Free Wv 8453 Form

In the realm of tax preparation, the State of West Virginia Individual Income Tax Declaration for Electronic Filing, commonly referred to as form WV-8453, plays a pivotal role for residents completing their income tax returns digitally for the year specified, in this instance, from January 1 through December 31, 2005. This form serves multiple essential functions: it acts as a formal agreement between the taxpayer and the state facilitating the electronic filing process, it details the taxpayer's consent for direct deposit of refunds or electronic withdrawal of payments due, and it confirms the accuracy of the submitted tax information under the penalties of perjury. Taxpayers provide personal identification, including their social security numbers, address, and contact information, alongside critical financial figures such as federal adjusted gross income and state income tax. Furthermore, it outlines options for taxpayers to designate their banking details for direct transactions with the state tax department. The declaration section requires signatures from the taxpayer, and if applicable, their spouse, thereby verifying the information's correctness to their best knowledge and belief. Paid preparers or Electronic Return Originators (EROs) are also mandated to sign the form, asserting that they have reviewed the information and found it to be accurate. Importantly, the form mandates retention of these documents and all supporting materials for at least three years post-filing, ensuring a comprehensive record-keeping system is in place for verification and future reference purposes. This form underscores the significance of accuracy and accountability in the electronic filing process, streamlining the tax submission and refund delivery system for both taxpayers and the state.

Wv 8453 Example

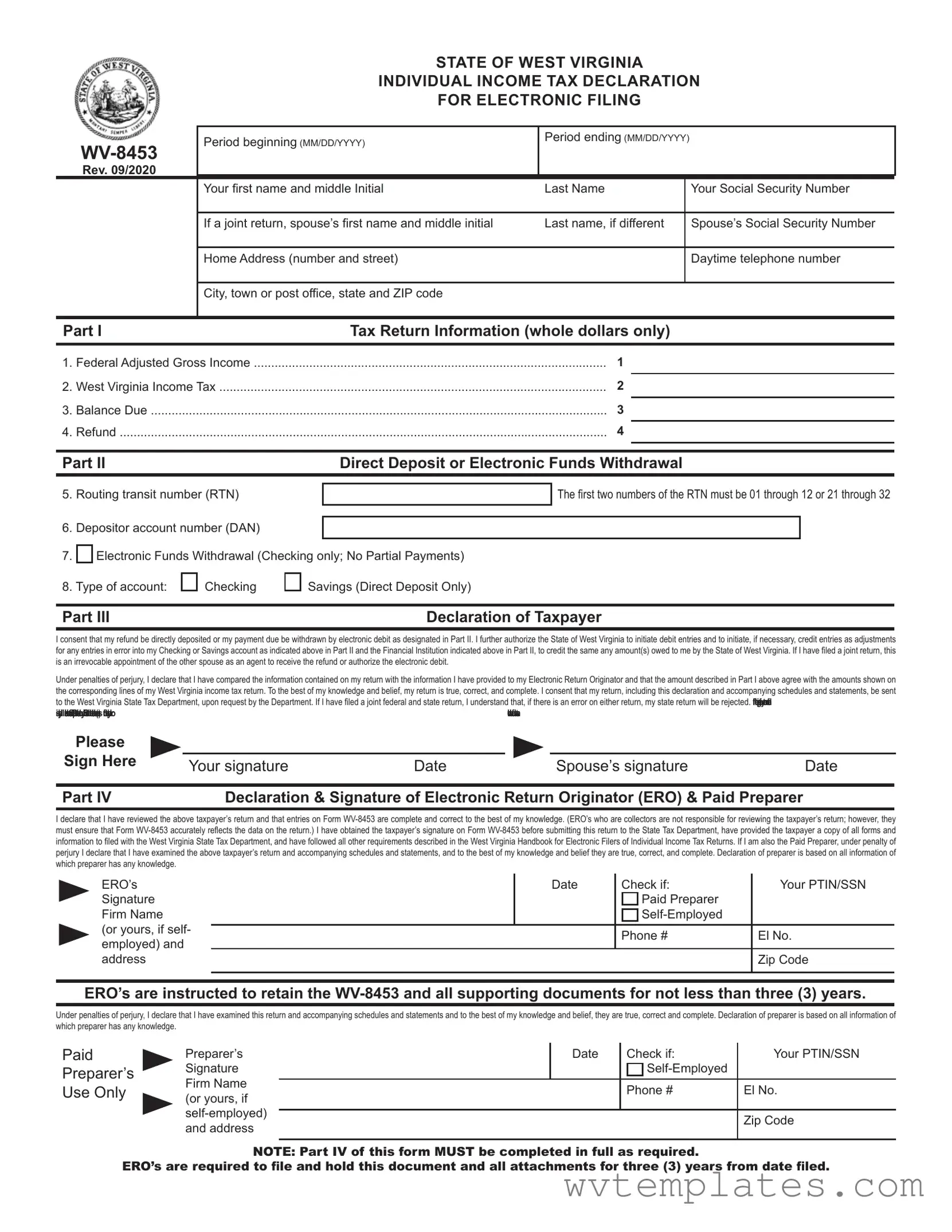

STATE OF WEST VIRGINIA

INDIVIDUAL INCOME TAX DECLARATION

FOR ELECTRONIC FILING

Rev. 09/2020

Period beginning (MM/DD/YYYY)

Period ending (MM/DD/YYYY)

Your first name and middle Initial |

Last Name |

Your Social Security Number

If a joint return, spouse’s first name and middle initial |

Last name, if different |

Spouse’s Social Security Number

Home Address (number and street)

Daytime telephone number

|

|

City, town or post office, state and ZIP code |

|

Part I |

|

Tax Return Information (whole dollars only) |

|

1. |

Federal Adjusted Gross Income |

1 |

|

2. |

West Virginia Income Tax |

2 |

|

3. |

Balance Due |

3 |

|

4. |

Refund |

4 |

|

Part II |

|

Direct Deposit or Electronic Funds Withdrawal |

|

5. |

Routing transit number (RTN) |

The first two numbers of the RTN must be 01 through 12 or 21 through 32 |

|

6. |

Depositor account number (DAN) |

|

|

7. |

Electronic Funds Withdrawal (Checking only; No Partial Payments) |

||

8. Type of account: |

Checking |

Savings (Direct Deposit Only) |

|

Part III |

|

Declaration of Taxpayer |

|

I consent that my refund be directly deposited or my payment due be withdrawn by electronic debit as designated in Part II. I further authorize the State of West Virginia to initiate debit entries and to initiate, if necessary, credit entries as adjustments for any entries in error into my Checking or Savings account as indicated above in Part II and the Financial Institution indicated above in Part II, to credit the same any amount(s) owed to me by the State of West Virginia. If I have filed a joint return, this is an irrevocable appointment of the other spouse as an agent to receive the refund or authorize the electronic debit.

Under penalties of perjury, I declare that I have compared the information contained on my return with the information I have provided to my Electronic Return Originator and that the amount described in Part I above agree with the amounts shown on the corresponding lines of my West Virginia income tax return. To the best of my knowledge and belief, my return is true, correct, and complete. I consent that my return, including this declaration and accompanying schedules and statements, be sent to the West Virginia State Tax Department, upon request by the Department. If I have filed a joint federal and state return, I understand that, if there is an error on either return, my state return will be rejected. If the processing of my return or refund

is delayed, I authorize the State Tax Department to disclose to my ERO and /or the transmitter the reason(s) for the delay, or |

|

when the refund was sent. |

|

|

||||||

Please |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Sign Here |

|

|

|

|

|

|

|

|

|

|

Your signature |

Date |

|

|

|

Spouse’s signature |

Date |

||||

|

|

|

|

|||||||

Part IV |

Declaration & Signature of Electronic Return Originator (ERO) & Paid Preparer |

|

|

|||||||

I declare that I have reviewed the above taxpayer’s return and that entries on Form

ERO’s Signature Firm Name

(or yours, if self- employed) and address

|

Date |

Check if: |

Your PTIN/SSN |

|

|

Paid Preparer |

|

|

|

|

|

|

|

Phone # |

El No. |

|

|

|

|

|

|

|

Zip Code |

|

|

|

|

ERO’s are instructed to retain the

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements and to the best of my knowledge and belief, they are true, correct and complete. Declaration of preparer is based on all information of which preparer has any knowledge.

Paid

Preparer’s

Use Only

Preparer’s

Signature

Firm Name (or yours, if

|

Date |

Check if: |

Your PTIN/SSN |

|

|

|

|

|

|

Phone # |

El No. |

|

|

|

|

|

|

|

Zip Code |

|

|

|

|

NOTE: Part IV of this form MUST be completed in full as required.

ERO’s are required to file and hold this document and all attachments for three (3) years from date filed.

Form Specifications

| Fact | Detail |

|---|---|

| Form Type | WV-8453: Individual Income Tax Declaration for Electronic Filing |

| State | West Virginia |

| Tax Year | 2005 |

| Revision Date | October 2005 |

| Main Purpose | To declare consent for electronic filing of West Virginia individual income tax, including authorizations for direct deposit or electronic funds withdrawal. |

| Part I Details | Contains Tax Return Information such as Federal Adjusted Gross Income, West Virginia Income Tax, Balance Due, and Refund details. |

| Part II Instructions | Guides on Direct Deposit or Electronic Funds Withdrawal options, requiring Routing Transit Number (RTN), Depositor Account Number (DAN), and account type. |

| Declaration Requirements | Taxpayers must consent to the direct deposit or electronic funds withdrawal, authorizing the State of West Virginia and financial institutions to process such transactions. The declaration includes authorization, perjury statement, and instructions for submission errors and processing delays disclosure. |

| Retention Period for ERO | Electronic Return Originators (EROs) must retain Form WV-8453 and all supporting documents for no less than three years from the date filed. |

Guide to Filling Out Wv 8453

Successfully filing your taxes requires attention to detail and ensuring all required forms are completed accurately. The WV 8453 form is a crucial document for individuals in West Virginia electing to file their income tax returns electronically. This form serves as a declaration for electronic filing and provides essential details about the taxpayer’s return. Following the correct procedures for filling out this form is important to avoid any delays or issues with your tax return processing. Below is a step-by-step guide to assist you.

- Begin by entering your first name, middle initial, and last name in the designated spaces. If you are filing a joint return, also include your spouse's first name, middle initial, and their last name if it is different from yours.

- Provide your Social Security Number in the space provided. For joint returns, include your spouse's Social Security Number as well.

- Fill in your home address, including the number and street. If your mailing address is different from your home, include that as well.

- Add your daytime telephone number for any potential follow-up or clarification needs.

- Write the city, town, or post office, as well as the state and ZIP code associated with your home address.

- Enter your Federal Adjusted Gross Income as reported on Form IT-140, Line 1, in the field labeled "1."

- For West Virginia Income Tax, refer to Form IT-140, Line 8, and enter this amount in the space for "2."

- If there is a balance due, look to IT-140, Line 17, and record this amount in the section marked "3."

- For refunds, locate the amount on Form IT-140, Line 22, and input it in the space provided for "4."

- If opting for direct deposit or electronic funds withdrawal, fill in your Routing Transit Number (RTN) and Depositor Account Number (DAN) in the sections labeled "5" and "6" respectively. Ensure the RTN is within the accepted range.

- Indicate your account type by marking either "Checking" or "Savings" to specify the destination for direct deposit or source of electronic funds withdrawal.

- Complete Part III by consenting to the direct deposit or electronic funds withdrawal authorization, as applicable. Ensure you and, if filing jointly, your spouse sign and date the form to validate it.

- Part IV should be completed by the Electronic Return Originator (ERO) and, if applicable, the Paid Preparer. They must verify the return’s accuracy, declare their review, and sign and date the form. Ensure the ERO fills in their PTIN/SSN, and if self-employed, includes their firm's information.

After completing these steps, review the form to ensure all information is accurate and complete. Retain a copy for your records, and submit the form as directed by the Electronic Return Originator or the instructions provided with your tax return package. Properly completing the WV 8453 form is a critical step in the electronic filing process, ensuring your tax return is processed efficiently and accurately.

Things You Should Know About Wv 8453

What is the WV-8453 form?

The WV-8453 form is the State of West Virginia Individual Income Tax Declaration for Electronic Filing. It's used for the tax year stated on the form to authorize the electronic filing of a West Virginia individual income tax return. Essentially, it’s a way to say you agree with the information that will be submitted electronically to the West Virginia State Tax Department on your behalf.

Who needs to file the WV-8453 form?

Any taxpayer who chooses to file their West Virginia individual income tax return electronically must complete and submit the WV-8453 form. This applies to both individuals and those filing a joint return with a spouse.

Where do I get the WV-8453 form?

You can obtain the WV-8453 form from the West Virginia State Tax Department’s website or from a tax professional who is handling your electronic tax filing. Electronic Return Originators (EROs) also provide this form when they prepare your taxes for e-filing.

What information do I need to fill out on the WV-8453 form?

You will need your federal adjusted gross income, your West Virginia income tax, any balance due or refund amount, and your direct deposit or electronic funds withdrawal information. Additionally, you’ll need basic personal information, including your Social Security Number and your spouse’s, if filing jointly, along with your contact details.

How do I submit the WV-8453 form?

After completing the form, you should provide it to your ERO or tax preparer, who will then submit it along with your electronic tax return. Keep in mind, the taxpayer must sign the form before submission, indicating their agreement with the information filed.

Is there a filing deadline for the WV-8453 form?

Yes, the filing deadline corresponds with the West Virginia individual income tax return deadline, which is typically April 15, unless extended for a specific tax year. To avoid penalties or delays, ensure your form is submitted on time.

What happens if I make a mistake on the form?

If a mistake is discovered before submission, you can correct it on the form before giving it to your ERO. If the mistake is found after submission, contact the West Virginia State Tax Department or your tax preparer as soon as possible to correct the error. Depending on the type of mistake, it may be necessary to file an amended tax return.

Common mistakes

When preparing the West Virginia Individual Income Tax Declaration for Electronic Filing (WV-8453), individuals often encounter several common pitfalls. Recognizing and addressing these errors early can streamline the filing process, ensuring timely and accurate processing of one's tax return. Highlighted below are seven frequent mistakes to be wary of:

- Omitting or inaccurately reporting Social Security Numbers (SSNs). The SSNs for both the taxpayer and spouse, if filing jointly, must match the SSNs on record. Any discrepancy or omission can lead to processing delays or rejection of the return.

- Incorrectly entering the Routing Transit Number (RTN) or Depositor Account Number (DAN) in Part II. These numbers must be accurately provided for direct deposit or electronic funds withdrawal. Entering incorrect banking information could result in lost refunds or payment errors.

- Failure to report the Federal Adjusted Gross Income and West Virginia Income Tax faithfully from Forms IT-140, Lines 1 and 8, respectively. These amounts must accurately reflect those reported on the state tax return to avoid discrepancies.

- Ignoring the requirement to check the type of account (checking or savings) for the direct deposit or withdrawal. This oversight can result in failed transactions if the wrong account type is specified or left blank.

- Neglecting the consent declaration in Part III. Signatures are mandatory to validate the taxpayer’s and spouse’s (if applicable) agreement to the terms of electronic processing. Missing signatures can invalidate the submission.

- Overlooking the Declaration & Signature section for the Electronic Return Originator (ERO) and Paid Preparer in Part IV. This section must be completed in full, affirming the accuracy and completeness of the return as prepared. This is a critical step to ensure accountability and compliance with filing standards.

- Submitting the form without ensuring that all required fields are completed. Incomplete forms or those with inconsistencies in reported figures compared to the accompanying documentation are subject to rejection.

Avoiding these mistakes not only facilitates a smoother filing process but also minimizes the risk of delays or additional inquiries from the State Tax Department. Taxpayers are encouraged to review their WV-8453 form thoroughly before submission, cross-referencing all reported figures with their primary tax documents. For those unsure about any part of the form, seeking guidance from a qualified tax professional or an ERO is advisable to ensure compliance and accuracy of their tax filings.

In conclusion, the attention given to the preparation of the WV-8453 form can significantly influence the efficiency and outcome of one’s tax return processing. By being mindful of the common errors listed above, taxpayers can better navigate the complexities of electronic filing, contributing to a timely and correct tax return. For further assistance, the West Virginia State Tax Department and qualified tax preparers offer resources and support to aid in the successful submission of tax documents.

Documents used along the form

When filing the WV-8453 form, an individual income tax declaration for electronic filing in West Virginia, it's common to use several other documents to ensure accuracy and compliance with state and federal tax laws. These forms and documents play crucial roles in the filing process, aiding in the accurate reporting of income, tax deductions, and credits.

- Form IT-140: This is the West Virginia Personal Income Tax Return document. It's the primary form used by residents to file their state income tax. It details the taxpayer's income, calculates the state tax based on this income, and shows whether the filer owes the state money or is due a refund.

- Schedule A: Often attached to the IT-140, Schedule A is used to itemize deductions such as medical and dental expenses, taxes paid, interest paid, gifts to charity, and casualty and theft losses. This form helps taxpayers increase their deductible expenses, potentially reducing their taxable income.

- W-2 Forms: These are Wage and Tax Statements provided by employers. They report an employee's annual wages and the amount of taxes withheld from their paycheck. Filers use this information to complete both federal and state tax returns, ensuring the income is accurately reported.

- 1099 Forms: Various 1099 forms report different types of income other than wages, salaries, and tips. For instance, 1099-INT for interest earned, 1099-DIV for dividends, and 1099-MISC for miscellaneous income. These documents are necessary for taxpayers to report all sources of income accurately.

Collectively, these documents contribute to a comprehensive and compliant tax filing. Using the WV-8453 alongside these forms ensures that taxpayers provide a full picture of their financial situation to the West Virginia State Tax Department, facilitating a smoother filing process and accurate tax assessment.

Similar forms

The WV 8453 form, specific to West Virginia, is closely related to the IRS Form 8879, the IRS e-file Signature Authorization. Both forms serve as tools to authenticate the taxpayer's consent to electronically file their tax returns. While WV 8453 pertains to West Virginia state taxes, Form 8879 applies to federal tax returns. Each form collects taxpayer information, including Social Security Numbers, and details regarding refunds or balances due, and requires taxpayer signatures to authorize electronic submission.

Form W-2, the Wage and Tax Statement, shares similarities with the WV 8453 in that it is integral to tax filing processes. The Form W-2 is issued by employers to employees to report annual wages and the amount of taxes withheld from their paychecks. Like the WV 8453, it includes necessary personal and financial information, which is crucial for accurately preparing tax returns. However, the W-2 is an informational document provided by employers, whereas the WV 8453 is completed by the taxpayer or their representative.

Another related document is the Form 1040, the U.S. Individual Income Tax Return. It is the federal counterpart to state-level income tax declarations like WV 8453. Form 1040 collects detailed information about an individual's income, deductions, and credits to determine their tax liability. While WV 8453 focuses on state tax obligations in West Virginia, Form 1040 addresses federal taxes, linking them through the necessity of sharing some of the same financial information across both forms.

Similar to the WV 8453 is the Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. While WV 8453 is used for electronic filing authorization, Form 4868 is submitted when taxpayers need more time to file their federal income tax return. Both forms involve the IRS and taxation processes, but they serve different purposes: one for electronic filing consent and the other for requesting filing extensions.

Form 1099, particularly its various versions (like 1099-MISC, 1099-INT), shares a link with the WV 8453 as well. These forms report various types of income other than wages, salaries, and tips. The information reported on Form 1099s can affect the tax return information used in WV 8453, such as in determining the federal adjusted gross income, which is necessary for completing both state and federal tax forms.

The Schedule SE (Form 1040), Self-Employment Tax, bears similarity to WV 8453 as it pertains to the tax filing process, focusing on individuals who have earned income from self-employment. It calculates the amount of self-employment tax owed by a taxpayer, information that would influence the numbers reported on the WV 8453. While Schedule SE applies to federal tax calculations, it indirectly informs state tax obligations.

Form IT-140, the West Virginia Personal Income Tax Return, is directly related to the WV 8543. It is where the taxpayer reports their West Virginia income, calculates tax liability, and determines either the amount owed to the state or the refund due from it. The WV 8453 serves as a declaration for electronic filing of the information completed in Form IT-140, making them complementary components of the state’s e-filing process.

Form 8822, Change of Address, although not exclusively for tax filing, is related to the WV 8453 by ensuring the IRS and state tax agencies have current taxpayer information. If a taxpayer moves and files Form 8822, this updated address information should be reflected in the WV 8453 to ensure correspondence and tax documents are accurately sent. Both are administrative forms that support the proper management of tax filings.

The Electronic Funds Withdrawal (EFW) Authorization Form is another document that functions similarly to a section of WV 8453. It specifically relates to the direct deposit or electronic funds withdrawal for tax payments or refunds, a feature also present in WV 8453's design. While an EFW Authorization Form is more generically used for various types of payments to the IRS or states, the WV 8451 includes similar authorization specifically for the purpose of state tax payments or refunds.

Last, the Direct Deposit of Refund to More Than One Account form, used for allocating a tax refund among multiple accounts, is conceptually related to the direct deposit information section of WV 8453. Both allow taxpayers to designate where they want their refunds deposited, though the WV 8453 is confined to either a single checking or savings account for the convenience of state tax refund processing.

Dos and Don'ts

When preparing to fill out the WV-8453 form for your West Virginia Individual Income Tax Declaration for Electronic Filing, there are important steps to follow and pitfalls to avoid ensuring your tax filing process is smooth and error-free. Here are the do’s and don’ts to consider:

- Do ensure all information matches the information on your federal income tax return and the West Virginia IT-140 form.

- Do review the routing and account numbers twice if you opt for direct deposit or electronic funds withdrawal to avoid any issues with your refund or payment.

- Do sign and date the form. If filing jointly, make sure both spouses sign and date the form to validate it.

- Do keep a copy of the form and all related documentation for your records. It’s recommended to retain these documents for at least three years.

- Do use whole dollar amounts when reporting figures, as specified in the form instructions.

- Don’t leave any required fields blank. Incomplete forms may result in processing delays or rejection.

- Don’t guess amounts or information; ensure you refer to your financial records and tax documents to provide accurate information.

- Don’t attempt to file electronically without the consent of your spouse if filing a joint return. This form serves as an irrevocable appointment of the other spouse as an agent to authorize the electronic transaction.

- Don’t choose partial payment if electing to pay by electronic funds withdrawal, as it is not permitted according to the instructions.

- Don’t forget to review the declaration section carefully before signing, as signing under penalty of perjury means you are attesting to the accuracy of the information provided.

By following these guidelines, you can help ensure that your West Virginia Individual Income Tax filing is successful and free of common errors. For any uncertainties or questions, consider consulting a tax professional to guide you through the process.

Misconceptions

When discussing tax forms such as the WV-8453, the Individual Income Tax Declaration for Electronic Filing for the State of West Virginia, several misconceptions often arise. These misunderstandings can lead to confusion and errors in filing. It's crucial to dispel these myths for a smoother tax filing experience.

- Misconception 1: The WV-8453 form is only for taxpayers who owe money to the state. This is incorrect. The form is utilized for electronic filing of state income tax returns regardless of whether the taxpayer is expecting a refund, owes taxes, or is filing a return with a zero amount due.

- Misconception 2: Direct deposit information is optional. If you are expecting a refund and wish to receive it via direct deposit, providing accurate routing and account numbers in Part II of the form is imperative. Without this information, your refund cannot be processed for direct deposit.

- Misconception 3: Electronic Funds Withdrawal (EFW) can be used for partial payments. Part II, item 7, specifically states that EFW is available for checking accounts only and does not allow for partial payments. Taxpayers must pay the full amount due if they choose this payment method.

- Misconception 4: The taxpayer's consent is not necessary for electronic transactions. On the contrary, Part III of the form requires the taxpayer's consent for both direct deposit of refunds and electronic funds withdrawal for payments. This consent is vital for the transactions to be legally authorized.

- Misconception 5: Joint filers do not need to pay special attention to the form. In cases of joint filing, one spouse giving consent also acts as an irrevocable appointment of the other spouse as an agent for these transactions. This underlines the importance of both spouses understanding and agreeing to the declarations made in the form.

- Misconception 6: Accuracy of information in Part I does not require verification. The declaration in Part III emphasizes the taxpayer's responsibility to ensure that the information provided matches the details on their West Virginia income tax return. Accuracy here is crucial for a correct and complete filing.

- Misconception 7: Electronic Return Originators (EROs) are responsible for the accuracy of the taxpayer's return. While EROs do play a role in ensuring the data on Form WV-8453 reflects the return accurately, it is ultimately the taxpayer's responsibility to verify that their income tax return is true, correct, and complete. EROs must also follow specific requirements but are not responsible for reviewing the taxpayer's return in its entirety.

Understanding the WV-8453 form and clearing up these common misconceptions will aid taxpayers in the accurate and efficient filing of their state income tax returns. Always ensure that you cross-check the information provided with the official tax documents to ensure compliance and accuracy in your tax filings.

Key takeaways

When preparing to file your taxes electronically in the State of West Virginia, it's important to understand the purpose and requirements of the WV 8453 form. Here are six key takeaways to aid in the process:

- The WV 8453 form serves as an Individual Income Tax Declaration for Electronic Filing. It is crucial for the year specified, in this case, January 1 through December 31, 2005.

- Part I of the form requires information about your Federal Adjusted Gross Income, West Virginia Income Tax, any balance due, and refund details, ensuring that these figures match those on your West Virginia income tax return.

- For taxpayers opting for direct deposit or electronic funds withdrawal, Part II requests banking details including the Routing Transit Number (RTN), Depositor Account Number (DAN), and the type of account. This section facilitates either the direct deposit of refunds or the electronic withdrawal of tax payments due.

- The declaration section in Part III is where you, and if applicable, your spouse, consent to the direct deposit or electronic withdrawal as detailed in Part II. This part also involves a declaration under penalty of perjury that the information provided is accurate and the tax return is true, correct, and complete to the best of your knowledge.

- Part IV needs to be completed by the Electronic Return Originator (ERO) and, if different, the Paid Preparer. It includes a declaration confirming the accuracy of the information on the WV 8453 form as it reflects the data on the tax return. The preparer must also confirm that they have followed the requirements as outlined in the West Virginia Handbook for Electronic Filers of Individual Income Tax Returns for the specified tax year.

- Electronic Return Originators are instructed to retain the WV-8453 form along with all supporting documents for a minimum of three years from the date the return was filed. This requirement ensures that documentation is available should any questions or issues arise concerning the filed return.

Understanding these key aspects of the WV 8453 form can streamline the process of electronically filing your West Virginia state income tax return. Ensuring that all parts of the form are completed accurately and thoroughly can help in avoiding processing delays and ensuring that any refunds due are received promptly.

Popular PDF Forms

West Virginia State Tax Department - Instructions for mailing addresses differentiate between those expecting a refund and those owing additional taxes.

Credentialing Documents - The credentialing form emphasizes the importance of verifying tax identification numbers for each payer, reflecting the administrative aspect of credentialing.