Free Wv Cst 280 Form

In navigating the complexities of taxation within West Virginia, understanding the provisions of the WV/CST-280 Exemption Certificate becomes crucial for entities aiming to conduct tax-exempt transactions. The form is designed to ensure that certain purchases of tangible personal property or taxable services, which are not normally exempt from tax, can qualify for a tax-exempt status under specific conditions outlined in the guidelines. This exemption encompasses a variety of situations, including purchases made for resale, by exempt commercial agricultural producers, tax-exempt organizations such as government agencies, non-profit organizations, schools, and churches, as well as specific service and tangible personal property acquisitions like electronic data processing services and aircraft maintenance services. The meticulous completion of this form is necessary for the purchaser to certify their eligibility for the exemption, detailing their claim and providing the requisite business and tax identification numbers. Important too is the understanding that this certificate cannot be used for the purchase of gasoline or special fuel, emphasizing the legal boundaries set by the state of West Virginia. Furthermore, the form serves as a reminder of the responsibilities borne by the purchaser, including the consequences of misuse or fraudulent claims, which could result in penalties, interest, and the potential revocation of a Business Registration Certificate. It underscores the importance of compliance with state tax laws and the diligent documentation required to substantiate tax-exempt transactions.

Wv Cst 280 Example

|

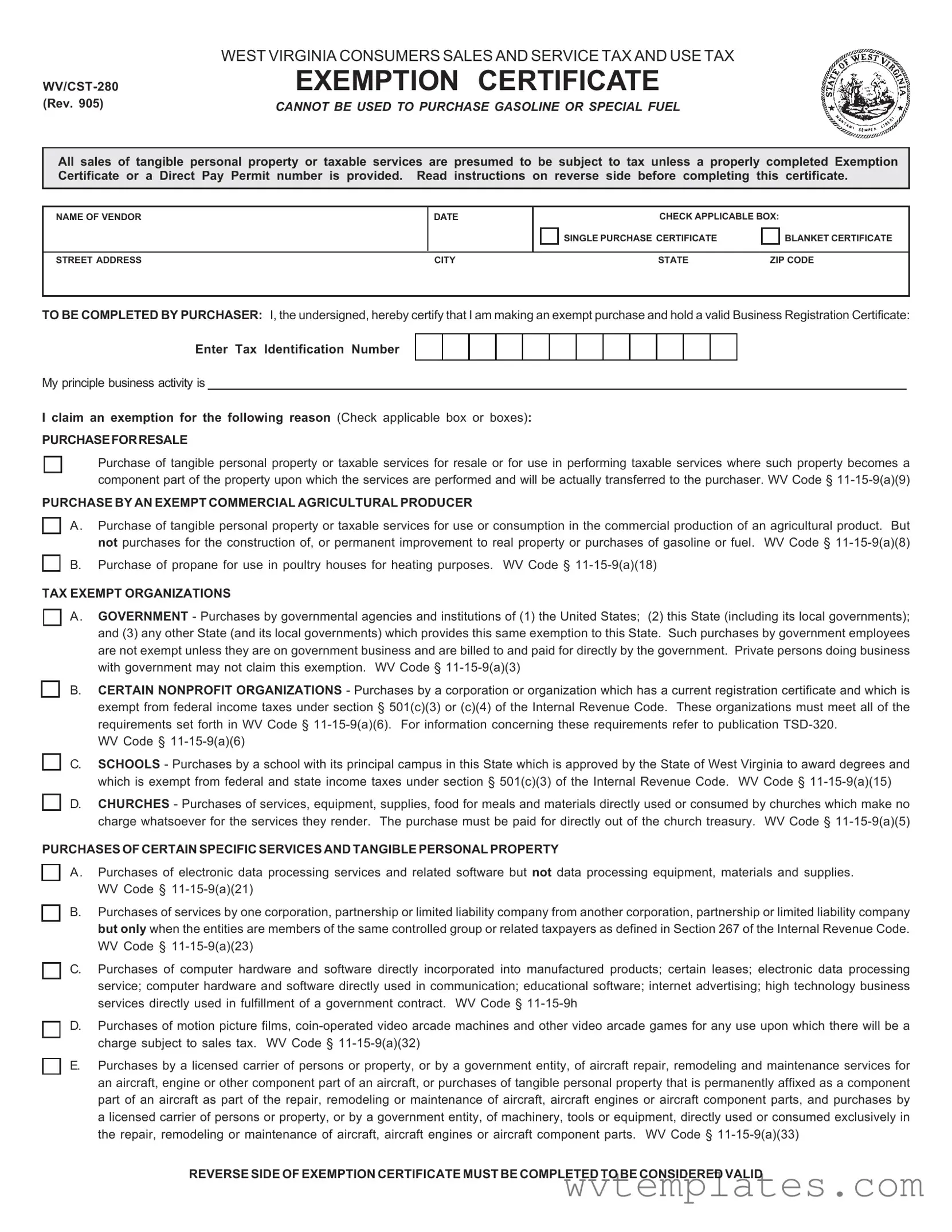

WEST VIRGINIA CONSUMERS SALES AND SERVICE TAX AND USE TAX |

EXEMPTION CERTIFICATE |

|

(Rev. 905) |

CANNOT BE USED TO PURCHASE GASOLINE OR SPECIAL FUEL |

All sales of tangible personal property or taxable services are presumed to be subject to tax unless a properly completed Exemption Certificate or a Direct Pay Permit number is provided. Read instructions on reverse side before completing this certificate.

NAME OF VENDOR

DATE

CHECK APPLICABLE BOX:

SINGLE PURCHASE CERTIFICATE

BLANKET CERTIFICATE

STREET ADDRESS |

CITY |

STATE |

ZIP CODE |

TO BE COMPLETED BY PURCHASER: I, the undersigned, hereby certify that I am making an exempt purchase and hold a valid Business Registration Certificate:

Enter Tax Identification Number

My principle business activity is

I claim an exemption for the following reason (Check applicable box or boxes):

PURCHASEFORRESALE

Purchase of tangible personal property or taxable services for resale or for use in performing taxable services where such property becomes a component part of the property upon which the services are performed and will be actually transferred to the purchaser. WV Code §

PURCHASE BY AN EXEMPT COMMERCIAL AGRICULTURAL PRODUCER

A. Purchase of tangible personal property or taxable services for use or consumption in the commercial production of an agricultural product. But not purchases for the construction of, or permanent improvement to real property or purchases of gasoline or fuel. WV Code §

B. Purchase of propane for use in poultry houses for heating purposes. WV Code §

TAX EXEMPT ORGANIZATIONS

A. GOVERNMENT - Purchases by governmental agencies and institutions of (1) the United States; (2) this State (including its local governments); and (3) any other State (and its local governments) which provides this same exemption to this State. Such purchases by government employees are not exempt unless they are on government business and are billed to and paid for directly by the government. Private persons doing business with government may not claim this exemption. WV Code §

B. CERTAIN NONPROFIT ORGANIZATIONS - Purchases by a corporation or organization which has a current registration certificate and which is exempt from federal income taxes under section § 501(c)(3) or (c)(4) of the Internal Revenue Code. These organizations must meet all of the requirements set forth in WV Code §

WV Code §

C. SCHOOLS - Purchases by a school with its principal campus in this State which is approved by the State of West Virginia to award degrees and which is exempt from federal and state income taxes under section § 501(c)(3) of the Internal Revenue Code. WV Code §

D. CHURCHES - Purchases of services, equipment, supplies, food for meals and materials directly used or consumed by churches which make no charge whatsoever for the services they render. The purchase must be paid for directly out of the church treasury. WV Code §

PURCHASES OF CERTAIN SPECIFIC SERVICES AND TANGIBLE PERSONAL PROPERTY

A. Purchases of electronic data processing services and related software but not data processing equipment, materials and supplies. WV Code §

B. Purchases of services by one corporation, partnership or limited liability company from another corporation, partnership or limited liability company but only when the entities are members of the same controlled group or related taxpayers as defined in Section 267 of the Internal Revenue Code. WV Code §

C. Purchases of computer hardware and software directly incorporated into manufactured products; certain leases; electronic data processing service; computer hardware and software directly used in communication; educational software; internet advertising; high technology business services directly used in fulfillment of a government contract. WV Code §

D. Purchases of motion picture films,

E. Purchases by a licensed carrier of persons or property, or by a government entity, of aircraft repair, remodeling and maintenance services for an aircraft, engine or other component part of an aircraft, or purchases of tangible personal property that is permanently affixed as a component part of an aircraft as part of the repair, remodeling or maintenance of aircraft, aircraft engines or aircraft component parts, and purchases by a licensed carrier of persons or property, or by a government entity, of machinery, tools or equipment, directly used or consumed exclusively in the repair, remodeling or maintenance of aircraft, aircraft engines or aircraft component parts. WV Code §

REVERSE SIDE OF EXEMPTION CERTIFICATE MUST BE COMPLETED TO BE CONSIDERED VALID

I understand that this certificate may not be used to make tax free purchases of items or services which are not for an exempt purpose and that I will pay the Consumers Sales or Use Tax on tangible personal property or services purchased pursuant to this certificate and subsequently used or consumed in a taxable manner. In addition, I understand that I will be liable for the tax due, plus substantial penalties and interest, for any erroneous or false use of this certificate.

NAME OF PURCHASER |

STREET ADDRESS |

|

|

|

|

SIGNATURE OF OWNER, PARTNER, OFFICER OF CORPORATION, ETC. |

CITY |

|

|

|

|

TITLE |

STATE |

ZIP CODE |

|

|

|

GENERALINSTRUCTIONS

An Exemption Certificate may be used only to claim exemption from tax upon a purchase of tangible personal property or services which will be used for an exempt purpose as stated on the front of this form.

ApurchasermayfileablanketExemptionCertificatewiththevendortocoveradditionalpurchasesofthesamegeneraltypeofproperty or service. However, each subsequent sales slip or purchase invoice evidencing a transaction covered by a blanket Exemption Certificate must show the purchaser’s name, address and Business Registration Certificate Number for purposes of certification.

INSTRUCTIONSFORPURCHASER

To purchase tangible personal property or services tax exempt, you must possess a valid Business Registration Certificate and you must properly complete this Exemption Certificate and present it to your supplier. To be properly completed, all entries on this Exemption Certificate must be filled in.

Your Business Registration Certificate (and any duplicates) may be suspended or revoked if you or someone acting on your behalf willfully issues this certificate for the purpose of making a tax exempt purchase of tangible personal property and/or services that is not used in a tax exempt manner (as stated on the front of this form).

When property or services are purchased tax exempt with an Exemption Certificate, but later used or consumed in a non exempt manner, the purchaser must pay Sales or Use Tax on the purchase price.

The willful issuance of a false or fraudulent Exemption Certificate with the intent to evade Sales or Use Tax is a misdemeanor.

Your misuse of this Certificate with intent to evade the Sales or Use Tax shall also result in your being subject to:

A penalty of fifty percent of the tax that would have been due

had there not been a misuse of such certificate.

This is in addition to any other penalty imposed by the Law.

In the event you make false or fraudulent use of this Certificate with intent to evade the tax, you may be assessed for the tax at any time subsequent to such use.

INSTRUCTIONSFORVENDOR

At the time the property is sold or the service is rendered, you must obtain from your customer this Certificate, properly completed, (or a Direct Pay Permit number issued by the West Virginia Department of Tax and Revenue), or the sale will be deemed a taxable sale, unless the property or service sold is exempt per se from Sales Tax. Your failure to collect tax on such taxable sale will make you personally liable for the tax, plus penalties and interest.

Additionalinformationmayberequiredtosubstantiatethatthesalewasforexemptpurposes. InorderforthisCertificatetobeproperly completed, it must be issued by a purchaser who has a valid Business Registration Certificate and must have all entries completed by the purchaser.

A timely received certificate which contains a material deficiency will be considered satisfactory if such deficiency is subsequently corrected.

You must keep this certificate for at least three years after the due date of the last return to which it relates, or the date when such return was filed, if later.

You must maintain a reasonable method of associating a particular exempt sale to a customer with the Exemption Certificate you have on file for such customer.

INSTRUCTIONSFORVENDORANDPURCHASER

If you, as vendor or as a purchaser, engage in any business activity in West Virginia without possessing a valid Business Registration Certificate (and you do not clearly qualify for an exemption), you shall be subject to a penalty in an amount not exceeding $100 for the first day on which such sales or purchases are made, plus an amount not exceeding $100 for each subsequent day on which such sales or purchases are made.

Please begin using this Certificate immediately.

Form Specifications

| Fact | Detail |

|---|---|

| Form Name and Revision | WV/CST-280 Exemption Certificate (Rev. 905) |

| Purpose | To certify purchases exempt from West Virginia Consumers Sales and Service Tax and Use Tax. |

| Exclusions | Cannot be used for the purchase of gasoline or special fuel. |

| Governing Laws | Variety of WV Codes including but not limited to §§ 11-15-9(a)(3), 11-15-9(a)(5), 11-15-9(a)(6), 11-15-9(a)(8), and 11-15-9(a)(9). |

| Proper Use | All entries must be completed; misuse or fraudulent use of the certificate can lead to penalties, interest, and misdemeanor charges. |

Guide to Filling Out Wv Cst 280

Filling out the WV/CST-280 Exemption Certificate correctly is crucial for vendors and purchasers looking to document tax-exempt transactions in West Virginia. This form is designed to certify that purchases of tangible personal property or taxable services are exempt from the state's Consumers Sales and Service Tax and Use Tax under specific conditions. To ensure compliance and avoid potential penalties, it's important to follow each step conscientiously and provide accurate information. Here are the steps to properly complete the WV/CST-280 form.

- Start by entering the name of the vendor from whom the purchase is being made at the top of the form.

- Fill in the date of the transaction next to the vendor's name.

- Choose the type of certificate you are issuing: either a "Single Purchase Certificate" or a "Blanket Certificate." Mark the appropriate box.

- Under the vendor's information, provide the street address, city, state, and ZIP code of the vendor.

- In the section titled "TO BE COMPLETED BY PURCHASER," begin by entering the purchaser’s Tax Identification Number and describing the principal business activity.

- Select the specific exemption reason that applies to your purchase. You must check the appropriate box next to the reason that best describes the nature of your tax-exempt purchase.

- Fill in the name of the purchaser, which could be an individual or a company, depending on the situation.

- Provide the purchaser’s street address, city, state, and ZIP code.

- The certificate must be signed by the owner, partner, officer of the corporation, or equivalent position. Include the title of the person signing the certificate next to their signature.

- Review the filled form for any errors or missing information as inaccurate completion could lead to penalties.

Once you’ve completed these steps, the form is ready for submission. Keep in mind that providing false information or improperly using this certificate to evade sales or use tax can result in significant penalties, including but not limited to, paying the tax due along with additional fines. Vendors should retain a copy of the completed form for a minimum of three years for record-keeping and compliance purposes. Similarly, purchasers should keep a copy of the form to support their claim of tax exemption under the stipulated reasons in case of future audits or inquiries.

Things You Should Know About Wv Cst 280

What is the WV/CST-280 Exemption Certificate?

The WV/CST-280 Exemption Certificate is a form used in West Virginia to claim exemption from consumers sales and service tax and use tax on purchases of tangible personal property or services. It must be properly completed and provided at the time of purchase. This certificate cannot be used for the purchase of gasoline or special fuel.

Who can use the WV/CST-280 form?

This form can be used by businesses holding a valid Business Registration Certificate in West Virginia. It is also available to certain other groups, including exempt commercial agricultural producers, tax-exempt organizations, schools, churches, and purchasers of specific services and tangible personal property that meet the criteria laid out in the form.

Are there different types of exemption certificates?

Yes, the form allows for two types: a Single Purchase Certificate for one-time use and a Blanket Certificate for ongoing purchases of the same general type of property or service from a vendor.

How does a business qualify to use the Exemption Certificate?

To qualify, a business must have a valid Business Registration Certificate and the purchase must be for an exempt purpose as stated on the WV/CST-280 form. Additionally, all entries on the Exemption Certificate must be properly completed.

Can this certificate be used for any type of purchase?

No, the certificate cannot be used for purchases of gasoline or special fuel. It is also specifically indicated that purchases must be for exempt purposes, such as for resale, direct use in agricultural production, by tax-exempt organizations, and for other specified uses outlined on the form.

What responsibilities do purchasers have when using this certificate?

Purchasers are responsible for ensuring that all the information filled out on the certificate is accurate and that the purchases made are for qualified exempt purposes. If an item or service purchased tax-exempt is later used in a way that is not exempt, the purchaser must pay the applicable Sales or Use Tax. Misuse of the certificate could result in liability for the tax owed, substantial penalties, and interest.

What are the responsibilities of vendors when accepting an exemption certificate?

Vendors are required to obtain a properly completed exemption certificate at the time of the sale or the service rendered. If a sale is later deemed taxable due to an improper exemption claim, the vendor could be held personally liable for the tax, plus penalties and interest. Vendors must keep the certificate for at least three years after the due date of the last return or the date the return was filed, whichever is later.

Can penalties be applied for the misuse of the Exemption Certificate?

Yes, both purchasers and vendors misusing the Exemption Certificate may be liable for the tax due on non-exempt purchases, along with a penalty of fifty percent of the tax that would have been due, additional penalties imposed by law, and interest. Issuing a false or fraudulent Exemption Certificate with intent to evade tax is considered a misdemeanor.

Where can more information about the WV/CST-280 Exemption Certificate be found?

For more detailed information about the Exemption Certificate and its proper use, refer to publication TSD-320 or contact the West Virginia Department of Tax and Revenue. They provide guidance on the requirements set forth for tax-exempt purchases and offer assistance in completing and submitting the certificate correctly.

Common mistakes

The process of completing the WV CST-280 Exemption Certificate, vital for businesses and organizations making tax-exempt purchases in West Virginia, is nuanced, and errors can lead to delayed approvals or even penalties. By avoiding common mistakes, entities can ensure their applications are processed smoothly and efficiently.

One of the primary errors involves incomplete information. Every section of the WV CST-280 form requires attention. Leaving any area blank, especially those related to the business's Tax Identification Number or specific reasons for tax exemption, can render the certificate invalid. These details are crucial for the West Virginia Department of Revenue to confirm the eligibility for tax exemption.

- Incorrect identification of the type of certificate needed—whether a single purchase certificate or a blanket certificate—is another frequent misstep. Choosing the wrong type can complicate future transactions and might require the submission of additional documentation.

- Often, entities mistakenly declare an incorrect exemption category for their purchase. Identifying the precise nature of the exemption, such as whether it's for resale or specific to tax-exempt organizations, is essential for compliance with state tax laws.

- Another error is failing to specify the primary business activity accurately. This information helps the tax authorities understand the context of the exemption request and verify its legitimacy.

- Signatory issues also arise when the individual signing the form does not have the authority to do so or fails to include their title and relation to the entity, complicating the form's legal standing.

- Lastly, a common oversight is not reviewing the reverse side of the certificate for additional instructions or requirements. This section often contains vital information that can affect the validity of the exemption.

While it may seem straightforward, the WV/CST-280 requires careful attention to detail. For vendors and purchasers alike, ensuring the accurate and complete submission of this form is integral to maintaining compliance and securing tax-exempt status for eligible transactions. This not only streamlines the purchasing process but also safeguards against unnecessary tax liabilities and penalties.

To avoid these mistakes and ensure a smoother process, purchasers should thoroughly review the instructions provided with the form, consult with tax professionals if necessary, and maintain open communication with vendors about the specific requirements for each tax-exempt purchase. By doing so, organizations can more effectively manage their tax obligations and maintain focus on their primary missions and business goals.

Documents used along the form

When handling the West Virginia Consumers Sales and Service Tax and Use Tax Exemption Certificate (WV/CST-280), it is crucial to be aware of various other forms and documents that are often used alongside it. These forms collectively ensure compliance with tax laws while maximizing operational efficiency. They cater to various exemptions, registrations, and verifications required for a smooth transaction process within West Virginia.

- Business Registration Certificate: This is essential for any business to operate legally within West Virginia. It verifies the business's eligibility for making tax-exempt purchases when applicable.

- Direct Pay Permit: Used by businesses that prefer to pay sales or use tax directly to the state rather than through vendors. It accompanies the WV/CST-280 to specify arrangements for direct tax payment.

- Sales and Use Tax Return (WV/CST-200CU): Filed periodically by businesses, this documents taxable and exempt sales and calculates the tax due or refundable for both sales and use tax.

- Application for Sales Tax Exemption for Purchases for Resale (Form WV/CST-283): Specifically designed for businesses purchasing goods or services for resale, this form supports the exemption claim on such purchases.

- Special Fuel Excise Tax Return (WV/MFT-200): Required for businesses involved in the purchase, sale, or use of special fuels, detailing the taxes due on these transactions.

- Consumer Sales and Service Tax and Use Tax Certificate of Capital Improvement (Form CST-280CI): Utilized when purchasing materials or services for capital improvements, certifying that the purchase is tax-exempt when applicable.

- Agricultural Certificate for Sales and Use Tax Exemption (Form F0003): Offers tax exemptions on purchases related to agricultural production, echoing some exemptions mentioned in the WV/CST-280.

- Streamlined Sales and Use Tax Agreement Certificate of Exemption: For use in multiple states, including West Virginia, this form simplifies the exemption process for businesses operating in participating states.

- Exemption Certificate for Government Purchases (Form WV/CST-284): Applied when government agencies make exempt purchases, ensuring that such transactions are in line with West Virginia tax laws.

Each of these documents plays a vital role in maintaining tax compliance and managing financial operations efficiently. Businesses should familiarize themselves with these forms to understand their obligations and rights under West Virginia tax law. Utilizing these forms correctly ensures a smooth operation, preventing potential legal hurdles and financial penalties.

Similar forms

The Unified Sales & Use Tax Exemption/Resale Certificate - Multijurisdiction form serves a similar purpose to the WV/CST-280 form, facilitating tax-exempt purchases across multiple states for resale or other exempt purposes. Like the WV/CST-280, this multi-state form requires the purchaser to assert a tax-exempt status, either for resale or for consumption in a manner consistent with the state's tax code exemptions. The main distinction lies in its broad applicability across participating states, streamlining the process for businesses operating in multiple jurisdictions.

The Streamlined Sales and Use Tax Agreement Certificate of Exemption is another document closely related to the WV/CST-280. It aims to simplify sales and use tax collection and administration for businesses, much like the WV/CST-280 does within West Virginia. This document allows businesses to make tax-exempt purchases or sales across states that have adopted this Agreement, focusing on ensuring compliance with the simplified tax structures under the Streamlined Sales and Use Tax Agreement (SSUTA).

The Nonprofit Organization Unrelated Business Income Tax Return bears resemblance to the WV/CST-280 in the sense that both address tax exemption under specific conditions. While the WV/CST-280 form is for exempt purchases, the Nonprofit organization return focuses on income earned from activities unrelated to their tax-exempt purpose, underscoring the nuanced landscape of tax exemptions for different activities and entities.

Agricultural Exemption Certificates in various states share the purpose with that section of the WV/CST-280 focusing on exemptions for agricultural producers. These certificates allow farmers and agricultural producers to purchase goods and services tax-free when they're used in the production of agricultural products, reflecting how both documents facilitate tax relief following a similar principle, albeit tailored to the agricultural sector.

The Governmental Agencies Exemption Certificate parallels the WV/CST-280 in its provision for tax-exempt purchases by government entities. Both documents ensure that governmental purchases, under specific situations, are not burdened by sales tax, respecting the inter-governmental agreements and policies that exempt government purchases from taxation within certain parameters.

Direct Pay Permit applications, available in certain states, offer businesses the ability to pay sales and use taxes directly to the state rather than to vendors, akin to a specific aspect of the WV/CST-280 that allows for direct, tax-exempt purchases under certain conditions. Both mechanisms provide businesses with a way to manage their tax liabilities more directly and efficiently, albeit through different administrative processes.

Vendor’s License forms, which are required for businesses to collect and remit sales tax on taxable sales, indirectly relate to the WV/CST-280. While the latter facilitates tax-exempt purchases under certain conditions, Vendor’s License forms operate on the premise of taxable transactions, thus outlining the broad spectrum of tax administration from exempt purchases to the collection of taxes on sales.

The Use Tax Payment form for out-of-state purchases mimics a part of the WV/CST-280’s functionality, allowing taxpayers to report and pay taxes on items bought outside their jurisdiction for use within. Although the Use Tax Payment form deals with tax payments rather than exemptions, it addresses the same fundamental principle of ensuring proper tax collection on goods and services consumed within a jurisdiction.

Resale Certificates serve an analogous purpose to the WV/CST-280 by allowing businesses to purchase goods tax-free when the intention is to resell them. Both documents are critical for businesses in maintaining tax compliance while avoiding the burden of sales tax on transactions ultimately subject to tax upon their final sale to a consumer.

The Charitable Organization’s Tax Declaratory Judgement forms, similar to the tax-exempt section for nonprofit organizations in the WV/CST-280, are used by charities to establish their right to exemption from sales and use taxes under specific conditions. While focusing on a narrower beneficiary group, both forms are essential tools for qualifying organizations to navigate tax laws without compromising their financial stability.

Dos and Don'ts

When filling out the WV CST-280 form, understanding the dos and don'ts can streamline the process, ensuring that your transactions are tax exempt where applicable. Here’s a guide to help you navigate the form accurately.

Dos:

- Ensure all information is complete and accurate: Before submitting, double-check that all required fields are filled in, including your Tax Identification Number and the specific exemption reason. Incomplete forms may be considered invalid.

- Understand the specific exemptions: Familiarize yourself with the different types of exemptions listed on the form. This knowledge will help you select the correct exemption category for your purchase, ensuring compliance with West Virginia tax laws.

- Keep a copy for your records: After completion, make a copy of the form for your records. This is crucial for maintaining proper documentation in case of audits or questions regarding your tax-exempt purchases.

- Provide proof of eligibility for the exemption claimed: Be prepared to support your claim with appropriate documentation or evidence that validates your exemption status, such as a Business Registration Certificate.

Don'ts:

- Don't use the form for non-qualifying purchases: The form explicitly states that it cannot be used for purchasing gasoline or special fuel. Ensure your purchases qualify for exemption under the categories provided.

- Don't leave sections incomplete: Each section of the form must be completed to validate the exemption. Missing information can result in the rejection of your exemption claim.

- Don't falsify information: Providing incorrect information or claiming an exemption under false pretenses is not only unethical but may also subject you to penalties, interest, and misdemeanor charges.

- Don't assume the form covers all tax-exempt purchases: Even with a valid exemption, certain purchases may still be liable for sales or use tax under West Virginia laws. Always refer to the most current tax regulations to ensure compliance.

By following these guidelines, you can effectively manage your tax-exempt purchases, avoid common pitfalls, and ensure compliance with West Virginia tax laws.

Misconceptions

Many people have misconceptions about the West Virginia Consumers Sales and Service Tax and Use Tax Exemption Certificate (WV/CST-280). Here's a list of the top 10 misconceptions and the facts to correct them.

It's only for big businesses: This form can be used by businesses of all sizes that meet the requirements for tax-exempt purchases, not just large corporations.

You can use it for any purchase: The WV/CST-280 cannot be used for purchasing gasoline or special fuel, and it is specifically designed for certain tax-exempt purchases outlined by West Virginia law.

It grants permanent exemption: There are two types of certificates - Single Purchase and Blanket. The Single Purchase Certificate is for one-time use, while the Blanket Certificate covers ongoing qualifying purchases.

Approval is automatic: The completion and submission of WV/CST-280 do not guarantee tax exemption. Purchases must meet specific criteria and be properly documented.

It covers all taxes: The certificate only applies to Consumers Sales and Service Tax and Use Tax. Other taxes may still apply to the purchase.

Nonprofits don't need it: Even tax-exempt organizations, like those holding 501(c)(3) or (c)(4) designations, must properly complete and submit the form for eligible tax-exempt purchases.

Any church purchase is covered: Churches are eligible for exemptions, but the purchases must be directly used or consumed by the church and paid for directly out of the church treasury.

Personal use items can be exempt: Items or services purchased for personal use, even by eligible individuals or entities, are not covered by this exemption certificate.

You don't need a Business Registration Certificate: A valid Business Registration Certificate is a prerequisite for using the WV/CST-280 form to make tax-exempt purchases.

There are no consequences for misuse: Incorrect or fraudulent use of the certificate can result in being liable for the tax due, plus significant penalties and interest, and potential legal action.

Understanding the correct use and limitations of the West Virginia CST-280 Exemption Certificate ensures compliance with state tax laws and helps avoid accidental misuse or penalties.

Key takeaways

Filling out and using the West Virginia CST-280 Exemption Certificate is an important process for businesses and organizations that qualify for tax-exempt purchases in West Virginia. Here are five key takeaways about this form:

- Validity of the Exemption: The CST-280 form is essential for purchasers who want to buy tangible personal property or taxable services tax-free, under specific exemptions recognized by West Virginia law. This form cannot be used to purchase gasoline or special fuel.

- Necessity of a Business Registration Certificate: To use the CST-280 form, a purchaser must hold a valid Business Harrison Certificate. This requirement underscores the importance of maintaining valid state business registrations and documents for tax-exempt transactions.

- Selection Between Single Purchase and Blanket Certificate: The form allows for the designation of the exemption certificate as either a Single Purchase Certificate or a Blanket Certificate. This choice provides flexibility depending on whether the exemption is for a one-time purchase or for multiple purchases over time.

- Exemption Categories: The CST-280 form lists specific categories under which purchases can be exempt from sales tax. These include purchases for resale, by exempt organizations like schools and churches, agricultural producers, and for specific services and tangible personal property, among others. Understanding these categories can help entities correctly apply for exemptions.

- Penalties for Misuse: There are significant penalties for the misuse of this certificate, including a 50% penalty of the tax that would have been due, plus additional penalties and interest. This highlights the importance of understanding and accurately applying for exemptions only for eligible purposes.

In summary, the CST-280 Exemption Certificate is a critical tool for eligible businesses and organizations in West Virginia to purchase goods and services tax-free, when applicable. However, understanding the proper use and restrictions of this form is essential to avoid penalties and ensure compliance with tax laws.

Popular PDF Forms

Wv Withholding Form - Includes a certification by the employee to adhere to legal exemption limits under penalty of law.

Wv Employee Withholding Form - Helps taxpayers to manage their cash flow more effectively by estimating and paying taxes in advance.

Credentialing Documents - This form serves as a key step in the credentialing process, asking for academic, training, and professional practice details to assess qualifications and competencies.