Free West Virginia Opt 1 Form

In a world where digital processes are increasingly becoming the norm, the West Virginia Opt 1 form presents an interesting deviation for those involved in the yearly ritual of income tax return preparation. Specifically designed for individuals using the services of tax preparers who, due to regulations, are generally required to file all West Virginia Income Tax returns electronically, this form serves as a bridge to the traditional paper filing. It comes into play when a taxpayer prefers not to submit their tax return via electronic means. By completing and signing the Opt 1 form, taxpayers can officially choose to have their return filed on paper, a choice that must be voluntarily made without any coaxing from the preparer. This option is not only a testament to the varied preferences among taxpayers but also highlights the importance of accommodating individual needs within the tax filing ecosystem. Moreover, the form carries stipulations for the tax preparer as well, who must retain the signed document for three years, ensuring accountability and compliance. This process not only respects the taxpayer's choice but also subtly underscores the evolving landscape of tax preparation, where electronic filing is the expectation but not the absolute rule. This level of flexibility provided to both taxpayers and preparers through the West Virginia Opt 1 form is crucial in a system that values accuracy, efficiency, and user comfort.

West Virginia Opt 1 Example

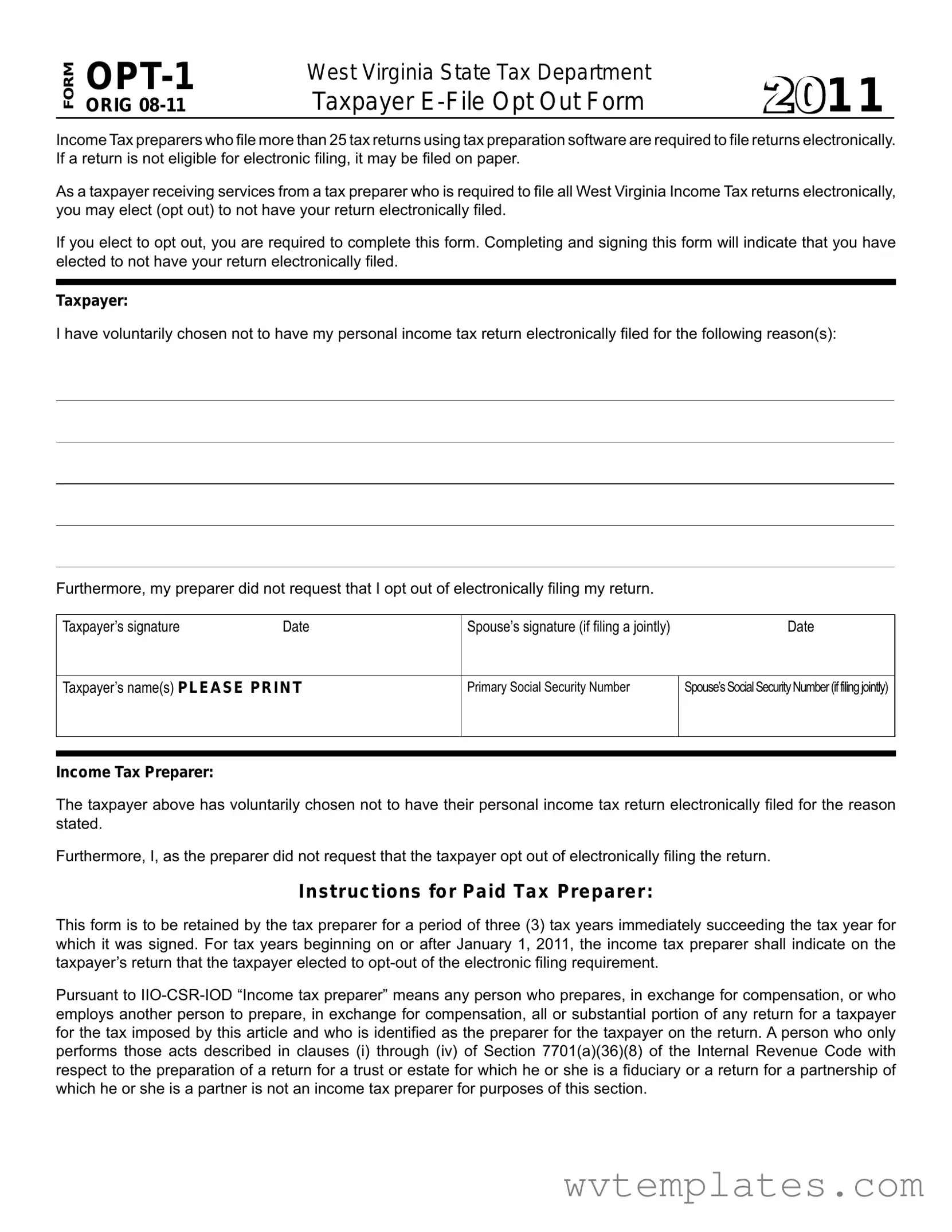

FORM

ORIG

West Virginia State Tax Department |

2 0 1 1 |

Taxpayer |

Income Tax preparers who ile more than 25 tax returns using tax preparation software are required to ile returns electronically. If a return is not eligible for electronic iling, it may be iled on paper.

As a taxpayer receiving services from a tax preparer who is required to ile all West Virginia Income Tax returns electronically, you may elect (opt out) to not have your return electronically iled.

If you elect to opt out, you are required to complete this form. Completing and signing this form will indicate that you have elected to not have your return electronically iled.

Taxpayer:

I have voluntarily chosen not to have my personal income tax return electronically iled for the following reason(s):

Furthermore, my preparer did not request that I opt out of electronically iling my return.

Taxpayer’s signature |

Date |

Spouse’s signature (if iling a jointly) |

Date |

Taxpayer’s name(s) PLEASE PRI N T

Primary Social Security Number

Spouse’s Social Security Number (if filing jointly)

Income Tax Preparer:

The taxpayer above has voluntarily chosen not to have their personal income tax return electronically iled for the reason stated.

Furthermore, I, as the preparer did not request that the taxpayer opt out of electronically iling the return.

I nst ruc t ions for Pa id Ta x Pre pa re r:

This form is to be retained by the tax preparer for a period of three (3) tax years immediately succeeding the tax year for which it was signed. For tax years beginning on or after January 1, 2011, the income tax preparer shall indicate on the taxpayer’s return that the taxpayer elected to

Pursuant to

Form Specifications

| Fact | Detail |

|---|---|

| Form Name and Number | West Virginia Opt 1 Form, FORM OPT-1 ORIG 08-11 |

| Purpose | To allow taxpayers to opt-out of having their tax return electronically filed by their tax preparer |

| Eligibility to File | Taxpayers receiving services from preparers required to file all West Virginia Income Tax returns electronically |

| Electronic Filing Requirement | Tax preparers who file more than 25 tax returns using tax preparation software are required to file returns electronically unless opted out by the taxpayer |

| Retention Period | Tax preparers must retain this form for three (3) tax years following the year it was signed |

| Governing Law(s) | Pursuant to IIO-CSR-IOD, part of the regulations governing taxation and income tax preparation in West Virginia |

| Special Instructions for Preparers | Upon a taxpayer opting out, the preparer must indicate on the taxpayer’s return that the taxpayer elected to opt-out of the electronic filing requirement |

Guide to Filling Out West Virginia Opt 1

When you're working with an income tax preparer in West Virginia, there's a specific procedure if you decide not to file your tax returns electronically, even though your preparer normally files electronically for all their clients. This might be a decision based on personal preference or specific circumstances. The West Virginia OPT-1 form is designed for this purpose. It allows you to officially opt-out of electronic filing. Here's how you can fill it out:

- At the top of the form, observe the section that reads "Taxpayer E-File Opt Out Form." It's important to note that this form is used for the year 2011 and beyond, for taxpayers who choose not to file electronically.

- Under the "Taxpayer" section, provide the reason(s) you have chosen not to file your personal income tax return electronically. Make sure to mention that the decision was made voluntarily and that your preparer did not influence you to opt out of electronic filing.

- Sign your name under "Taxpayer's signature" to validate the form. Make sure to include the date next to your signature.

- If you're filing jointly with a spouse, your spouse must also sign the form and date it under "Spouse’s signature (if filing a jointly)."

- Fill in your name(s) in the designated area. This should be printed clearly to avoid misunderstandings.

- Enter the "Primary Social Security Number" for yourself and, if applicable, your spouse’s Social Security Number in the spaces provided if you're filing jointly.

- In the "Income Tax Preparer" section, it is stated that you have voluntarily chosen not to e-file. Your preparer must acknowledge this by also confirming that they did not request you to opt out.

- The bottom section of the form provides instructions for paid tax preparers, indicating that this form should be retained for three (3) tax years following the year it was signed. It also outlines the preparer’s responsibility to indicate on the taxpayer’s return that they opted out of electronic filing.

Once completed, this form acts as an official record of your decision to opt-out of electronic filing for your West Virginia Income Tax return. Keep a copy for your records and make sure your tax preparer does the same. This ensures compliance with state requirements and verifies the choice made regarding the filing method.

Things You Should Know About West Virginia Opt 1

What is the purpose of the West Virginia OPT-1 Form?

The West Virginia OPT-1 Form is designed for taxpayers who choose not to have their personal income tax return filed electronically by their tax preparer. It is intended for use in scenarios where a tax preparer, who is generally required to file returns electronically for clients, is asked by a taxpayer to submit their return in a paper format instead. This form legally documents the taxpayer's choice to opt out of electronic filing.

Who needs to complete the West Virginia OPT-1 Form?

This form must be completed by taxpayers receiving services from a tax preparer mandated to file West Virginia Income Tax returns electronically but prefer their returns to be filed on paper. The taxpayer's deliberate choice not to electronically file their tax return is formally indicated by filling out and signing this form.

How does a taxpayer opt out of electronic filing using the OPT-1 form?

To opt out of electronic filing, a taxpayer must complete the OPT-1 form, providing a valid reason for choosing not to e-file their West Virginia Income Tax return. Both the taxpayer and, if filing jointly, their spouse must sign the form to validate their choice. This action informs both the tax preparer and the West Virginia State Tax Department of the taxpayer's decision to opt out of electronic filing.

What are the responsibilities of the tax preparer regarding the OPT-1 form?

Tax preparers are responsible for retaining the OPT-1 form for three tax years following the year it pertains to, as a record of the taxpayer's choice to opt out of electronic filing. They must also indicate on the taxpayer's return that the choice to opt out was made. This process ensures that there is formal documentation supporting the taxpayer's decision, should it need to be verified by the West Virginia State Tax Department in the future.

Common mistakes

Filling out forms can often feel straightforward until one encounters the complexities of legal and tax documents. The West Virginia Opt 1 form is a perfect example of a document that, while essential, can be tricky to navigate without making mistakes. Here are 10 common errors people tend to make on this form:

- Incorrectly printing names: The form clearly states that names should be printed. However, many individuals mistakenly use cursive or signatures where printed letters are required, leading to confusion and potential processing delays.

- Forgetting to list a reason for opting out: The form requires taxpayers to state why they've chosen not to file electronically. This step is often overlooked, rendering the form incomplete.

- Overlooking the spouse’s details: If filing jointly, the spouse’s signature is mandatory. It's common for this to be missed, especially if one spouse is handling the taxes.

- Omitting Social Security Numbers (SSNs): Both the taxpayer's and spouse’s SSNs are crucial. Failure to include these can result in the form not being processed.

- Ignoring the preparer’s section: The section meant for the Income Tax Preparer's acknowledgment is frequently left blank, which is a critical oversight.

- Not dating the signatures: Both the taxpayer and the spouse must date their signatures. This is a simple but frequently forgotten step.

- Misunderstanding the opt-out reasons: Taxpayers sometimes believe they need to provide extensive explanations for opting out, while simple, clear reasons are preferred.

- Tax preparer not indicating the opt-out on the return: It's the preparer's responsibility to mark the taxpayer’s return indicating the opt-out. Sometimes this is neglected, causing compliance issues.

- Improperly storing the form: Once completed, the form needs to be retained by the preparer for three tax years. Poor record-keeping can lead to issues if documentation is requested.

- Assuming a preparer's request to opt-out: The form specifies that the taxpayer’s decision to opt-out should be voluntary and not at the request of the preparer. This distinction is often misunderstood.

When filling out the West Virginia Opt 1 form, it is essential to approach the task with attention and diligence. Avoiding these common mistakes ensures a smoother process for both the taxpayer and the preparer. Emphasizing the importance of reading instructions carefully cannot be overstated - it is a crucial step toward accurate and compliant tax filing.

- Ensure names are printed clearly and legibly.

- Always remember to include valid reasons for opting out of electronic filing.

- Don't overlook the importance of including and correctly filling out your spouse's details if filing jointly.

- Double-check that all necessary signatures and dates are present on the form.

Remember, the goal is to provide accurate information that meets all requirements. Taking the time to review your entries can prevent unnecessary delays or issues with your tax filing. When in doubt, consulting a professional for advice or clarification on how to properly complete the form is a wise move.

Documents used along the form

When filing taxes in West Virginia, the West Virginia Opt 1 form is an important document for those who wish to opt out of electronic filing for their personal income tax returns. However, this is often just one of several documents and forms needed during the tax preparation and filing process. Understanding these additional documents can simplify the process and ensure compliance with all filing requirements.

- Form IT-140: This is the West Virginia Personal Income Tax Return form for residents. It is the primary form used to report income, deductions, and credits to the state.

- Form IT-140W: This Form is for calculating West Virginia withholding. It's essential for individuals who have had income tax withheld and need to reconcile the amount with their total tax liability.

- Schedule M: Modifications to Adjusted Gross Income. Taxpayers use this schedule to make certain adjustments to their federal adjusted gross income for West Virginia state tax purposes.

- Schedule L: Credit for Income Tax Paid to Another State. It's for taxpayers who must file in more than one state. This form helps avoid double taxation on the same income.

- Form IT-140ES: Estimated Tax for Individuals. This form is used by individuals to pay estimated taxes throughout the year, typically applicable for those who do not have sufficient withholding.

- Form IT-141: West Virginia Fiduciary Income Tax Return, required for estates or trusts earning income within the state.

- Form IT-210: Underpayment of Estimated Tax by Individuals. If taxpayers didn't pay enough in estimated taxes throughout the year, this form calculates the penalty owed.

- Form WV-8379: Injured Spouse Allocation. This form allows a spouse to claim their portion of a joint refund if it was (or is expected to be) applied against the other spouse's debts.

- Direct Deposit Authorization: Many opt for direct deposit for their refunds. While not a form exclusive to West Virginia, including a direct deposit authorization form with your tax return can expedite your refund.

Each of these forms and documents plays a critical role in the tax filing process, helping taxpayers to accurately report their income, claim eligible deductions and credits, and fulfill their tax obligations. Understanding when and how to use these documents, alongside the West Virginia Opt 1 form, can make the tax filing process smoother and more efficient.

Similar forms

The IRS Form 8948, "Preparer's Explanation for Not Filing Electronically," closely mirrors the West Virginia Opt 1 form. Both forms serve a similar purpose: they are used by taxpayers or their preparers to officially document why a tax return was not submitted electronically. The key similarity lies in their function to exempt the taxpayer from electronic filing mandates, provided they have valid reasons documented on the forms. Just like the Opt 1 form, Form 8948 is filled out and retained by the tax preparer as part of their records.

Form 4868, "Application for Automatic Extension of Time To File U.S. Individual Income Tax Return," although serving a different function, shares a procedural similarity with the West Virginia Opt 1 form. It allows taxpayers to extend the deadline for filing their income tax returns. While not about opting out of electronic filing, it showcases the broader system's flexibility in accommodating taxpayers' circumstances, a theme central to both documents. Each form must be completed and submitted according to specific requirements to be valid.

The Consent to Disclosure of Tax Information is another document that parallels the West Virginia Opt 1 form in that it involves a taxpayer's decision regarding the handling of their personal tax information. This document allows a taxpayer to authorize the sharing of their tax information with specified individuals or entities. Like the Opt 1 form, it emphasizes taxpayer consent and the importance of documenting choices related to tax filing and preparation processes.

A Power of Attorney and Declaration of Representative form is somewhat similar to the West Virginia Opt 1 form, in the aspect of designated actions on behalf of someone else regarding tax matters. Although it primarily appoints an individual to act in a representational capacity for tax affairs, including filing returns, it underlines the necessity of clear documentation when tax-related duties are delegated or decisions made that deviate from the norm, resonating with the Opt 1's focus on formally acknowledging a non-standard filing choice.

The Request for Copy of Tax Return form shares similarities with the Opt 1 form in the context of handling and processing sensitive tax-related documents. This form is necessary for individuals who need an official copy of their tax return for various reasons. Despite their different purposes, both forms play important roles in the administrative aspect of tax filing, emphasizing taxpayer agency and the need for formal requests or declarations in altering typical filing practices.

The IRS Form 8888, "Allocation of Refund (Including Savings Bond Purchases)," bears resemblance to the West Virginia Opt 1 form in that it involves directing the specifics of tax filing outcomes – in this case, how a refund is allocated. While Form 8888 deals with the dispersion of funds rather than the method of filing, it similarly requires taxpayers to make and document deliberate choices regarding their returns, showcasing the IRS's broader adaptability to individual needs and preferences.

Last, the Change of Address Form (Form 8822) for the IRS is akin to the West Virginia Opt 1 form in regards to facilitating taxpayer-initiated updates or adjustments outside of standard return filing. It allows taxpayers to inform the IRS of a change in address to ensure that they receive all correspondence. Although this form does not deal with electronic filing directly, it embodies the theme of taxpayer control over personal information and the necessity of submitting specific forms to enact changes within the tax system.

Dos and Don'ts

When filling out the West Virginia Opt 1 form, there are certain guidelines to adhere to, ensuring the process is both compliant and efficient. This form plays a critical role for taxpayers who choose not to submit their West Virginia Income Tax returns electronically, despite their tax preparer's obligations to file returns electronically if more than 25 tax returns are prepared using tax preparation software. Being aware of the do's and don'ts will help prevent any issues that could potentially arise from the incorrect filing of this form.

Do:

Ensure that all the required fields are completed with legible, accurate information. This includes the taxpayer's name(s), primary Social Security Number, and spouse’s Social Security Number (if filing jointly), alongside the signatures and dates from both the taxpayer and the spouse (if applicable).

Provide clear and specific reasons for choosing not to have the tax return electronically filed. This explanation helps in maintaining a transparent record and fulfilling the taxpayer's obligations.

Verify that the tax preparer has also signed the form acknowledging that you, as the taxpayer, have voluntarily chosen not to e-file your return for the stated reasons.

Retain a copy of this form for your records. As the form must be kept by the tax preparer for three tax years succeeding the tax year for which it was signed, it is prudent for you to also keep a copy for your personal records.

Don't:

Do not leave any of the form fields blank. Incomplete forms may result in non-compliance with the West Virginia State Tax Department's requirements for opting out of electronic filing.

Do not sign the form without thoroughly reviewing all the information provided, ensuring that it is correct and fully represents your decision to opt out.

Avoid submitting this form without first discussing your decision with your income tax preparer, as they need to acknowledge your choice and comply with their own set of requirements.

Do not ignore the requirement for the tax preparer to indicate on the taxpayer’s return that the taxpayer elected to opt out of the electronic filing requirement. Ensure this step is completed to maintain compliance with the West Virginia State Tax Department directives.

Misconceptions

There are several misconceptions about the West Virginia Opt 1 form, a document utilized by taxpayers to opt out of electronic filing of their state income tax returns. Understanding these misconceptions is essential for taxpayers and tax preparers alike to ensure compliance with state tax filing requirements.

Misconception 1: Completing the Opt 1 form automatically exempts the taxpayer from electronic filing with the IRS. While the Opt 1 form pertains to West Virginia state income tax returns, it does not impact federal tax return filing requirements. Taxpayers must adhere to separate processes for federal returns.

Misconception 2: Tax preparers can decide to file on paper for all their clients without needing to complete an Opt 1 form for each. Actually, the form must be filled out and signed by each taxpayer (or jointly if filing with a spouse) who chooses to opt out of electronic filing, highlighting the individual choice involved in this process.

Misconception 3: If a taxpayer opts out of electronic filing, their tax preparer is not required to keep a record of the Opt 1 form. On the contrary, tax preparers must retain the completed Opt 1 form for three tax years following the year it pertains to, ensuring that there is a record of the taxpayer's choice to opt out.

Misconception 4: The Opt 1 form is required for all taxpayers, regardless of how their return is prepared. This form is specifically for taxpayers whose preparers are mandated to file electronically because they file more than 25 tax returns using tax preparation software. It is designed for those who, for any reason, decide against electronic submission.

Misconception 5: Electronically filing a return is optional for tax preparers who file more than 25 returns annually. In reality, such preparers are required by law to file electronically unless the return is not eligible for electronic filing. The Opt 1 form allows taxpayers to opt out, but the default expectation is electronic filing.

Misconception 6: The Opt 1 form negates the need for a preparer to indicate on the taxpayer’s return that they opted out of electronic filing. Incorrect—the preparer must still mark the taxpayer’s return to indicate that the taxpayer elected the opt-out option. This ensures clarity and compliance with state filing requirements.

Correcting these misconceptions can help taxpayers make informed decisions about their filing options and ensure tax preparers remain compliant with state rules and regulations.

Key takeaways

Understanding the West Virginia Opt 1 form is crucial for taxpayers who prefer paper filing over electronic submission of their income tax returns. The following points provide key insights into filling out and using this form:

- Eligibility for Opt-Out: Taxpayers who are served by tax preparers obligated to file more than 25 returns electronically can choose to opt out of electronic filing. This is a conscious choice made by the taxpayer, not suggested by the preparer.

- Completion and Signature: To officially opt out of electronic filing, taxpayers must complete and sign the OPT-1 form. This action registers their preference to not e-file their personal income tax return for specific stated reasons.

- Joint Filing Consideration: If filing jointly, both the taxpayer and the spouse are required to sign the form, indicating a mutual decision to opt out of electronic filing. This ensures that both parties acknowledge the preference for paper filing.

- Preparer’s Role: Tax preparers are required to retain the completed OPT-1 form for three tax years following the year for which the opt-out applies. Additionally, the income tax preparer must indicate on the taxpayer’s return that the election to opt-out of electronic filing was made by the taxpayer.

- Definition of Income Tax Preparer: The form clarifies who is considered an income tax preparer under West Virginia law. Importantly, this excludes individuals who prepare tax returns in certain capacities, such as fiduciaries of estates or trusts, or as partners preparing a return for a partnership.

Ensuring compliance with the stipulations of the West Virginia Opt 1 form is essential for both taxpayers and tax preparers to avoid potential issues with the state's tax department. By following these guidelines, taxpayers can make informed decisions about their filing preferences while adhering to regulatory requirements.

Popular PDF Forms

West Virginia Residency - By filling out WV/8379, injured spouses assert their right to a refund free from the encumbrances of the other spouse’s financial oversights.

Wv Employee Withholding Form - Directs taxpayers to the Tax Account Administration Division for mailing their estimated tax payments.