Free Wv 8379 Form

Navigating the financial implications of tax obligations when married can be complicated, especially when one spouse is left shouldering unfair tax liabilities due to the activities or debts of the other. The State of West Virginia provides a recourse through the WV 8379 form, a critical tool designed to ameliorate the effects of such circumstances. This form, officially known as the "Injured Spouse Allocation," is pivotal for married couples filing a joint tax return when part of their refund has been, or is expected to be, allocated towards the other spouse's past-due child support, back taxes, or other federal or state debt. It allows for the "injured" spouse, who is not responsible for these debts, to claim their share of the tax refund. The form entails a detailed process where the income and taxes paid by each spouse are reported and appropriately allocated. This methodology enables the West Virginia State Tax Department to calculate and disburse the injured spouse’s portion of the refund accurately. Essential elements such as actual income, adjustments to income, subtractions, exemptions, and various credits are meticulously factored into this calculation, ensuring a fair and equitable resolution. Furthermore, the form's accommodations for changes in mailing address and the necessity of attaching withholding tax statements underscore the state’s commitment to a thorough and responsive tax process. Through the provisions laid out in the form, it offers a financial lifeline for those inadvertently caught in the crossfire of a spouse's financial obligations.

Wv 8379 Example

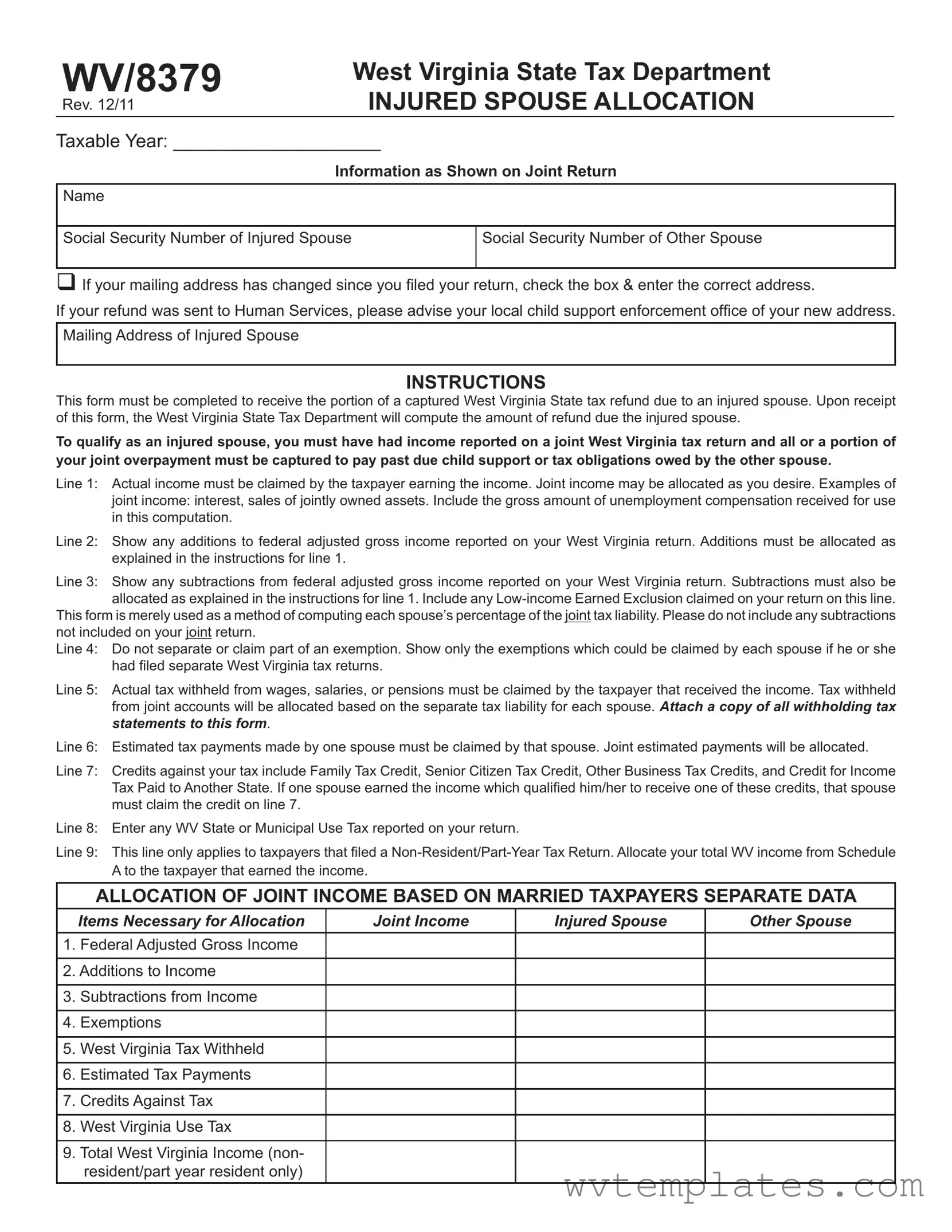

WV/8379 |

West Virginia State Tax Department |

|

INJURED SPOUSE ALLOCATION |

||

Rev. 12/11 |

Taxable Year: ____________________

Information as Shown on Joint Return

Name

Social Security Number of Injured Spouse

Social Security Number of Other Spouse

If your mailing address has changed since you iled your return, check the box & enter the correct address.

If your refund was sent to Human Services, please advise your local child support enforcement ofice of your new address.

Mailing Address of Injured Spouse

INSTRUCTIONS

This form must be completed to receive the portion of a captured West Virginia State tax refund due to an injured spouse. Upon receipt of this form, the West Virginia State Tax Department will compute the amount of refund due the injured spouse.

To qualify as an injured spouse, you must have had income reported on a joint West Virginia tax return and all or a portion of your joint overpayment must be captured to pay past due child support or tax obligations owed by the other spouse.

Line 1: Actual income must be claimed by the taxpayer earning the income. Joint income may be allocated as you desire. Examples of joint income: interest, sales of jointly owned assets. Include the gross amount of unemployment compensation received for use

in this computation.

Line 2: Show any additions to federal adjusted gross income reported on your West Virginia return. Additions must be allocated as explained in the instructions for line 1.

Line 3: Show any subtractions from federal adjusted gross income reported on your West Virginia return. Subtractions must also be allocated as explained in the instructions for line 1. Include any

This form is merely used as a method of computing each spouse’s percentage of the joint tax liability. Please do not include any subtractions not included on your joint return.

Line 4: Do not separate or claim part of an exemption. Show only the exemptions which could be claimed by each spouse if he or she had iled separate West Virginia tax returns.

Line 5: Actual tax withheld from wages, salaries, or pensions must be claimed by the taxpayer that received the income. Tax withheld

from joint accounts will be allocated based on the separate tax liability for each spouse. Attach a copy of all withholding tax statements to this form.

Line 6: Estimated tax payments made by one spouse must be claimed by that spouse. Joint estimated payments will be allocated.

Line 7: Credits against your tax include Family Tax Credit, Senior Citizen Tax Credit, Other Business Tax Credits, and Credit for Income Tax Paid to Another State. If one spouse earned the income which qualiied him/her to receive one of these credits, that spouse

must claim the credit on line 7.

Line 8: Enter any WV State or Municipal Use Tax reported on your return.

Line 9: This line only applies to taxpayers that iled a

A to the taxpayer that earned the income.

ALLOCATION OF JOINT INCOME BASED ON MARRIED TAXPAYERS SEPARATE DATA

|

Items Necessary for Allocation |

Joint Income |

Injured Spouse |

Other Spouse |

|

|

|

|

|

1. |

Federal Adjusted Gross Income |

|

|

|

|

|

|

|

|

2. Additions to Income |

|

|

|

|

|

|

|

|

|

3. |

Subtractions from Income |

|

|

|

|

|

|

|

|

4. |

Exemptions |

|

|

|

|

|

|

|

|

5. |

West Virginia Tax Withheld |

|

|

|

|

|

|

|

|

6. |

Estimated Tax Payments |

|

|

|

|

|

|

|

|

7. |

Credits Against Tax |

|

|

|

|

|

|

|

|

8. |

West Virginia Use Tax |

|

|

|

|

|

|

|

|

9. Total West Virginia Income (non- |

|

|

|

|

|

resident/part year resident only) |

|

|

|

|

|

|

|

|

Form Specifications

| Fact | Detail |

|---|---|

| Purpose | The WV/8379 form is designed for an injured spouse to claim their share of a joint tax refund captured for the other spouse's debts, such as past due child support or tax obligations. |

| Allocation of Income and Deductions | Income, additions, and deductions on a joint West Virginia tax return must be allocated between spouses to calculate the injured spouse's refund portion correctly. |

| Eligibility Requirements | To qualify as an injured spouse, one must have reported income on a joint return and part of the joint overpayment is applied towards the other spouse's obligation. |

| Governing Law | This form is governed by the tax laws of West Virginia as enforced by the West Virginia State Tax Department. |

Guide to Filling Out Wv 8379

Filling out the WV 8379 form is the next step to ensure that the injured spouse can claim their rightful share of a West Virginia State tax refund. This process might seem daunting at first, but it's crucial for protecting the injured spouse's interests when part of a joint tax refund has been allocated for debts owed by the other spouse. By following the detailed steps below, the injured spouse can accurately report their share of income, taxes withheld, and credits to receive the portion of the refund they are entitled to. Here's how to proceed:

- Enter the Taxable Year at the top of the form to specify the year for which you are claiming the injured spouse allocation.

- Under Information as Shown on Joint Return, provide the name and Social Security Number (SSN) of the injured spouse. Also, include the SSN of the other spouse.

- If there has been a change in your mailing address since the joint return was filed, check the box provided and enter the new address for the injured spouse.

- For individuals whose refund was sent to Human Services, inform your local child support enforcement office of the new address as well.

- Allocation of Joint Income Based on Married Taxpayers Separate Data: Start this section by reporting the Federal Adjusted Gross Income, ensuring to claim the actual income each taxpayer earned.

- Add any additions to the federal adjusted gross income as reported on your West Virginia return. Allocate these additions as per the guidelines for joint income.

- List any subtractions from the federal adjusted gross income that were reported on your West Virginia return, allocating them accordingly.

- For exemptions, indicate only those which each spouse could claim if they had filed separate West Virginia tax returns. Do not separate or claim part of an exemption.

- State the actual tax withheld from wages, salaries, or pensions for each spouse. Remember, tax withheld from joint accounts should be allocated based on each spouse's separate tax liability.

- If there were estimated tax payments made, allocate these to the spouse who made the payments. Joint estimated payments should be divided as explained.

- Line 7 asks for credits against tax. If one spouse earned the income qualifying them for any credits listed (e.g., Family Tax Credit, Senior Citizen Tax Credit), that spouse must claim the credit here.

- Enter any West Virginia State or Municipal Use Tax reported on your return.

- For non-resident or part-year resident filers, allocate your total WV income from Schedule A to the spouse that earned the income.

- Ensure to attach copies of all withholding tax statements to this form before submission.

After completing the form, review it carefully to ensure all information is accurate and corresponds with the shared income and tax details. This careful process helps protect the interests of the injured spouse, ensuring they receive the portion of the tax refund they are due without delay.

Things You Should Know About Wv 8379

What is the WV 8379 form used for?

The WV 8379 form, also known as the Injured Spouse Allocation form, is used by individuals to claim their portion of a West Virginia State tax refund that was captured to pay past due child support or tax obligations owed by their spouse. It is specifically designed for people who filed a joint tax return and allows them to allocate the joint overpayment based on each spouse's individual income and deductions.

How do I know if I qualify as an injured spouse?

To qualify as an injured spouse, you must meet specific criteria. First, you must have reported income on a joint West Virginia tax return. Secondly, a portion or all of your joint tax overpayment must have been captured to settle past due child support, spousal support, federal debts, state taxes, or other obligations that your spouse owes. Essentially, if your portion of the refund was used to cover your spouse's debt, you may qualify.

What information is required to complete the WV 8379 form?

Completing the form requires detailed information as shown on your joint tax return. This includes the name and Social Security numbers of both spouses, your current mailing address, and specific financial details like joint income, individual earnings, withholdings, estimated tax payments, and any applicable credits. You’ll need to accurately compute and allocate income and withholdings between you and your spouse according to the instructions provided for each line on the form.

Are there any attachments required when submitting the WV 8379 form?

Yes, you must attach all withholding tax statements to your WV 8379 form. These statements are necessary to verify the taxes that were withheld from your wages, salaries, pensions, or joint accounts, and to correctly allocate them between you and your spouse as part of the injured spouse claim process.

How is the refund amount for the injured spouse calculated?

The West Virginia State Tax Department will review the completed WV 8379 form and accompanying documentation to determine each spouse’s percentage of the joint tax liability. This includes analyzing the allocated joint income, deductions, and credits as outlined in the form. Based on this analysis, the department will compute the amount of refund due to the injured spouse, ensuring that only the income and payments applicable to the injured spouse are considered for their refund portion.

What should I do if my mailing address has changed since filing my return?

If your mailing address has changed since filing your joint tax return, you must check the designated box on the WV 8379 form and provide your new address. Additionally, if your refund was sent to Human Services (e.g., for child support enforcement), it's important to advise your local child support enforcement office of your new address to ensure proper handling of your refund.

Common mistakes

Filling out the WV 8379 form, known as the Injured Spouse Allocation form for the West Virginia State Tax Department, can be complex. It's designed to ensure that an injured spouse can claim their rightful portion of a tax refund that might otherwise be used to offset the debts of the other spouse. However, a few common mistakes can complicate the process, potentially delaying or even reducing the amount of the refund that the injured spouse is entitled to receive.

First, a critical mistake often made is not accurately reporting income. The form requires that actual income earned by each spouse be reported distinctly. This includes not only wages but also any joint income such as interest from joint accounts or proceeds from the sale of jointly owned assets. The injured spouse must carefully allocate this joint income on the form, as incorrect allocations can lead to miscalculations in the refund amount due.

Another area where errors frequently occur is with tax withholdings and estimated tax payments. On the WV 8379 form, it’s essential to claim only the taxes withheld from one’s own income, whether it be wages, salaries, or pensions. Similarly, estimated tax payments made by one spouse should not be mistakenly claimed by the other. These mistakes can alter the computation of each spouse's separate tax liability, potentially affecting the injured spouse's refund.

Additionally, when filling out the form, there’s often confusion over exemptions and credits. The form instructs not to divide exemptions or claim parts of an exemption but to show only those exemptions which each spouse could claim if they were filing separate West Virginia tax returns. Misunderstanding this instruction can lead to inaccuracies that may delay the processing of the form. Similarly, credits such as the Family Tax Credit or Credit for Income Tax Paid to Another State must be correctly allocated to the spouse who earned the applicable income, yet this is another common source of error.

Common mistakes include:

- Incorrectly reporting or allocating income, including joint income and individual earnings.

- Improperly attributing tax withholdings and estimated tax payments to the wrong spouse.

- Misunderstanding how to correctly claim exemptions and credits, leading to possible overestimations or underestimations of the injured spouse’s refund entitlement.

- Not attaching all necessary withholding tax statements, a crucial step for verifying the accurate tax withheld from wages, which is necessary for accurate processing.

To avoid these mistakes, it's recommended that individuals carefully read the instructions provided with the WV 8379 form and double-check their entries before submission. Ensuring accurate and complete information will help in receiving the correct portion of the tax refund efficiently and without unnecessary delays.

Documents used along the form

When dealing with the complexities of tax forms and financial obligations, many individuals find themselves navigating through a maze of paperwork. Specifically, those utilizing the West Virginia State Tax Department's WV/8379 form, or Injured Spouse Allocation, are working to claim their rightful portion of a tax refund that might otherwise be diverted for the payment of the other spouse's past obligations, such as child support or tax debts. This necessary document is but one in a repertoire often required for such financial matters. Here are several accompanying forms and documents that might also be pertinent in these situations:

- Form 1040: The U.S. individual income tax return form is pivotal for married couples filing jointly, as it details the income, deductions, and credits that contribute to their overall tax scenario, influencing the allocation process on the WV/8379 form.

- W-2 Forms: These wage and tax statement forms are essential for verifying the incomes of both spouses, helping to accurately allocate income as required on the WV/8379 form.

- Schedule A (Form 1040): For couples who itemize deductions instead of taking the standard deduction, this form provides the necessary details of these deductions, impacting the calculations on the WV/8379 form.

- Form 1099: These forms report various types of income other than wages, salaries, and tips. Relevant 1099 forms must be attached to validate any non-wage incomes reported on the WV/8379 form.

- Child Support Documents: For couples dealing with an injury spouse claim due to intercepted tax refunds for child support, official documents detailing the obligation may be required to substantiate the claim.

- Direct Deposit Forms: If the injured spouse's portion of the refund is approved, direct deposit forms may expedite the transfer of funds to the appropriate account.

- Power of Attorney (POA) Form: If one spouse cannot participate directly in filing or discussing the case, a POA form may be necessary to authorize representation on their behalf.

The process of reclaiming a portion of a tax refund as an injured spouse involves not just the WV/8379 form but also a constellation of other documents and forms that establish the couple's financial picture. Each document plays a role in ensuring that the allocation of joint income, exemptions, and credits is fair and justified. Understanding the purpose and requirement of each form can alleviate some of the frustrations often associated with navigating tax issues, especially those as nuanced and personalized as an injured spouse claim.

Similar forms

The IRS Form 8379, Injured Spouse Allocation, shares similarities with the WV 8379 in terms of purpose and utilization for couples filing joint tax returns. This federal form allows the "injured" spouse to claim their portion of a tax refund that might be held or intercepted by the IRS to cover the other spouse's separate debts, such as back taxes, child or spousal support, or federal debts like student loans. Both forms operate under the principle of dividing income and tax liabilities to ensure fair treatment of both parties in the relationship, especially when one spouse is not responsible for the other's debts.

Similar in concept to the Child Support Allocation Form used in some states, the WV 8379 allows for the allocation of joint tax refunds in cases where a portion might be intercepted for child support arrears owed by one spouse. Though tailored to specific state tax obligations, both documents aim to protect the financial interests of a spouse not responsible for the debt triggering the interception, ensuring that they receive their rightful share of any joint tax refunds. The methodology of allocating income and deductions helps determine what portion of a refund is rightfully owed to the non-debtor spouse.

The IRS Innocent Spouse Relief Form provides another comparative example, though its application and implications differ significantly. It's designed for situations where one spouse seeks relief from joint tax liability due to the actions or omissions of the other spouse. While the WV 8379 doesn't absolve tax liability, it similarly recognizes the concept of separate financial justice within joint filings, allowing for the allocation of refunds based on each spouse's income and tax responsibility without resolving liability issues.

The Allocation for Separate Filers Form, found in certain jurisdictions, also parallels the WV 8379. This form is used when individuals elect to file separate state tax returns but need to allocate joint incomes or deductions such as mortgage interest or real estate taxes. Like the WV 8379, this form acknowledges the complexities of shared finances and aims to equitably distribute tax obligations and benefits, reinforcing the principle of fairness in tax law by accounting for individual contributions to joint finances.

Dos and Don'ts

When completing the WV 8379 form for Injured Spouse Allocation, it's important to follow certain dos and don'ts to ensure the process goes smoothly. Here are key points to consider:

- Do thoroughly review the instructions before filling out the form to understand the requirements and processes.

- Do ensure that the social security numbers for both the injured spouse and the other spouse are correctly entered to avoid processing delays.

- Do report actual income earned by each spouse accurately to facilitate the correct allocation of joint income.

- Do attach all necessary withholding tax statements as required by line 5, to substantiate the claims for tax withheld.

- Do accurately allocate estimated tax payments and credits to the correct spouse, especially when only one spouse is responsible for the income that qualified for those credits or made the estimated payments.

- Don't forget to check the box if your mailing address has changed since filing your return, and provide the correct address to ensure you receive any correspondence or refunds.

- Don't include income, deductions, or credits on the form that were not reported on your joint West Virginia tax return, as this form is a tool for allocating already reported amounts, not for making corrections or updates to your return.

Misconceptions

When it comes to navigating tax forms, misunderstandings can easily arise. The WV 8379 form, used for injured spouse allocation in West Virginia, is no exception. Let's address and clarify some common misconceptions about this particular form to ensure taxpayers can approach it with confidence.

- Misconception 1: The injured spouse form is only for couples going through a divorce.

This belief is incorrect. The form aims to protect the tax refund portion of a spouse (the injured spouse) when the other spouse's debts, such as past-due child support or governmental obligations, risk claiming it. It applies regardless of the couple's marital status.

- Misconception 2: You can claim any part of an exemption on behalf of the injured spouse.

The form explicitly instructs not to separate or claim parts of exemptions. Each exemption should represent what each spouse could claim if they were filing separate West Virginia tax returns, supporting clear and fair allocation of tax liabilities and refunds.

- Misconception 3: Income must be allocated equally between spouses.

This is not accurate. The West Virginia State Tax Department allows joint income to be allocated in the manner the couple sees fit, with the requirement that actual earned income must be claimed by the person who earned it, ensuring a more equitable division based on individual contributions.

- Misconception 4: The form is a request to split the tax refund evenly.

While it might seem like the form aims to divide the refund 50/50, its actual purpose is to compute each spouse's percentage of the joint tax liability based on their respective incomes, withholdings, and credits. This computation helps determine the injured spouse's fair share of the refund.

- Misconception 5: All tax credits must be divided.

It's a common mistake to think that. However, the form requires that credits such as the Family Tax Credit, Senior Citizen Tax Credit, and others be claimed only by the spouse whose income qualified for those credits. This specificity ensures that benefits are allocated based on individual eligibility rather than a blanket division.

- Misconception 6: You do not need to attach any documentation.

Contrary to this belief, attaching withholding tax statements and other relevant documentation is necessary for processing the form. This evidence supports the allocation claims made and assists the tax department in determining the correct refund amount for the injured spouse.

- Misconception 7: The form affects how your taxes are filed in the future.

Using this form does not impact how a couple files their taxes in subsequent years. It is a solution for a specific tax year where an injured spouse seeks to protect their portion of a refund. Couples can choose how to file their taxes each year independently of past injured spouse claims.

Understanding these misconceptions can help taxpayers navigate the complexities of the WV 8379 form more effectively, ensuring that injured spouses can claim their rightful portion of a tax refund. Knowledge empowers individuals to take the correct steps in securing their financial interests within the bounds of tax laws.

Key takeaways

When dealing with West Virginia State tax issues, particularly in situations involving an injured spouse, the WV 8379 form becomes critically important. Here are the key takeaways you need to understand for filling out and using this form effectively:

- Definition of an Injured Spouse: An injured spouse in West Virginia is someone who may lose part of their tax refund due to their partner's debts, such as past-due child support or tax obligations. For these individuals, the WV 8379 form is a tool to claim their share of a joint tax refund.

- Importance of Accurate Information: The form requires accurate details as reported on your joint tax return. This includes the name, Social Security numbers, and the most current mailing address for the injured spouse.

- Allocation of Income: Both actual income earned by each spouse and joint income need to be reported. For joint income like interest from joint accounts or sales of jointly owned property, this form allows for allocation as deemed appropriate by the filing parties.

- Allocation of Additions and Subtractions to Income: Specific additions to and subtractions from your federal adjusted gross income, as reported on your state return, must be accurately allocated between spouses on the form. This includes items such as low-income exclusions.

- No Partial Exemptions: Exemptions should be reported as if each spouse filed separately. Partial exemptions are not permissible on the WV 8379 form.

- Withheld Taxes and Estimated Payments: Taxes withheld from wages, salaries, pensions, or estimated tax payments must be claimed by the spouse who earned the income. For joint accounts or payments, allocation is based on each spouse's separate tax liability.

- Claiming Credits: If one spouse qualifies for specific tax credits based on their income, such as the Family Tax Credit or Senior Citizen Tax Credit, that spouse must claim the credit on the form.

- Reporting Use Tax: Any West Virginia State or Municipal Use Tax reported on your return should also be included on the form.

- Non-Resident/Part-Year Resident Allocation: For those who filed a Non-Resident/Part-Year return, it's essential to allocate total West Virginia income from Schedule A to the spouse who earned it.

Completing the WV 8379 form can ensure that an injured spouse receives their fair share of a joint tax refund, protecting them from losing out due to debts that are not their own. It is crucial to fill out the form carefully, providing precise information and understanding the allocation rules to accurately compute each spouse's share of the tax obligations and refunds.

Popular PDF Forms

Credentialing Documents - The section on Workers’ Compensation Information underlines the necessity of being prepared to handle patients with work-related injuries or illnesses.

Wv Sales and Use Tax Form - The clear demarcation between refund and credit options in the form allows businesses to tailor their claims based on their financial strategies and needs.

Wv State Tax Forms - Updates wineries about state tax department innovations, aiming to improve the reporting process.