Free Wv Cst 250 Form

Delving into the world of taxes and regulations, the WV CST-250 form emerges as a critical document for businesses in West Virginia that opt to handle their sales and use tax obligations directly with the state. Tailored for companies engaged in a variety of activities—from manufacturing and providing utilities to non-profit operations and healthcare providers—this application enables them to bypass the traditional method of tax collection through vendors and take matters into their own hands. Such autonomy comes with stringent requirements, including the regular filing of returns, meticulous bookkeeping for audits, and the responsibility of notifying vendors about their direct pay permit status. Issued by the West Virginia State Tax Department, this permit not only streamlines the tax payment process but also puts businesses under the watchful eye of tax authorities to ensure compliance. The form itself requires detailed business information, a declaration of tax compliance, and specifics of the business activities within West Virginia, undersigned with the solemnity of perjury. Moreover, it touches upon the perks of having a direct pay permit, like the ability to directly remit taxes due, and elaborates on the obligations such as notifying vendors and maintaining accurate records for inspection. With penalties awaiting those who falter, the signification of this form and its accompanying responsibilities are immense, making it pivotal for eligible businesses aiming to wield greater control over their tax affairs.

Wv Cst 250 Example

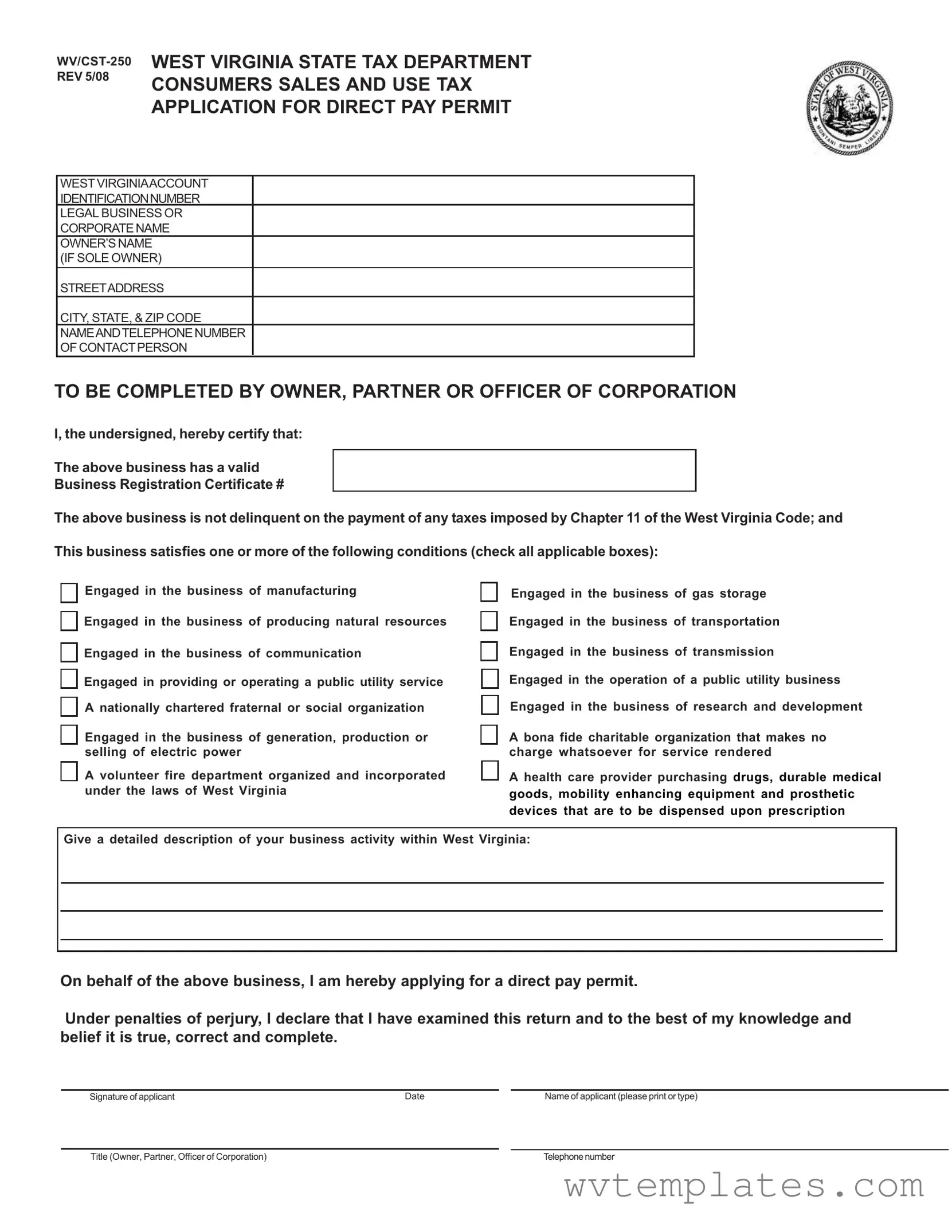

WEST VIRGINIA STATE TAX DEPARTMENT CONSUMERS SALES AND USE TAX APPLICATION FOR DIRECT PAY PERMIT

WESTVIRGINIAACCOUNT

IDENTIFICATIONNUMBER

LEGAL BUSINESS OR

CORPORATENAME

OWNER’SNAME (IF SOLE OWNER)

STREETADDRESS

CITY, STATE, & ZIP CODE

NAMEANDTELEPHONENUMBER

OF CONTACTPERSON

TO BE COMPLETED BY OWNER, PARTNER OR OFFICER OF CORPORATION

I, the undersigned, hereby certify that:

The above business has a valid

Business Registration Certificate #

The above business is not delinquent on the payment of any taxes imposed by Chapter 11 of the West Virginia Code; and This business satisfies one or more of the following conditions (check all applicable boxes):

Engaged in the business of manufacturing

Engaged in the business of producing natural resources

Engaged in the business of communication

Engaged in providing or operating a public utility service

A nationally chartered fraternal or social organization

Engaged in the business of generation, production or selling of electric power

A volunteer fire department organized and incorporated under the laws of West Virginia

Engaged in the business of gas storage

Engaged in the business of transportation

Engaged in the business of transmission

Engaged in the operation of a public utility business

Engaged in the business of research and development

A bona fide charitable organization that makes no charge whatsoever for service rendered

A health care provider purchasing drugs, durable medical goods, mobility enhancing equipment and prosthetic devices that are to be dispensed upon prescription

Give a detailed description of your business activity within West Virginia:

On behalf of the above business, I am hereby applying for a direct pay permit.

Under penalties of perjury, I declare that I have examined this return and to the best of my knowledge and belief it is true, correct and complete.

Signature of applicant |

Date |

Name of applicant (please print or type) |

Title (Owner, Partner, Officer of Corporation) |

Telephonenumber |

REV 5/08

The State Tax Commissioner may, in his discretion, authorize a person that is a user, consumer, distributor or lessee to which sales or leases of tangible personal property are made or services provided, to pay consumers sales and/or use tax directly to the West Virginia State Tax Department thereby waiving the collection of the tax by that person’s vendor. (W.Va. Code §

The issuance of a Direct Pay Permit imposes certain requirements on the holder of such permit. These requirements include:

1.Notification of each vendor from whom tangible personal property is purchased or leased or from whom services are purchased of his Direct Pay Permit Number and that any tax thereon will be paid directly to the Tax Commissioner. If the Direct Pay Permit Number is changed by the Tax Commissioner, all vendors must be renotified.

2.Filing a Direct Pay Consumers Sales or Use Tax Return on or before the 20th day of the month for the proceeding month’s or quarter’s transaction. Direct Pay Consumers Sales and Use Tax Returns not filed by the due date will be subject to interest and penalties and the permit may be cancelled.

3.Maintenance of books, records and invoices (including vendor lists) for inspection by the West Virginia State Tax Depart ment.

4.A Direct Pay Permit may not be used to purchase food, gasoline or special fuel.

INSTRUCTIONS FOR APPLICANT

This application is NOT valid unless all entries are completed.

Upon review of the application, the West Virginia State Tax Department will determine whether you are entitled to receive a Direct Pay Permit. Upon approval of your application, a numbered Direct Pay Permit will be mailed to you. Should your application be rejected, you will be notified in writing.

Direct Pay Consumers Sales and Use Tax Returns will be forwarded to you by the Department for remitting tax. If you do not receive a Direct Pay Consumers Sales and Use Tax Return within sixty (60) days after you receive your Direct Pay Permit, you must notify the West Virginia State Tax Department.

A Direct Pay Permit will continue to be valid until it is surrendered by you or cancelled. You will be notified by the State Tax Department of any change in your Direct Pay Permit number.

Upon surrender or cancellation of the Direct Pay Permit, the holder must promptly notify, in writing, the specified vendors from whom tangible personal property is purchased or leased or by whom services are rendered of such surrender or cancellation.

MAIL TO:

WEST VIRGINIASTATE TAX DEPARTMENT INTERNALAUDITINGDIVISION

PO BOX 425

CHARLESTON, WEST VIRGINIA

FOR ASSISTANCE CALL:

(304)

INTERNET ADDRESS

http://www.state.wv.us/taxdiv

Form Specifications

| # | Fact |

|---|---|

| 1 | The WV/CST-250 form is an application for a direct pay permit for consumers sales and use tax in West Virginia. |

| 2 | Applicants must hold a valid Business Registration Certificate to apply. |

| 3 | Businesses cannot be delinquent on any taxes imposed by Chapter 11 of the West Virginia Code. |

| 4 | Eligible businesses include those in manufacturing, natural resource production, communication, public utilities, and more. |

| 5 | Applicants must describe their business activity within West Virginia. |

| 6 | The State Tax Commissioner authorizes direct pay permits under W.Va. Code § 11-15-9d. |

| 7 | Direct Pay Permit holders must notify vendors of their permit number and file returns monthly or quarterly. |

| 8 | A Direct Pay Permit cannot be used to purchase food, gasoline, or special fuel. |

| 9 | Permits are subject to cancellation for non-compliance, including failure to file returns on time. |

| 10 | Applications must be fully completed and approved by the West Virginia State Tax Department to be valid. |

Guide to Filling Out Wv Cst 250

When a business in West Virginia needs to manage its own sales and use taxes directly, the WV/CST-250 form becomes essential. Filling out this form accurately and entirely is the first step toward obtaining a Direct Pay Permit from the West Virginia State Tax Department. This permit allows businesses to bypass the usual route of paying these taxes through vendors and instead, handle these responsibilities directly with the state. This streamlined process, while beneficial, comes with its own set of obligations, such as notifying vendors of the permit and submitting regular tax returns. Below are the detailed steps to fill out the form correctly.

- Start by entering the West Virginia Account Identification Number of your business in the designated field.

- Write the Legal Business or Corporate Name as officially registered.

- If applicable, include the Owner’s Name (if it’s a sole proprietorship).

- Provide the Street Address, including City, State, & ZIP code, where the business operates.

- Enter the Name and Telephone Number of the person within the business who will act as the primary contact for the West Virginia State Tax Department.

- Certify your business's eligibility by ticking the checkboxes that apply to the nature and operation of your business. Options range from manufacturing to providing health care services, highlighting the diversity of businesses that can apply for this permit. Be prepared to describe your business activity in West Virginia in detail in the space provided.

- Under the declaration section, affirm the statement about not being delinquent on tax payments and other certifications as required. This includes confirming that the business holds a valid Business Registration Certificate and checking off applicable business conditions.

- The applicant must sign and date the form at the bottom. Also, clearly print or type the name and title (Owner, Partner, Officer of Corporation) of the applicant alongside their telephone number.

Upon completing the form, double-check all the information for accuracy and completeness. Then, mail the form to the address provided on the form itself, attention to the Internal Auditing Division of the West Virginia State Tax Department. After submission, keep an eye out for correspondence from the department regarding the status of your application. Remember, receiving a Direct Pay Permit entails maintaining meticulous records and timely tax return submissions. If approved, this permit will facilitate a more direct interaction with the state tax regulations, emphasizing the importance of staying diligent about tax-related duties and deadlines.

Things You Should Know About Wv Cst 250

What is the WV/CST-250 form and who needs it?

The WV/CST-250 form, also known as the Consumers Sales and Use Tax Application for Direct Pay Permit, is a document required for businesses in West Virginia that wish to pay consumer sales and use tax directly to the State Tax Department, instead of having vendors collect the tax. Businesses that engage in certain types of activities, such as manufacturing, providing public utilities, or engaging in research and development, may need to complete this form.

How does a direct pay permit benefit my business?

A direct pay permit allows your business to manage and report consumer sales and use taxes directly to the West Virginia State Tax Department. This can provide your business with more control over tax reporting and compliance, potentially streamline tax processes, and ensure accuracy in tax payments specific to the nature of your business operations.

What are the conditions that must be satisfied to be eligible for a direct pay permit?

To be eligible for a direct pay permit, your business must not be delinquent in any taxes imposed by Chapter 11 of the West Virginia Code. Additionally, it must fall into one or more specific categories, such as being engaged in manufacturing, public utilities, transportation, research and development, or operating as a health care provider purchasing specific medical goods, among others.

What are the responsibilities of a holder of a direct pay permit?

Holders of a direct pay permit have several responsibilities, including notifying each vendor about their permit and ensuring that tax will be paid directly to the Tax Commissioner, filing a Direct Pay Consumers Sales or Use Tax Return by the specified deadline, maintaining accurate books and records for inspection, and not using the permit to purchase food, gasoline, or special fuel.

How can I apply for a direct pay permit?

To apply for a direct pay permit, fully complete the WV/CST-250 form, ensuring all entries are filled. The form requires information about your business, such as the legal name, address, and the type of activity your business engages in within West Virginia. The application will then be reviewed by the West Virginia State Tax Department to determine eligibility.

What happens if my application for a direct pay permit is approved?

If your application is approved, you will receive a numbered Direct Pay Permit in the mail. This permit allows you to begin paying consumer sales and use taxes directly to the State Tax Department according to the conditions outlined.

What should I do if I don’t receive a Direct Pay Consumers Sales and Use Tax Return?

If you do not receive a Direct Pay Consumers Sales and Use Tax Return within 60 days after receiving your Direct Pay Permit, it is important to notify the West Virginia State Tax Department promptly to ensure compliance and avoid potential penalties.

Can a direct pay permit be cancelled or surrendered?

Yes, a direct pay permit can be either surrendered by the holder or cancelled by the State Tax Department. In such cases, the holder is required to promptly notify all relevant vendors, in writing, about the permit’s surrender or cancellation to avoid misunderstandings regarding tax collection obligations.

Common mistakes

Filling out the West Virginia CST-250 form, a direct pay permit application, can be a complex process, fraught with potential mistakes that can impede the approval process or the efficient use of the permit if granted. This document is designed to enable certain businesses to pay consumer sales and use tax directly to the West Virginia State Tax Department, bypassing the need for vendors to collect these taxes. Recognizing and avoiding common errors can streamline tax compliance and permit usage. Below are eight frequently made errors during the application process:

- Not completing all entries: The application explicitly states that it is not valid unless all entries are completed. A common mistake is leaving sections blank, which can lead to immediate rejection. The detail required underscores the department's need for comprehensive information to process the request adequately.

- Failing to ensure eligibility: The form outlines specific conditions under which a business can apply for a direct pay permit. Applicants sometimes overlook this section, assuming their business model fits without verifying against the listed criteria. This misstep can result in the rejection of the application.

- Incorrect business identification: Providing accurate identification details, including the West Virginia Account Identification Number and the Business Registration Certificate number, is paramount. Mistakes or inconsistencies in these identifiers can lead to delays or denial as it impedes the verification of the business’s standing and legitimacy.

- Delinquency on tax payments: Certification that the business is not delinquent on any tax payments imposed by Chapter 11 of the West Virginia Code is required. Applicants sometimes overlook or inaccurately assess their tax status, which can halt the application process if unresolved taxes are discovered.

- Not providing a detailed business description: The application requests a detailed description of the business activity within West Virginia. A vague or incomplete description can hinder the tax department’s ability to determine eligibility based on the business’s operations.

- Omission of signature and date: An often overlooked but critical error is failing to sign and date the application. This oversight can invalidate the entire application, as it is a necessary confirmation of the information’s accuracy and the applicant's authority.

- Misunderstanding the permit’s scope: The permit does not apply to the purchase of food, gasoline, or special fuel. Some applicants do not realize this limitation, which could lead to misuse of the permit if not properly understood.

- Lack of communication with vendors: Once the permit is granted, permit holders must notify all relevant vendors of their direct pay status and permit number. Failing to do so can result in the inappropriate collection of sales tax by vendors unaware of the direct pay arrangement.

The Direct Pay Permit process embodies a distinct responsibility: to accurately self-assess and remit taxes due directly to the state. Applicants should approach this application with the seriousness it demands, meticulously ensuring accuracy, completeness, and compliance with all specified requirements. Awareness of and attention to these common mistakes can facilitate a smoother application process, prevent unnecessary delays, and foster compliance with West Virginia tax obligations.

Documents used along the form

When applying for a Direct Pay Permit with the WV/CST-250 form, businesses often need to prepare and submit additional documents to support their application or comply with related tax regulations. Understanding these documents is crucial to ensure a thorough and compliant application process.

- Business Registration Certificate - This document serves as proof that the business is officially registered with the state of West Virginia, a prerequisite mentioned directly in the WV/CST-250 form.

- Tax Clearance Certificate - Indicates that the business is not delinquent on any state taxes, aligning with the statement of tax compliance required in the WV/CST-250 application.

- Annual Financial Statements - Reviewed or audited financial statements may be required to assess the financial health of the business and its ability to comply with tax obligations.

- Articles of Incorporation/Organization - For corporations or LLCs, these documents are needed to verify the legal status and structure of the business.

- Operating Agreement - If applicable, this document outlines the operations of the business and is often required for LLCs to provide further evidence of business operations.

- Board Resolution for Tax Matters - A resolution from the business’s board of directors that authorizes specific individuals to handle tax matters, including the application for a Direct Pay Permit.

- Vendor List - A comprehensive list of vendors from whom the business purchases tangible personal property or services, as the permit holder must notify vendors of their Direct Pay status.

- Use Tax Records - Historical use tax records may be reviewed to ensure previous taxes have been correctly assessed and paid, highlighting the applicant's compliance history.

- Monthly Sales Reports - These reports can sometimes be requested to present an overview of the regular business activities, supporting the need for a Direct Pay Permit.

- Copy of Previous Tax Returns - Including sales, use, and any other relevant state tax returns to demonstrate the applicant’s tax filing history and compliance.

The collection and preparation of these documents, in addition to the WV/CST-250 form, are fundamental steps toward ensuring a permitted business can direct pay its sales and use tax. Paying close attention to the requirements laid out by the West Virginia State Tax Department and providing thorough documentation will streamline the application process and facilitate compliance with state tax regulations.

Similar forms

The WV/CST-250 form, used for applying for a Direct Pay Permit in West Virginia, bears similarities to other tax and permit application documents, each serving a unique purpose within various jurisdictional frameworks. One such document is the Sales and Use Tax Exemption Certificate. This certificate is utilized by businesses to purchase goods or services intended for resale without paying sales tax at the point of purchase. Both forms require detailed business information, and the premise behind their use is to prevent double taxation -- once when the business purchases the goods and again when they sell the goods to the end consumer.

Another comparable document is the Business Registration Certificate application. This document is a prerequisite for operating legally within a state, serving to register a business with the state tax department and often with the secretary of state. Similar to the WV/CST-250, detailed business information and certification of compliance with state tax obligations are fundamental requirements. Both forms are vital steps in establishing a business’s legality and its compliance with state tax laws.

The Request for Taxpayer Identification Number and Certification, commonly known as Form W-9, also shares similarities with the WV/CST-250. While the W-9 is a federal form used primarily to provide a taxpayer identification number to entities that will pay them income, it similarly gathers details about the business or individual and their tax status. Like the WV/CST-250, the W-9 form is integral to ensuring tax compliance and facilitating proper tax reporting and withholding obligations.

The Application for Employer Identification Number (EIN), or Form SS-4, is another document akin to the WV/CST-250. This form is used to apply for an EIN, which is necessary for tax administration for employers, corporations, partnerships, and certain other entities. Both the SS-4 and the WV/CST-250 require detailed information about the entity applying for the number or permit, and both are centered around tax administrative procedures, albeit for different purposes and tax types.

Lastly, the State Contractor’s License Application mirrors the WV/CST-250 in the sense that both are forms entailing stringent disclosure of business operations, ownership, and compliance information for regulatory purposes. While the Contractor’s License Application is more specific to construction or trade businesses seeking authorization to operate within a state, it similarly emphasizes the business’s obligation to adhere to state laws and regulations, akin to tax compliance in the WV/CST-250 form.

Dos and Don'ts

Filling out the WV CST-250 form accurately and thoroughly is crucial for businesses looking to apply for a Direct Pay Permit in West Virginia. To assist with this process, here’s a compiled list of best practices to follow and common mistakes to avoid.

Things You Should Do:

Ensure that all entries on the form are completed. An incomplete application is not considered valid and will lead to delays or rejection.

Double-check the accuracy of the business’s legal name, West Virginia account identification number, and other essential details to avoid processing delays.

Provide a detailed description of your business activity within West Virginia, as this information helps in the assessment of your eligibility for a Direct Pay Permit.

Sign and date the application. The application must be signed by an owner, partner, or officer of the corporation, certifying that the information provided is true, correct, and complete.

Review the conditions and requirements associated with holding a Direct Pay Permit, such as notifying vendors and maintaining records, to ensure compliance.

Things You Shouldn't Do:

Do not leave any sections blank. If certain sections do not apply to your business, indicate this appropriately instead of skipping them.

Avoid guessing or estimating information. Ensure that all data provided on the form is accurate and up-to-date.

Do not ignore the application’s instructions. Following the guidelines can expedite the approval process.

Refrain from using the Direct Pay Permit to purchase items such as food, gasoline, or special fuel, as these are not covered under the permit’s use.

Do not neglect to notify the West Virginia State Tax Department if you do not receive a Direct Pay Consumers Sales and Use Tax Return within sixty (60) days after receiving your Direct Pay Permit.

By following these guidelines, businesses can navigate the application process more smoothly and ensure they meet all requirements for obtaining and maintaining a Direct Pay Permit in West Virginia.

Misconceptions

Misconceptions about the WV CST-250 form, the application for a Direct Pay Permit in West Virginia, abound. Often, applicants enter the process with incorrect assumptions that can lead to confusion or errors. Here’s a list of common misconceptions and the truths behind them.

It’s only for big corporations: Many assume the WV CST-250 is exclusively for large businesses. However, it’s also available to any business, including small operations that meet specific criteria like engaging in manufacturing or providing public utility services.

Application approval is guaranteed: Completing the application doesn’t ensure you will receive a Direct Pay Permit. The State Tax Department reviews each application to determine eligibility based on several factors listed on the form.

It’s complicated to apply: While the form requires detailed information, if you carefully follow the instructions and provide accurate responses, the application process is straightforward.

Direct Pay Permits cover all purchases: Contrary to this belief, certain items like food, gasoline, and special fuel cannot be purchased using a Direct Pay Permit as highlighted on the form.

Once obtained, it’s valid indefinitely: While there’s no specified expiration date, the permit remains valid as long as you comply with all requirements. It can be cancelled or surrendered if conditions change.

Filing returns is optional: Permit holders are required to file Direct Pay Consumers Sales or Use Tax Returns monthly or quarterly. Not filing by the due date can result in interest, penalties, and potentially cancellation of the permit.

You can wait to inform the WV State Tax Department about issues with your Direct Pay Permit: If your permit number changes or if you haven’t received your return forms, it’s crucial to notify the Tax Department promptly, not whenever you choose to.

Approval is immediate: Approval for a Direct Pay Permit can take some time as the Tax Department must review your application thoroughly. It’s a process that requires patience.

Understanding the realities of the WV CST-250 and the Direct Pay Permit process can set the right expectations and help avoid unnecessary hurdles. With accurate information and adherence to the stipulations, businesses can navigate the process more smoothly.

Key takeaways

Understanding the West Virginia CST-250 form is crucial for businesses operating within the state, especially those who wish to pay consumer sales and use tax directly to the state tax department. Below are eight key takeaways related to the completion and use of the WV CST-250 form:

- The WV CST-250 form serves as an application for businesses desiring to obtain a Direct Pay Permit, allowing them to pay consumers sales and/or use tax directly to the West Virginia State Tax Department.

- Businesses eligible for a Direct Pay Permit include those involved in manufacturing, producing natural resources, communication, public utility services, and several other specified activities within West Virginia.

- An essential prerequisite for applying for a Direct Pay Permit is having a valid Business Registration Certificate and being current on all tax payments as mandated by Chapter 11 of the West Virginia Code.

- The application mandates the disclosure of detailed business activities conducted within West Virginia, underscoring the significance of providing a comprehensive business description.

- Upon receiving a Direct Pay Permit, the holder must notify all vendors of their permit number and the arrangement to pay the tax directly to the Tax Commissioner, including any subsequent changes to the permit number.

- Permit holders are obliged to file a Direct Pay Consumers Sales or Use Tax Return by the 20th day of the month following the month or quarter of the transaction, with late filings subject to interest and penalties.

- There are restrictions on the use of the Direct Pay Permit; specifically, it cannot be used to purchase food, gasoline, or special fuel.

- It's important for permit holders to maintain accurate records, including books and invoices, for review by the West Virginia State Tax Department, reflecting the department’s emphasis on compliance and record-keeping.

Lastly, should a business's Direct Pay Permit be surrendered or canceled, prompt notification to vendors is required, underscoring the importance of clear communication between permit holders and their suppliers or service providers. This mechanism ensures a coherent flow of tax payment responsibilities directly from the business to the state.

Popular PDF Forms

Courtswv - Provides a structured process for West Virginia employers to receive tax incentives when hiring military individuals, with the WV/MIP-31 voucher.

Wv It 104 - Specifies the documentation and calculation needed to accurately report and withhold taxes due on nonresident real estate transactions.

West Virginia Business License - Business owners and their authorized representatives must sign the GSR-01 form, verifying their identity and entitlement to the requested information.