairness and equitable considerations.

Lastly, the Taxpayer Advocate Service Request forms, which enable taxpayers to seek help with tax issues that haven't been resolved through normal IRS channels, share an underlying principle with the Offer in Compromise form. Both are last-resort measures for when standard procedures have failed to resolve a taxpayer's problem. Although the Advocate Service focuses more on problem-solving and navigating the system, both mechanisms aim to offer relief and fairness to taxpayers struggling with their obligations.

Dos and Don'ts

When completing the West Virginia CD-3 form for an Offer in Compromise, it's important to navigate the process carefully to ensure your offer is considered. The following list provides guidance on what you should and shouldn't do during this process:

- Do: Provide complete and accurate information regarding your name, address, and taxpayer identification number(s) at the top of the form.

- Do: List all tax liabilities you wish to compromise, including the types of tax, the periods, and the amounts accurately.

- Do: Clearly state the total amount you're offering to compromise, excluding any amounts already paid towards the liability.

- Do: Attach a detailed explanation in item 9, explaining why the State should accept your offer, including documentation supporting your claim that the State cannot collect more than the offered amount from your assets and future income.

- Do: Include Form 433-A, Collection Information Statement for Individuals and/or Form 433-B, Collection Information Statement for Business, as required.

- Don't: Leave any sections incomplete. If a section does not apply, indicate with "N/A" (not applicable).

- Don't: Submit the form without making sure all necessary documentation is attached, including any required financial statements and a clear statement of facts and reasons for the compromise.

- Don't: Extend the payment of the offer beyond two years, as this could lead to rejection.

- Don't: Forget to sign and date the offer. If someone other than the taxpayer is signing, ensure that a power of attorney form is included.

By following these guidelines, you'll help ensure your Offer in Compromise is duly considered by the West Virginia State Tax Department. It's crucial to present a clear and compelling case that accurately reflects your financial situation and the reasons why the compromise is in both your and the State's best interest.

Misconceptions

Many taxpayers view the West Virginia CD-3 form, or the Offer in Compromise form, as a complex and sometimes misunderstood tool for dealing with tax debts. However, a clearer understanding of some common misconceptions can help demystify this form, making it a potentially valuable resource for those who are eligible. Let’s explore seven of these misconceptions:

- “The form is a way to eliminate tax debt easily.” Contrary to what some may believe, the Offer in Compromise is not an easy solution for erasing tax debt. Applicants must provide substantial evidence of their inability to pay the full amount owed, including detailed financial statements and documentation.

- “Any taxpayer can qualify for an Offer in Compromise.” In reality, eligibility for an Offer in Compromise is determined by specific criteria related to the taxpayer's financial ability to pay the tax owed. Not everyone will qualify, as the state seeks to ensure that taxpayers are truly unable to pay the full amount before accepting a lesser amount.

- “Offers in Compromise can be used for any tax debt.” This program is designated for state tax liabilities. It’s essential to understand which types of tax debts can be compromised, as not all are eligible under this particular relief option.

- “The Offer in Compromise process is quick.” The review process for an Offer in Compromise can be lengthy, requiring thorough evaluation of the provided documentation and the taxpayer’s financial situation. Patience is key, as the process can extend over several months.

- “The initial offer amount is non-negotiable.” In fact, the initial offer is not always the final word. The State Tax Department may negotiate the offer amount based on their assessment of the taxpayer’s ability to pay.

- “Once an offer is accepted, other tax obligations are suspended.” Taxpresents must continue to file and pay all tax obligations according to state laws even after an Offer in Compromise is accepted. Future compliance for a specified period is a condition of the agreement.

- “Submitting an Offer in Compromise form will automatically stop all collection activities.” Filing this form does not guarantee that collection efforts will cease. In some cases, collections may continue if it's believed the offer was submitted to deliberately delay collection efforts.

Understanding these misconceptions can significantly impact a taxpayer’s decision and approach when considering an Offer in Compromise with the West Virginia State Tax Department. It’s always recommended to consult with a tax professional to ensure that this course of action is appropriate and well-informed.

Key takeaways

When dealing with the West Virginia State Tax Department Offer in Compromise Form CD-3, it's crucial to understand several key aspects to ensure proper completion and submission:

- The purpose of Form CD-3 is to propose a compromise to the West Virginia State Tax Commissioner to settle state tax liabilities for less than the full amount owed.

- Applicants must clearly specify the type of taxes, the periods in question, and the total amounts including tax, interest, additions, and the total sum of liabilities intended for compromise.

- The form requires a detailed breakdown of the offer amount, including initial payment with the submission, amount to be paid upon acceptance of the offer, and subsequent monthly payments, if any, along with the interest that will accrue on any remaining balance.

- By submitting the offer, taxpayers agree that the State will retain any payments or credits made towards the liability before the offer's submission and any overpayments or refunds eligible until the offer's full payment is made or until the calendar year-end in which the offer is accepted.

- Acceptance of the offer by the State means the taxpayer cannot dispute the compromised liability amount, and if the taxpayer defaults on payments or other conditions, the State may enforce collection of the entire unpaid balance or disregard the offer.

- The offer includes a stipulation that the period of limitations on assessment and collection is suspended until the total offer amount is paid, all terms are fully complied with, and for one year thereafter.

- To be considered, the offer must be accompanied by a financial statement (Forms 433A and/or 433B), detailing the taxpayer's financial position, and a statement explaining why the compromise is justified, which includes the taxpayer's inability to pay the full liability.

- The completion and submission of the Form CD-3 require honesty and accuracy, with the taxpayer signing under penalty of perjury that all information provided is true, correct, and complete to the best of their knowledge.

Understanding these points and carefully filling out the Offer in Compromise Form CD-3 can significantly impact a taxpayer's ability to resolve outstanding tax liabilities with the West Virginia State Tax Department. It is also advisable for taxpayers to maintain compliance with all state tax laws, including filing and payment obligations, especially for the five years following acceptance of an offer.

Popular PDF Forms

West Virginia State Tax Department - Explore the comprehensive table of contents provided within the WV tax form packet for a smooth tax preparation process.

Wv Pas - Utilized in a wide range of settings, including nursing homes, rehabilitation centers, and other long-term care facilities.

Wv Abc - Overview of the licensing period validity and pro-rated fee information for applications submitted mid-year.