Free Wv Nrsr Form

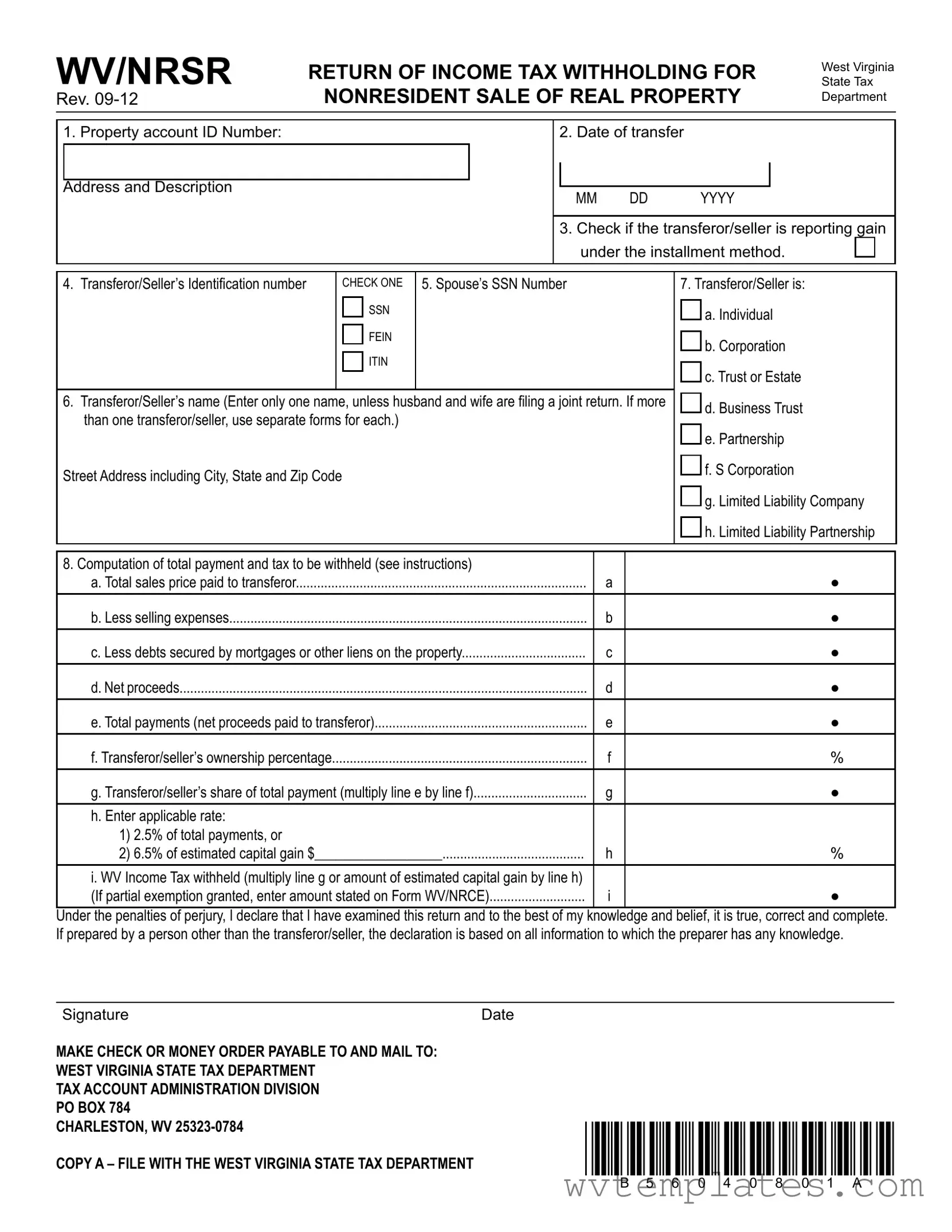

The WV/NRSR Return of Income Tax Withholding for Nonresident Sale of Real Property is a critical document that plays a pivotal role in the sale or transfer of real estate by nonresidents in West Virginia. Designed to ensure the timely collection of income tax due from nonresident sellers, this form facilitates a smooth transaction process by clearly outlining the financial responsibilities associated with the sale. Key elements of the WV/NRSR form include the identification of the property through its account ID number, the date of transfer, and detailed information regarding the computation of total payment and the amount of tax to be withheld. Sellers need to indicate their status, ranging from individuals to various types of business entities, and calculate the sales price, expenses, and net proceeds to determine the applicable tax rate and the total income tax withheld. It is essential for each party involved, including the transferor/seller and the entity responsible for closing, to accurately complete their respective sections to comply with West Virginia's state tax requirements. Furthermore, the form serves as a declaration under the penalties of perjury, ensuring that the information provided is true, correct, and complete to the best of the preparer's knowledge. This calculated approach to tax withholding for nonresident sellers underscores the importance of adhering to legal and financial protocols to facilitate a transparent and compliant real estate transaction in West Virginia.

Wv Nrsr Example

WV/NRSR |

RetuRN of iNcome tax WithholdiNg foR |

Rev. |

NoNReSideNt Sale of Real pRopeRty |

West Virginia

State Tax

Department

|

1. Property account ID Number: |

|

|

|

|

|

2. Date of transfer |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address and Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MM |

DD |

|

|

YYYY |

|||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Check if the transferor/seller is reporting gain |

||||||||

|

|

|

|

|

|

|

|

under the installment method. |

|

|

|||||

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

4. Transferor/Seller’s Identiication number |

|

CheCk one |

5. Spouse’s SSN Number |

|

|

7. Transferor/Seller is: |

||||||||

|

|

|

|

SSn |

|

|

|

|

|

|

|

a. Individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

FeIn |

|

|

|

|

|

|

|

b. Corporation |

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ITIn |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

c. Trust or Estate |

||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

6. Transferor/Seller’s name (Enter only one name, unless husband and wife are iling a joint return. If more |

|

|

d. Business Trust |

|||||||||||

|

|

|

|||||||||||||

|

than one transferor/seller, use separate forms for each.) |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

e. Partnership |

|||||||||

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Street Address including City, State and Zip Code |

|

|

|

|

|

|

|

|

|

f. S Corporation |

||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

g. Limited Liability Company |

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

h. Limited Liability Partnership |

|||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

8. Computation of total payment and tax to be withheld (see instructions) |

|

|

|

|

|

|

|

|

|

|||||

|

a. Total sales price paid to transferor |

|

|

|

|

|

|

a |

|

|

|

● |

|||

|

b. Less selling expenses |

|

|

|

|

|

|

b |

|

|

|

● |

|||

|

c. Less debts secured by mortgages or other liens on the property |

|

c |

|

|

|

|

● |

|||||||

|

d. Net proceeds |

|

|

|

|

|

|

d |

|

|

|

● |

|||

|

e. Total payments (net proceeds paid to transferor) |

|

|

e |

|

|

|

● |

|||||||

|

f. Transferor/seller’s ownership percentage |

|

|

|

|

|

|

f |

% |

|

|

||||

|

g. Transferor/seller’s share of total payment (multiply line e by line f) |

|

|

g |

|

|

|

● |

|||||||

|

h. Enter applicable rate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1) 2.5% of total payments, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2) 6.5% of estimated capital gain $__________________ |

|

|

h |

% |

|

|

||||||||

|

i. WV Income Tax withheld (multiply line g or amount of estimated capital gain by line h) |

|

|

|

|

|

|

|

|||||||

|

(If partial exemption granted, enter amount stated on Form WV/NRCE) |

|

|

i |

|

|

|

● |

|||||||

Under the penalties of perjury, I declare that I have examined this return and to the best of my knowledge and belief, it is true, correct and complete. If prepared by a person other than the transferor/seller, the declaration is based on all information to which the preparer has any knowledge.

Signature |

Date |

|

Make check or Money order payable to and Mail to: |

|

|

West Virginia state tax departMent |

|

|

tax account adMinistration diVision |

|

|

po box 784 |

|

|

charleston, WV |

*b56040801a* |

|

copy a – File With the West Virginia state tax departMent |

||

|

WV/NRSR

InstructIons for return of Income tax wIthholdIng

for nonresIdent sale of real property

here are three copies of From WV/NRSR

GeNeRal INStRuctIoNS

Purpose of form:

his form is designed to assure the regular and timely collection of wV income tax due from nonresident sellers of real property located within the state. his form is used to determine the amount of income tax withholding due on the sale of property and provide for its collection at the time of the sale or transfer.

Who must file:

If the transferor/seller is a nonresident individual or nonresident entity, and is transferring an interest in real property located within the state of wV, unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must ile form wV/nrsr with the wV state tax department. If there are multiple transferors/sellers, a separate form must be completed for each nonresident individual or nonresident entity subject to the withholding requirements. he separate form requirement does not apply to a husband and wife iling a joint wV income tax return.

a “nonresident entity” is deined to mean an entity that: (1) is not formed under the laws of wV, and (2) is not qualiied by or registered with the wV state tax department to do business in wV.

When to file:

unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must complete form wV/nrsr for each nonresident transferor/seller at closing of sale.

a nonresident individual or nonresident entity that sells real or personal property located in wV must ile a wV income tax return. he appropriate income tax return must be iled for the year in which the transfer of the real property occurred. he due date for each income tax return type can be found in the instructions to the speciic income tax return.

What to file:

copy a of form wV/nrsr must be submitted to the wV state tax department with check or money order in the aggregate amount of tax due for each nonresident transferor/seller with regard to a sale or transfer of real property within thirty (30) days of the date the amounts were withheld.

copy B of form wV/nrsr is to be provided to the transferor/seller at closing. nonresident individuals or nonresident entities must ile the appropriate wV income tax return for the year in which the transfer of the property occurred. see the speciic instructions for the tax return being iled.

copy c of form wV/nrsr is to be retained by the taxpayer.

SpecIfIc INStRuctIoNS foR completING the foRm:

lIne 1 enter the street address for the property as listed with the county assessor. If the property does not have a street address, provide such descriptive information as is used by the county assessor to identify the property. also include the property account Id number for the parcel being transferred. If the property is made up of more than one parcel and has more than one account number, include all applicable account numbers.

lINe 2 enter the date of transfer. he date of transfer is the efective date of the deed. he efective date is the later of: (1) the date of the last acknowledgement; or (2) the date stated in the deed.

lINe 3 check the box if the transferor/seller is reporting the gain under the installment method.

lINeS 4, 5, and 6 unless transferors/sellers are husband and wife and iling a joint wV income tax return, a separate form wV/ nrsr must be completed for each transferor/seller that is entitiled to receive any part of the proceeds of the transfer. enter the tax identiication number or social security number for the nonresident transferor/seller and the social security number for the spouse, if applicable. do not enter the street address of the property being transferred.

lINe 7 check the appropriate box for the transferor/seller.

lINe 8 If a certiicate of partial exemption is issued by the wV state tax commissioner, do not complete lines 8a through 8h. Instead, enter the amount stated on form wV/nrce.

complete this section to determine the total payment allocable to the transferor/seller that is subject to the income tax withholding requirements and the amount of tax required to be withheld. he total payment is computed by deducting from the total sales price including the fair market value of any property or other non- monetary consideration paid to or otherwise transferred to the transferor/seller the amount of any mortgages or other liens, the commission payable on account of the sale, and any other expenses due from the seller in connection with the sale.

lINe 8f If there are multiple owners, enter the percentage of ownership of the transferor/seller for whom this form is being iled.

lINe 8g multiply line 8e by line 8f to determine the transferor/ seller’s share of the total payment.

lINe 8h enter the applicable rate for the transferor/seller used for computing the withholding tax. If withholding tax is computed on 6.5%, enter the amount of the estimated capital gain on line h2.

lINe 8i enter the amount of tax withheld.

payment of tax: make check or money order payable to the wV state tax department.

signature: copy a of this return must be veriied and signed by the individual transferor/seller, an authorized person or oicer of a business entity, or the person responsible for closing.

SpecIfIc INStRuctIoNS foR tRaNSfeRoR/SelleR (copy B)

How to claim the tax withheld

a copy of form wV/nrsr (copy B) must be submitted with the appropriate wV Income tax return. failure to do so will result in

the disallowance of the credit claimed.

he manner in which the income tax withheld is claimed by the nonresident individual or nonresident entity depends on the type of wV income tax return you are required to ile. follow the speciic instructions below. claiming the income tax withheld on a line other than as described below may result in the withholding being denied.

Individuals and Revocable Living Trusts

nonresident individuals are required to ile a nonresident wV Income tax return (form

C corporations

c corporations are required to ile a wV combined corporation net Income/Business franchise tax return (form wV/cnf120).

he income tax withheld and reported on line 8 of form wV/nrsr must be claimed as a withholding income tax payment.

S corporations, Partnerships and Limited Liability Companies and Business Trusts

s corporation, partnerships and limited liability companies and business trusts that elect to be treated as

his tax, and any other tax paid with form wV/nrsr must be allocated to the nonresident shareholders, partners or members and reported on a modiied federal schedule

Trusts and Estates

trustees of trusts and personal representatives of estates are required to ile a wV fiduciary Income tax return (form

WV/NRSR |

RetuRN of iNcome tax WithholdiNg foR |

Rev. |

NoNReSideNt Sale of Real pRopeRty |

West Virginia

State Tax

Department

|

1. Property account ID Number: |

|

|

|

|

|

2. Date of transfer |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address and Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MM |

|

DD |

|

|

YYYY |

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Check if the transferor/seller is reporting gain |

||||||||||

|

|

|

|

|

|

|

|

under the installment method. |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

4. Transferor/Seller’s Identiication number |

|

CheCk one |

5. Spouse’s SSN Number |

|

|

|

7. Transferor/Seller is: |

|||||||||

|

|

|

|

SSn |

|

|

|

|

|

|

|

|

|

a. Individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

FeIn |

|

|

|

|

|

|

|

|

|

b. Corporation |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ITIn |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

c. Trust or Estate |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

6. Transferor/Seller’s name (Enter only one name, unless husband and wife are iling a joint return. If more |

|

|

d. Business Trust |

|||||||||||||

|

|

|

|||||||||||||||

|

than one transferor/seller, use separate forms for each.) |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

e. Partnership |

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Street Address including City, State and Zip Code |

|

|

|

|

|

|

|

|

|

|

|

f. S Corporation |

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

g. Limited Liability Company |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

h. Limited Liability Partnership |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

8. Computation of total payment and tax to be withheld (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

a. Total sales price paid to transferor |

|

|

|

|

|

|

|

a |

|

|

|

|

● |

|||

|

b. Less selling expenses |

|

|

|

|

|

|

|

b |

|

|

|

|

● |

|||

|

c. Less debts secured by mortgages or other liens on the property |

|

c |

|

|

|

|

|

|

● |

|||||||

|

d. Net proceeds |

|

|

|

|

|

|

|

d |

|

|

|

|

● |

|||

|

e. Total payments (net proceeds paid to transferor) |

|

|

|

e |

|

|

|

|

● |

|||||||

|

f. Transferor/seller’s ownership percentage |

|

|

|

|

|

|

|

f |

|

% |

|

|

||||

|

g. Transferor/seller’s share of total payment (multiply line e by line f) |

|

|

|

g |

|

|

|

|

● |

|||||||

|

h. Enter applicable rate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1) 2.5% of total payments, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2) 6.5% of estimated capital gain $__________________ |

|

|

|

h |

|

% |

|

|

||||||||

|

i. WV Income Tax withheld (multiply line g or amount of estimated capital gain by line h) |

|

|

|

|

|

|

|

|

|

|||||||

|

(If partial exemption granted, enter amount stated on Form WV/NRCE) |

|

|

|

i |

|

|

|

|

● |

|||||||

copy b – For transFeror/seller(records copy)

WV/NRSR |

RetuRN of iNcome tax WithholdiNg foR |

Rev. |

NoNReSideNt Sale of Real pRopeRty |

West Virginia

State Tax

Department

|

1. Property account ID Number: |

|

|

|

|

|

2. Date of transfer |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address and Description |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MM |

|

DD |

|

|

YYYY |

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Check if the transferor/seller is reporting gain |

||||||||||

|

|

|

|

|

|

|

|

under the installment method. |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

4. Transferor/Seller’s Identiication number |

|

CheCk one |

5. Spouse’s SSN Number |

|

|

|

7. Transferor/Seller is: |

|||||||||

|

|

|

|

SSn |

|

|

|

|

|

|

|

|

|

a. Individual |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

FeIn |

|

|

|

|

|

|

|

|

|

b. Corporation |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ITIn |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

c. Trust or Estate |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

6. Transferor/Seller’s name (Enter only one name, unless husband and wife are iling a joint return. If more |

|

|

d. Business Trust |

|||||||||||||

|

|

|

|||||||||||||||

|

than one transferor/seller, use separate forms for each.) |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

e. Partnership |

|||||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Street Address including City, State and Zip Code |

|

|

|

|

|

|

|

|

|

|

|

f. S Corporation |

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

g. Limited Liability Company |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

h. Limited Liability Partnership |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

8. Computation of total payment and tax to be withheld (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

a. Total sales price paid to transferor |

|

|

|

|

|

|

|

a |

|

|

|

|

● |

|||

|

b. Less selling expenses |

|

|

|

|

|

|

|

b |

|

|

|

|

● |

|||

|

c. Less debts secured by mortgages or other liens on the property |

|

c |

|

|

|

|

|

|

● |

|||||||

|

d. Net proceeds |

|

|

|

|

|

|

|

d |

|

|

|

|

● |

|||

|

e. Total payments (net proceeds paid to transferor) |

|

|

|

e |

|

|

|

|

● |

|||||||

|

f. Transferor/seller’s ownership percentage |

|

|

|

|

|

|

|

f |

|

% |

|

|

||||

|

g. Transferor/seller’s share of total payment (multiply line e by line f) |

|

|

|

g |

|

|

|

|

● |

|||||||

|

h. Enter applicable rate: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1) 2.5% of total payments, or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2) 6.5% of estimated capital gain $__________________ |

|

|

|

h |

|

% |

|

|

||||||||

|

i. WV Income Tax withheld (multiply line g or amount of estimated capital gain by line h) |

|

|

|

|

|

|

|

|

|

|||||||

|

(If partial exemption granted, enter amount stated on Form WV/NRCE) |

|

|

|

i |

|

|

|

|

● |

|||||||

copy c – For issuer

Form Specifications

| # | Fact |

|---|---|

| 1 | The WV/NRSR form is officially titled "Return of Income Tax Withholding for Nonresident Sale of Real Property". |

| 2 | It is specifically designed for the collection of West Virginia state income tax from nonresident individuals or entities selling real property located within West Virginia. |

| 3 | The form is applicable when the transferor/seller of the real property is a nonresident of West Virginia. |

| 4 | Submission of this form is required at the closing of the sale or transfer of the property. |

| 5 | Instructions on the form include calculations for the total sales price, less selling expenses, debts, and the net proceeds to determine the taxable amount. |

| 6 | The form is governed by the West Virginia State Tax Department and must be filed in accordance with West Virginia law. |

| 7 | If the property sale is eligible for the installment sale method, the form offers a section to indicate this selection. |

| 8 | A detailed breakdown of the seller's share of the payment and the applicable tax rate to calculate the withholding tax is required. |

| 9 | The form requires the signature of the transferor/seller, certifying under penalty of perjury that the information provided is true and correct. |

| 10 | Payment of the tax amount withheld must be submitted to the West Virginia State Tax Department, along with Copy A of the form, within 30 days of the withholding. |

Guide to Filling Out Wv Nrsr

Once you've completed the sale of real property in West Virginia as a nonresident, you'll need to address the income tax withholding requirements using the WV/NRSR form. This form plays a crucial role in ensuring the state's tax obligations are met promptly and accurately. Below are detailed steps to guide you through filling out this form accurately, ensuring compliance with the requirements and facilitating a smooth submission process.

- Start by entering the Property account ID Number for the parcel being transferred. If the sale involves multiple parcels with distinct numbers, list all applicable account numbers.

- Fill in the Date of transfer, using the MM DD YYYY format. This date should match the effective date highlighted in the property's deed.

- Check the box if you are reporting the gain under the installment method.

- For Transferor/Seller’s Identification number, select the appropriate identifier (SSN, FEIN, ITIN) and provide the corresponding number.

- If applicable, enter the Spouse’s SSN Number.

- Under Transferor/Seller’s name, enter the name of the individual or entity transferring the property. If a joint return involves a married couple, both names can be included; otherwise, use separate forms for each transferor/seller.

- Select the correct identifier for the transferor/seller from the options (a. Individual, b. Corporation, etc.).

- For the Computation of total payment and tax to be withheld section:

- Enter the Total sales price paid to the transferor.

- Subtract any selling expenses, debts secured by the property, and note the Net proceeds.

- Detail the Total payments (net proceeds paid to the transferor).

- Record the Transferor/seller’s ownership percentage.

- Calculate the Transferor/seller’s share of total payment by multiplying the total payments by the ownership percentage.

- Enter the applicable rate for income tax withholding. This might be 2.5% of total payments or 6.5% of the estimated capital gain, depending on the specifics of the sale.

- Compute the WV Income Tax withheld by multiplying the share of total payment by the applicable rate, and enter this amount.

- In the signature area, the form must be signed by the transferor/seller, an authorized representative, or the closing agent, attesting to the accuracy of the return under penalty of perjury.

- Prepare a check or money order for the total tax amount owed, payable to the West Virginia State Tax Department. Mail this, along with copy A of the form, to: Tax Account Administration Division, PO Box 784, Charleston, WV 25323-0784.

Remember to provide the transferor/seller with copy B of the form and retain copy C for your records. Following these steps meticulously will ensure you meet the legal requirements for the withholding and reporting of income tax on the sale of real property by a nonresident in West Virginia.

Things You Should Know About Wv Nrsr

What is the WV/NRSR form and why is it important?

The WV/NRSR form is a return for income tax withholding for nonresident sales of real property in West Virginia. It's important because it ensures the collection of income tax due from nonresidents who sell real estate within the state. The form helps in determining the amount of tax to be withheld at the time of sale or transfer.

Who needs to file the WV/NRSR form?

Nonresident individuals or entities selling real property located in West Virginia must file the form, barring some exemptions. This requirement also applies if there are multiple nonresident sellers; each must file a separate form unless filing as a married couple on a joint return.

When should the WV/NRSR form be filed?

The form must be completed at the close of sale or transfer of the property by the person responsible for closing. The submitted form along with the payment of withheld taxes should reach the West Virginia State Tax Department within 30 days of the withholding.

What should be included when filing the WV/NRSR form?

One must submit Copy A of the WV/NRSR form to the West Virginia State Tax Department, accompanied by a check or money order for the total amount of tax due for each nonresident seller. Additionally, nonresident sellers must file a West Virginia income tax return for the year in which the transfer occurred.

How does a nonresident claim the tax withheld?

Nonresidents should include Copy B of the WV/NRSR form with their state income tax return. Failing to attach this form may result in the disallowance of the claimed withholding credit. The specific line to claim this withholding varies depending on the type of income tax return filed.

What are the specific steps for completing the WV/NRSR form?

To complete the form, one must provide the property and transferor details, calculate the net proceeds from the sale, determine the transferor/seller's share of the total payment, and compute the tax to be withheld. If eligible, one may apply for a partial exemption rather than calculating the tax based on the standard rates.

What happens if there are multiple owners of the sold property?

When multiple owners are involved, each nonresident owner must file a separate WV/NRSR form unless they are married and filing jointly. The ownership percentage of the transferor/seller being filed for must be indicated on the form to calculate the correct amount of tax to be withheld.

How does one pay the tax required to be withheld?

The tax due should be paid by check or money order made out to the West Virginia State Tax Department. This payment, along with Copy A of the form, must be mailed to the tax department's specified address within 30 days of the tax being withheld.

Common mistakes

Completing the West Virginia Nonresident Seller Real Property Withholding (WV/NRSR) form can be a daunting task for many, leading to common mistakes that could delay transactions or lead to incorrect withholdings. Here are eight typical errors to avoid:

Incorrect Property Identification: Failing to correctly enter the property account ID number or not providing a clear description of the property. This identification is crucial for the West Virginia State Tax Department to locate and assess the correct property involved in the transaction.

Transfer Date Errors: The date of transfer must accurately reflect the effective date of the deed. This is either the date of the last acknowledgement or the date stated within the deed itself. Incorrect dates can cause processing delays.

Installment Sale Reporting: Neglecting to indicate whether the sale will be reported under the installment method. This selection impacts the calculation of the withholding tax due.

Entering multiple names in the section intended for the transferor/seller's name without considering the filing status. If a joint return is not being filed, separate forms must be used for each seller.

Overlooking Ownership Percentage: Mistakes in listing the seller's ownership percentage can lead to incorrect computation of the withholdable tax. This figure plays a significant role in determining the seller’s share of total payment.

Incorrect calculation in the computation of total payment and tax to be withheld. Each step from the total sales price to the final withholding tax requires careful attention to detail.

Withholding Tax Rate Selection: Incorrectly choosing the applicable tax rate for withholding can result in underpayment or overpayment of taxes. Ensure to accurately apply the 2.5% or 6.5% rate as dictated by the estimated capital gain or total payment.

Failure to sign or date the form. A signature and date confirm that the information provided is accurate to the best of the filer’s knowledge and ensures the form is processed efficiently.

Avoiding these common mistakes can smooth the process of real property transactions involving nonresidents in West Virginia. It’s always a good idea to thoroughly review the form and its instructions, or consult with a professional, to ensure compliance and accurate withholding.

Documents used along the form

When dealing with the intricacies of nonresident sales of real property in West Virginia, a thorough understanding of the documentation required is invaluable. The West Virginia Nonresident Seller's Income Tax Withholding (WV/NRSR) form is just the starting point for a series of documents that play critical roles in ensuring compliance with state tax laws. These documents range from declarations of exemption to tax returns, each serving a unique purpose in the transaction process. The understanding and correct application of these documents ensure that both the transferor/seller and the transferee/purchaser meet their legal obligations, thereby facilitating a smooth and legally compliant property transfer.

- WV/NRCE Certificate of Exemption: This form is crucial when a real estate transaction qualifies for exempt status, negating the need for income tax withholding for a nonresident seller.

- WV State Income Tax Return: For nonresidents who have conducted transactions, filing a state income tax return is mandatory to report any gains or losses from the sale of real property in West Virginia.

- IRS Form 8288: For transactions involving foreign sellers, this IRS form collects the withholding tax on the sale or transfer of U.S. real property interests by foreign persons.

- IRS Form W-9: The Request for Taxpayer Identification Number and Certification is used to obtain the correct taxpayer identification number of the seller to report income tax withholding correctly.

- Closing Disclosure: This document itemizes all the financial details of the transaction, including the sales price, loan amounts, closing costs, and the total amount due to/from the buyer and seller.

- Title Deed: The official document transferring ownership from the seller to the buyer. It must be filed with the state to record the new ownership.

- Property Tax Records: These records, obtained from local authorities, provide historical tax information on the property and verify that all property taxes have been paid up to the point of sale.

- Settlement Statement (HUD-1): Used in some transactions, this form provides a detailed breakdown of all costs associated with the transaction. It’s essential for record-keeping and tax purposes.

- Nonresident Withholding Tax Receipt: After paying the required withholding tax, a receipt or confirmation from the West Virginia State Tax Department serves as proof of payment.

In essence, each document associated with the WV/NRSR form plays a pivotal role in orchestrating a lawful and transparent transaction involving nonresident sellers of real estate in West Virginia. Professionals involved in such transactions must ensure that these documents are correctly completed and filed to adhere to state tax obligations and property law. The compilation and accurate processing of these documents ensure the lawful completion of real estate transactions, thereby protecting the interests of all parties involved.

Similar forms

The Federal FIRPTA Withholding Form (IRS Form 8288 or 8288-A) is similar to the WV/NRSR form in its core purpose, which is the collection of tax on the sale of U.S. real property interests by foreign persons. Both forms require the buyer or other appointed party to withhold a certain percentage of the sale proceeds to ensure the collection of taxes. While the FIRPTA forms apply to foreign sellers on a national level, the WV/NRSR specifically addresses nonresident sales within West Virginia.

State Nonresident Income Tax Withholding Forms found in other states parallel the WV/NRSR form, focusing on real estate transactions involving nonresident sellers. Each state's form mandates the withholding of state income tax on sales or transfers of real property and associated tangible personal property. Though the specifics, such as rate and exemption qualifications, may vary, the overarching goal is to secure payment of taxes from nonresidents to prevent tax evasion.

The 1099-S Form, used in the reporting of sale or exchange of real estate, shares a commonality with the WV/NRSR form in that it involves real estate transactions. However, the 1099-S emphasizes reporting the transaction to the IRS for federal tax purposes, including sales by residents and nonresidents, whereas the WV/NRSR focuses on withholding state tax from nonresidents at the time of sale.

The Seller's Residency Certification/Exemption (SRCE) forms, utilized in various states, resemble the WV/NRSR form through their function of certifying a seller's residency status for tax purposes during a real estate transaction. These forms determine whether a seller qualifies for exemption from state withholding requirements based on their residency status, similar to how the WV/NRSR form identifies nonresident sellers liable for state income tax withholding.

The Closing Disclosure form, part of the real estate settlement procedures in residential property sales, shares an indirect linkage with the WV/NRSR by detailing the financial transactions involved in a property sale. Although its primary purpose is to provide transparency in the transaction between buyer and seller, it also supports tax form accuracy by listing the sales price and other financial details necessary for completing forms like the WV/NRSR.

State Capital Gains Tax Forms that require the calculation and reporting of capital gains from the sale of real property also share a purpose with the WV/NRSR form. These forms may vary by state but generally involve calculating net proceeds from the sale to determine the taxable amount. The WV/NRSR form requires similar computations to ascertain the correct withholding tax based on the seller's gains.

Lastly, the Real Estate Withholding Certificate forms, specific to some states, necessitate action similar to the WV/NRSR form by requesting details about a property transaction to enforce withholding tax on nonresident sellers. They serve the comparable objective of capturing tax at the point of sale, ensuring that nonresident sellers meet their tax obligations for property sales within the state.

Dos and Don'ts

When dealing with the West Virginia Nonresident Sale of Real Property Tax Withholding (WV/NRSR) form, accurately completing and submitting the form is paramount. This document facilitates the collection of income tax from nonresident sellers of real property in West Virginia. To assist in this process, here are some crucial do's and don'ts:

Do:- Verify the property account ID number and address. It’s essential to ensure the property identification and location details align with county records for accurate processing.

- Accurately report the date of transfer. The date of transfer should reflect the effective date noted in the deed documentation.

- Complete separate forms for each transferor/seller, if applicable. Unless filing jointly as husband and wife, separate forms are required for each individual involved in the transfer.

- Correctly compute the total payment and tax to be withheld. Deduct relevant expenses and calculate the correct amount of withholding tax based on the net proceeds and applicable rate.

- Sign and date the form under the penalty of perjury. A signature is necessary to attest to the accuracy of the information provided on the form.

- Make payment to the appropriate authority. Check or money orders should be made payable to the West Virginia State Tax Department and submitted as instructed.

- Overlook checking if the installment method applies. If the seller is reporting gain under the installment method, this should be indicated on the form.

- Misstate the ownership percentage. For properties with multiple owners, it’s crucial to accurately report each owner's share of the total payment.

- Ignore instructions for partial exemptions. If a certificate of partial exemption has been issued, follow the modified instructions for withholding computation.

- Enter incorrect identification numbers. Ensure the transferor/seller’s identification number and, if applicable, the spouse’s SSN are accurately reported.

- Forget to provide all necessary copies. Copy A must be submitted to the WV State Tax Department, Copy B should go to the transferor/seller, and Copy C is retained by the issuer.

- Delay submission beyond the deadline. To avoid penalties, submit Copy A with the appropriate payment within 30 days of the withholding date.

Adhering to these guidelines will help ensure a smooth process in complying with West Virginia's requirements for the taxable event of a nonresident's sale of real property.

Misconceptions

When it comes to the WV/NRSR, a form required for the return of income tax withholding for nonresident sales of real property in West Virginia, there are several misconceptions that can lead to confusion and potentially incorrect filings. Here, we aim to clarify these misconceptions to ensure accurate and compliant submissions.

Misconception 1: The form is only for individuals. While the form is often associated with individual sellers, it is also designed for a variety of transferor/seller types including corporations, trusts, estates, business trusts, partnerships, S corporations, limited liability companies, and limited liability partnerships.

Misconception 2: Only one form is needed per sale, regardless of the number of sellers. In fact, if there are multiple transferor/sellers (except for a husband and wife filing jointly), separate forms must be completed for each.

Misconception 3: The form is complex and requires extensive financial information. The form primarily requires basic information about the sale, the seller, and computation of total payment and tax to be withheld, guided by comprehensive instructions provided.

Misconception 4: It’s only applicable if a financial gain is made from the sale. The obligation to file this form and withhold tax arises from the sale or transfer of real property by nonresidents, not from the profit or loss realized from the sale.

Misconception 5: No tax withholding is required if the seller reports a loss on the sale. The requirement to withhold tax is based on the transfer of property, regardless of whether the sale results in a gain or a loss.

Misconception 6: The full sales price is subject to withholding. The form allows for deductions such as selling expenses and debts secured by mortgages or other liens on the property to calculate the net proceeds and the total payment subject to withholding.

Misconception 7: The transferor/seller’s signature is not necessary. The form must be verified and signed by the individual transferor/seller, an authorized person or officer of a business entity, or the person responsible for closing, affirming the accuracy of the information provided.

Misconception 8: The transferor/seller does not need to report the sale on their West Virginia income tax return if the WV/NRSR form is filed. Nonresident individuals or entities must also file the appropriate WV income tax return for the year in which the transfer occurred.

Misconception 9: The installment sale method cannot be applied to nonresident sales of real property in West Virginia. The form specifically provides an option to check if the gain is being reported under the installment method.

Misconception 10: Estimated payments cannot adjust the amount withheld. In cases where a certificate of partial exemption is issued by the WV State Tax Commissioner, only the amount stated on the Form WV/NRCE needs to be withheld, which might be lesser than the standard calculation.

Addressing these misconceptions helps ensure that individuals and entities involved in nonresident property sales in West Virginia understand their obligations and are able to accurately complete and file the WV/NRSR form, thereby complying with state tax requirements.

Key takeaways

Filling out the West Virginia Nonresident Seller (WV/NRSR) Income Tax Withholding form is a crucial step for nonresident sellers when selling real property located in West Virginia. Here are some key takeaways to remember:

- Nonresident individuals or entities must fill out this form if they are selling real estate in West Virginia, unless the sale is exempt from income tax withholding. The purpose is to ensure the collection of any applicable income tax from the sale.

- The form requires detailed information about the sale, including property identification, date of transfer, seller identification, and computation of the tax to be withheld. Accuracy in filling out these details is essential for compliance with state tax requirements.

- Separate forms must be used for each transferor or seller unless a husband and wife are filing a joint return. This means that if multiple owners are involved in the sale, each nonresident owner must complete their own form.

- Calculating the total payment and tax to be withheld involves several steps, including determining the net proceeds from the sale and the seller's share of the total payment. These calculations guide the amount of income tax that must be withheld from the sale proceeds.

- After completion, Copy A of the form must be sent to the West Virginia State Tax Department along with the appropriate payment, while Copy B should be provided to the transferor/seller for their records. Copy C is for the issuer's records. Timely submission within 30 days of the sale is important to avoid penalties.

Being diligent in completing and submitting the WV/NRSR form is essential for both compliance purposes and to facilitate the proper allocation and reporting of income from the sale of real property by nonresidents in West Virginia.

Popular PDF Forms

Wv Sales and Use Tax Form - The inclusion of a space for the purchaser’s signature and title formalizes the declaration and asserts the claims made in the document.

Wv Pas - Provides a coherent framework for evaluating care needs against available services.