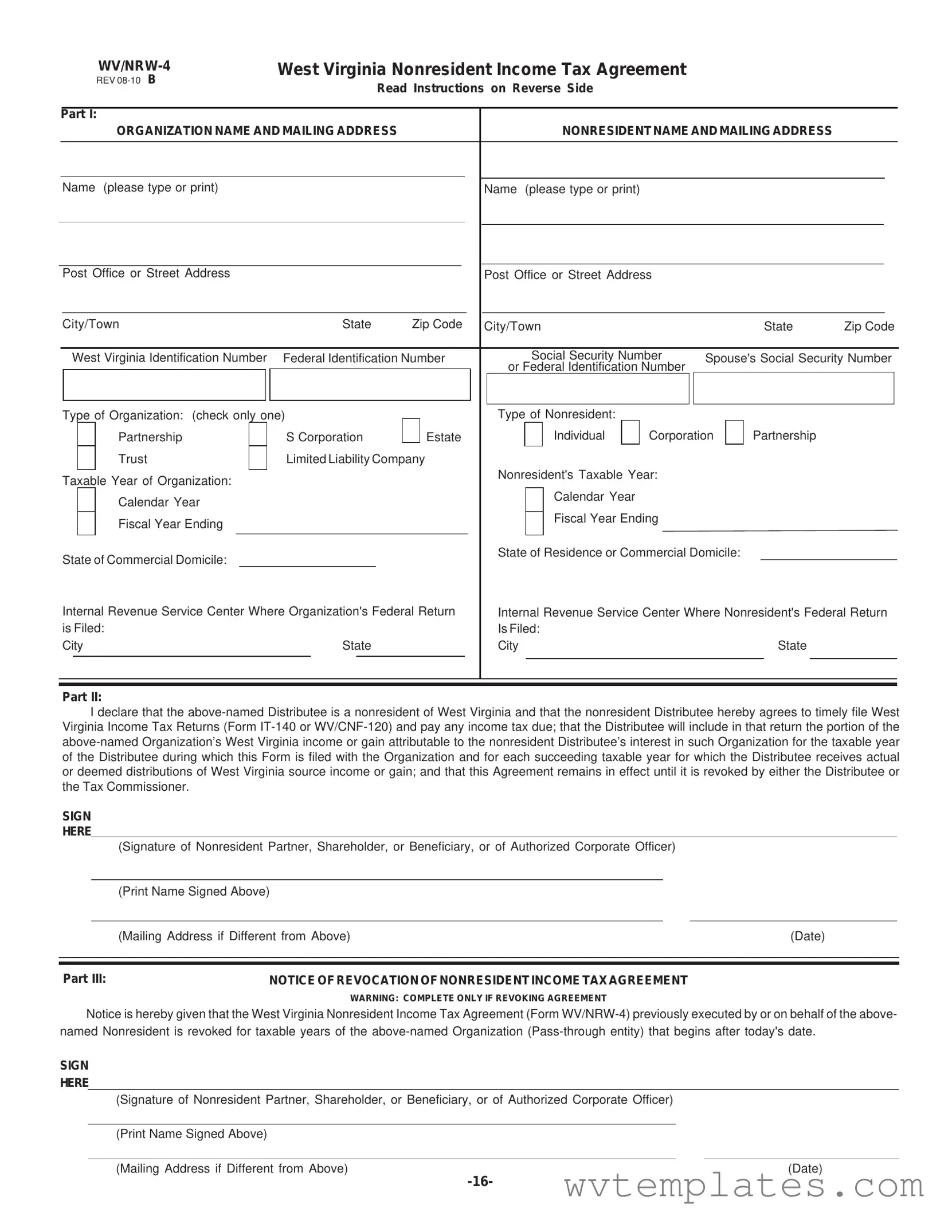

Free Wv Nrw 4 Form

In addressing the complexities associated with nonresident income tax obligations, the West Virginia Nonresident Income Tax Agreement, known as Form WV/NRW-4, serves a key role for both nonresidents and organizations operating within the state. This document, meticulously designed to streamline the process of tax compliance for nonresident individuals and entities earning income from West Virginia sources through partnerships, S corporations, estates, trusts, or limited liability companies, operates under the provisions outlined in West Virginia Code § 11-21-71a. The importance of this form lies in its capacity to exempt specified nonresidents from the withholding tax that might otherwise be deducted by the distributing organization. A critical aspect of this agreement is its requirement for nonresident distributees to declare their commitment to timely file West Virginia Income Tax Returns and to include in their returns the portion of income or gain attributable to their West Virginia activities. Moreover, the form stipulates that the nonresident distributee agrees to maintain this compliance for each taxable year in which they receive real or deemed distributions of income from the source within West Virginia. The execution of this agreement involves a detailed process outlined in the form, including the requirement for the agreement to be filed with the respective organization before the last day of the organization's taxable year to avoid state income tax withholding. Additionally, the agreement remains in effect until expressly revoked by the distributee or by the Tax Commissioner, with specific routes provided for revocation by either party. Through the lens of these guidelines, Form WV/NRW-4 exemplifies a carefully structured agreement aimed at ensuring tax compliance while minimizing the administrative burden on nonresident income earners and their associated organizations within West Virginia.

Wv Nrw 4 Example

|

|

West Virginia Nonresident Income Tax Agreement |

||||||

|

|

REV |

Read Instructions on Reverse Side |

|||||

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

Part I: |

|

|

|

|

|

|

|

|

|

ORGANIZATION NAME AND MAILING ADDRESS |

NONRESIDENT NAME AND MAILING ADDRESS |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (please type or print) |

|

|

|

Name |

(please type or print) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Post Office or Street Address |

|

|

|

|

|

|

|

|

|

|

|

Post Office or Street Address |

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City/Town |

|

|

State |

Zip Code |

City/Town |

|

|

|

|

|

|

State |

Zip Code |

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

West Virginia Identification Number |

|

Federal Identification Number |

|

|

Social Security Number |

Spouse's Social Security Number |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or Federal Identification Number |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type of Organization: (check only one) |

|

|

|

|

|

|

|

Type of Nonresident: |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

Partnership |

|

|

S Corporation |

|

Estate |

|

|

|

Individual |

|

Corporation |

|

Partnership |

|

|

|

|

||||||||||||||

|

|

|

|

Trust |

|

|

Limited Liability Company |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonresident's Taxable Year: |

|

|

|

|

|

|

|

|

|

|

|||||

Taxable Year of Organization: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

Calendar Year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar Year |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

Fiscal Year Ending |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fiscal Year Ending |

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

State of Commercial Domicile: |

|

|

|

|

|

|

|

|

|

|

|

|

|

State of Residence or Commercial Domicile: |

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Internal Revenue Service Center Where Organization's Federal Return |

|

Internal Revenue Service Center Where Nonresident's Federal Return |

|||||||||||||||||||||||||||||||||

is Filed: |

|

|

|

|

|

|

|

|

|

|

|

|

Is Filed: |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

City |

|

|

State |

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

State |

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part II:

I declare that the

SIGN

HERE

|

|

(Signature of Nonresident Partner, Shareholder, or Beneficiary, or of Authorized Corporate Officer) |

|

|

|

|

|

|

|

|

|

|

|

(Print Name Signed Above) |

|

|

|

|

|

|

|

|

|

|

|

(Mailing Address if Different from Above) |

(Date) |

|

|

|

|

|

|

||

|

|

|

|

||

Part III: |

NOTICE OF REVOCATION OF NONRESIDENT INCOME TAX AGREEMENT |

|

|

||

WARNING: COMPLETE ONLY IF REVOKING AGREEMENT

Notice is hereby given that the West Virginia Nonresident Income Tax Agreement (Form

SIGN

HERE

(Signature of Nonresident Partner, Shareholder, or Beneficiary, or of Authorized Corporate Officer)

(Print Name Signed Above)

(Mailing Address if Different from Above) |

(Date) |

WEST VIRGINIA NONRESIDENT INCOME TAX AGREEMENT

INSTRUCTIONS

Who May File: Any Nonresident individual or C corporation who has West Virginia source income derived from a partnership, S corporation, estate, trust, or limited liability company (“Organization”) who desires to not have West Virginia income tax withheld by that Organization as provided in W.Va. Code §

When and Where to File: This Form must be completed and filed with the Organization on or before the last day of the Organization’s taxable year. If the Distributee receives West Virginia source income from more than one such Organization, a separate Form WV/NRW- 4 must be filed with each Organization in order to avoid withholding by that Organization. The Organization may copy this form or use a facsimile to distribute as follows: (1) one copy to be filed with the Organization's West Virginia income tax return, (2) one copy to be retained by the

West Virginia Income Tax Withholding for Nonresidents: Every Organization distributing West Virginia source income to a nonresident distributee is required to withhold West Virginia income tax on the amount thereof distributed to Nonresident Distributee unless the Nonresident Distributee timely files this Form with the Organization and the Organization attaches a copy of it to its West Virginia income tax return filed for the taxable year of its receipt. The withholding tax rate is 6.5% of distributions of West Virginia source income (whether actual or deemed distributions). The amount of tax withheld and remitted by the Organization is allowed as a credit against the Distributee’s West Virginia income tax liability for that taxable year.

Nonresident Agreement: Once this agreement is executed, it must be filed with the Organization to avoid having withholding tax deducted from further distributions (actual or deemed). This agreement first applies to the taxable year of the Organization during which the Organization receives a properly executed agreement from the Nonresident Distributee.

Duration of Agreement: Once this Agreement is filed with the Organization, it remains in effect until it is revoked by the Nonresident Distributee, or by the Tax Commissioner.

Revocation:

1.A Nonresident Distributee may revoke this Agreement by completing this Form and filing it with the Organization through which it receives West Virginia source income. Revocation applies prospectively, meaning that it first applies to taxable years of the Organization which begin after revocation is filed with that Organization.

2.The Tax Commissioner may revoke this Agreement if the Nonresident Distributee fails to file a West Virginia income tax return

Form Specifications

| Fact | Detail |

|---|---|

| Purpose | Allows nonresident individuals and C corporations to avoid West Virginia income tax withholding by agreeing to file West Virginia income tax returns and pay taxes on West Virginia source income. |

| Eligible Parties | Nonresident individuals or C corporations with West Virginia source income derived from partnerships, S corporations, estates, trusts, or limited liability companies. |

| When and Where to File | Must be filed with the Organization on or before the last day of the Organization’s taxable year. Separate forms are required for each Organization to avoid withholding. |

| Duration and Revocation | The agreement remains in effect until it is revoked by the nonresident distributee or the Tax Commissioner. Revocation applies prospectively to future taxable years. |

| Governing Law | West Virginia Code § 11-21-71a. Requires nonresident income tax agreements for certain nonresidents to prevent withholding tax deductions on distributions of West Virginia source income. |

Guide to Filling Out Wv Nrw 4

Before diving into the detailed process of completing the WV/NRW-4 form, it's vital to understand what awaits next. This essential form serves as the linchpin for nonresident individuals and corporations generating income through various organizations within West Virginia, aiming to sidestep the default withholding tax on their earnings. By accurately filling out this agreement, nonresidents assert their commitment to timely file West Virginia income tax returns and manage tax due, directly influencing how their earnings are treated tax-wise. The agreement, once filed, establishes a critical pact with the Organization, altering the withholding tax mechanism and ensuring compliance with West Virginia’s tax obligations.

To accurately complete the West Virginia Nonresident Income Tax Agreement (WV/NRW-4), please follow these step-by-step instructions:

- Part I: Start with your organization's name and mailing address. Include the full name (typed or printed), street or post office address, city or town, state, and zip code.

- Enter the West Virginia Identification Number alongside the Federal Identification Number for your organization. If you are filing as an individual, include your Social Security Number (and your spouse’s, if applicable).

- Select your type of organization from the options provided (Partnership, S Corporation, Estate, Individual, Corporation, Partnership, Trust, Limited Liability Company) by checking the appropriate box.

- Specify the taxable year of your organization. Indicate whether it follows a calendar year or a fiscal year ending on a specific date.

- For nonresidents, fill in your name and mailing address following the same format as for the organization’s details.

- Indicate your state of residence or commercial domicile, along with the Internal Revenue Service Center where your federal return is filed, including the city and state.

- Document the nonresident's taxable year in the same manner as done for the organization's taxable year.

Part II: This section requires the signature of the nonresident partner, shareholder, beneficiary, or an authorized corporate officer, asserting the commitments laid out in the form. Make sure to print the name signed, provide a mailing address if different from above, and date the agreement to seal this pact.

Part III: NOTICE OF REVOCATION OF NONRESIDENT INCOME TAX AGREEMENT: This segment is only to be completed if you're revoking a previously executed agreement. It mirrors the signature requirement of Part II with an emphasis on the revocation’s applicability moving forward.

Upon diligently following these steps, ensure to distribute copies of the completed form as directed. One copy shall accompany the organization's West Virginia income tax return, another retained by the pass-through entity, and a final copy for the nonresident distributee. By doing so, you facilitate a smooth execution of your tax obligations, directly shaping your tax liability and compliance with the state’s legislative requirements.

Things You Should Know About Wv Nrw 4

What is the purpose of the WV/NRW-4 form?

The WV/NRW-4 form allows nonresident individuals and C corporations that derive income from West Virginia sources through partnerships, S corporations, estates, trusts, or limited liability companies to agree not to have West Virginia income tax withheld by these organizations. This agreement is necessary to comply with West Virginia Code § 11-21-71a, and it ensures that nonresidents include their share of West Virginia income on their own tax returns.

Who needs to file the WV/NRW-4 form?

Any nonresident individual or C corporation with West Virginia source income from an organization such as a partnership, S corporation, estate, trust, or limited liability company needs to complete and file the WV/NRW-4 form. This requirement applies to entities whose commercial domicile is located outside of West Virginia.

When should the WV/NRW-4 form be filed?

The form must be filed on or before the last day of the organization's taxable year. If the nonresident receives income from more than one such organization in West Virginia, they need to file a separate WV/NRW-4 form with each organization to avoid income tax withholding.

Where should the WV/NRW-4 form be filed?

The completed form should be submitted directly to the organization distributing the West Virginia source income. The organization is responsible for attaching a copy of this form to its West Virginia income tax return.

What is the withholding tax rate for nonresidents?

Organizations distributing West Virginia source income to nonresident distributees are required to withhold West Virginia income tax at a rate of 6.5% of the distributed income, unless the distributee has timely filed a WV/NRW-4 form. This withheld amount can be credited against the distributee's West Virginia income tax liability for the taxable year.

How long does the nonresident agreement last?

Once filed, the nonresident agreement remains in effect until it is revoked by either the nonresident distributee or by the Tax Commissioner. This means that as long as the agreement is in place, withholding on distributions will not be required.

How can a nonresident revoke the agreement?

A nonresident can revoke the agreement by completing the WV/NRW-4 form indicating the revocation and filing it with the organization from which they receive West Virginia source income. The revocation will apply going forward, affecting only the taxable years of the organization that begin after the revocation is filed.

What happens if a nonresident fails to file or pay taxes?

The Tax Commissioner may revoke this agreement if the nonresident fails to file a West Virginia income tax return or to timely pay West Virginia income tax for any taxable year covered by the agreement. The revocation is considered if the failure exceeds more than 60 days after the due date of the return, including any extensions.

Can organizations use a facsimile of the WV/NRW-4 form?

Yes, organizations may use a facsimile of the WV/NRW-4 form to distribute to nonresident distributees. The organization must keep a copy of the form, attach a copy to its West Virginia income tax return, and provide a copy to the nonresident distributee.

Common mistakes

Filling out the WV/NRW-4 form, while straightforward to some, can often be a source of errors due to overlooked details or misunderstandings of what's required. Here are common mistakes made when completing this form:

- Not double-checking the organization or nonresident name and address fields: It's crucial to ensure that these fields are filled out accurately, including correct spelling and current addresses. A mix-up here can lead to correspondence and tax documents being sent to the wrong place.

- Incorrect or missing identification numbers: Every organization and individual must provide their West Virginia Identification Number, Federal Identification Number, or Social Security Number where applicable. Leaving these blank or entering them incorrectly can cause significant processing delays.

- Failing to check the correct type of organization or nonresident: This section is essential for the correct processing of the form. One common mistake is overlooking this part entirely or making an incorrect selection that doesn’t match the organization's or individual's status.

- Choosing the wrong taxable year format: Organizations and nonresidents need to specify whether they are reporting based on a calendar year or a fiscal year. Mixing these up can create discrepancies in your tax obligations and filings.

- Not specifying the state of commercial domicile accurately: Particularly for corporations, indicating the state where the principal business is conducted is crucial. An incorrect state can lead to inappropriate tax assessments or benefits.

- Sending the form to the wrong place or at the wrong time: The instructions specify when and where to file this form. Missing the deadline or sending it to the wrong location can result in unwanted withholding or penalties.

- Signing but not printing name or providing a different mailing address if applicable: The signature area asks for a printed name and possibly a different mailing address. This is often overlooked, which can be problematic if a clear audit trail is necessary or if correspondence needs to be sent to another address.

- Revocation errors: If revoking the agreement, it is essential to fill out the notice of revocation correctly and understand that it applies prospectively. Not clearly understanding the implications of revocation can lead to unexpected tax liabilities.

Avoiding these mistakes requires careful attention to the form's instructions and details. Double-checking entries for accuracy and completeness can save a great deal of time and prevent issues with tax filings. Additionally, when in doubt, seeking clarification from a tax professional or the tax authority can help ensure that the form is filled out correctly.

Remember, even seemingly minor errors on forms like the WV/NRW-4 can have significant implications for tax liability and compliance. Investing the time to fill it out accurately and completely is well worth the effort.

Documents used along the form

When dealing with the WV/NRW-4 form, which is a West Virginia Nonresident Income Tax Agreement, individuals and organizations often need to submit additional forms and documents to ensure compliance with tax laws and regulations. These documents play crucial roles in the tax filing process, helping both nonresidents and the tax authorities to accurately determine tax liabilities and entitlements. The following list outlines some of the key forms and documents commonly used alongside the WV/NRW-4 form:

- IT-140 Form: The West Virginia Personal Income Tax Return for residents and nonresidents. This form is crucial for individuals, as it is used to report income earned within West Virginia and to calculate the state income tax due.

- WV/CNF-120 Form: The West Virginia Corporate Net Income Tax Return. Corporations use this form to report their income, gains, losses, and to calculate their corporate income tax liability to the state.

- WV/SPF-100 Form: The Special Nonresident Income Tax Return for certain nonresident individuals, estates, and trusts deriving income from West Virginia sources. This form is particularly relevant for entities that have specific types of West Virginia source income.

- WV/UCR-1 Form: The Employer's Quarterly Contribution Report. Employers in West Virginia use this form to report wages paid to employees and to calculate unemployment insurance contributions.

- WV/IT-101V: Electronic Filing Payment Voucher. This is used by filers who submit their state tax returns electronically, allowing them to also make payments electronically.

- W-9 Form: Request for Taxpayer Identification Number and Certification. This form is often required from individuals or entities that receive income, to ensure accurate tax reporting and withholding.

- Extension Request Forms: These forms, specific to different types of filers (individual, corporate, etc.), allow taxpayers to request additional time to file their state tax returns if they cannot meet the original deadline.

Together, these forms and documents support a comprehensive approach to tax filing for individuals and entities with obligations in West Virginia, ensuring that all necessary information is accurately reported and processed. By efficiently managing these forms, taxpayers can better navigate their tax responsibilities, potentially avoiding common pitfalls such as underpayment or late filing penalties.

Similar forms

The WV/NRW-4 West Virginia Nonresident Income Tax Agreement has several counterparts in other states and legal frameworks, each designed to manage tax obligations for nonresidents earning income within the jurisdiction. One similar document is the California Form 588, Nonresident Withholding Waiver Request. Like the WV/NRW-4, this form enables nonresidents to request a waiver from withholding on income earned in California, specifying conditions under which nonresident income is subject to state tax and the process for requesting an exemption.

Another comparable document is the New York IT-2104-E, Certificate of Exemption from Withholding. It serves a similar purpose by allowing nonresident employees or those who expect to earn income in the state to declare an exemption from New York State income tax withholding. The form is critical for nonresidents who earn income in New York but wish to assert their nonresident tax status, paralleling the WV/NRW-4’s function for West Virginia income.

The Texas Nonresident Employee Waiver, though Texas does not have a state income tax, resembles the WV/NRW-4 in its purpose to clarify tax responsibilities for nonresidents. For states like Texas with unique tax laws, similar forms may address other tax-related disclosures for nonresident workers or investors, ensuring compliance with state-specific legal requirements while acknowledging the individual's nonresident status.

Arizona’s Form 301, Nonresident Personal Income Tax Agreement, is a close counterpart, allowing nonresident individuals to report income earned within the state and arrange for appropriate tax treatment. This form, like the WV/NRW-4, lays out the responsibilities of nonresident earners regarding filing and paying state income taxes, emphasizing the interstate nature of modern work and investment.

Florida’s Declaration of Domicile, while not a tax form per se since Florida does not levy a personal income tax, is a legal document that nonresidents might file to clarify their residency status. This document can be seen as a counterpart to the WV/NRW-4 in contexts where establishing nonresidency or domicile is crucial for legal or tax purposes, albeit serving a broader purpose beyond income tax alone.

Illinois Form NR, Agreement Between Resident and Nonresident Taxpayers, facilitates a similar agreement between nonresident individuals earning income in Illinois and the state’s Department of Revenue. It outlines how nonresidents can comply with state tax obligations, mirroring the WV/NRW-4’s aim to ensure tax compliance for nonresident income earners in West Virginia.

Lastly, the Pennsylvania REV-1832, Nonresident Withholding Agreement Form, shares the WV/NRW-4's goal in managing tax obligations for nonresidents. It is used for income earned by nonresidents within Pennsylvania, detailing the state's process for withholding and reporting income tax in a manner that acknowledges the complexities of interstate and nonresident income.

Each of these documents, while tailored to the specific tax laws and requirements of their respective states, shares the WV/NRW-4's fundamental objective: to facilitate clear, compliant tax processes for nonresident income earners. They reflect a common challenge across jurisdictions—balancing the ease of doing business or working across state lines with the need to ensure fair and adequate tax collection.

Dos and Don'ts

Filling out the WV/NRW-4 form, a West Virginia Nonresident Income Tax Agreement, is a crucial task that demands attention to detail. This form is designed for nonresident individuals or C corporations with West Virginia source income from partnerships, S corporations, estates, trusts, or limited liability companies. To ensure accurate and efficient completion of this form, here are several dos and don'ts to keep in mind:

- Do read the instructions on the reverse side of the form thoroughly before beginning to fill it out. Understanding these guidelines can prevent common mistakes.

- Do type or clearly print all requested information. This makes the form easier to read for tax officials and helps avoid processing delays caused by illegible handwriting.

- Do verify the accuracy of all identification numbers provided, including the West Virginia Identification Number, Federal Identification Number, and Social Security Numbers. Errors in these fields can lead to unnecessary complications.

- Do check the appropriate box to indicate the type of organization and type of nonresident, as this information is crucial for proper tax treatment.

- Do ensure that the nonresident signing the form includes a signature, prints their name above the signature, provides a differing mailing address if applicable, and dates the form accurately.

- Don't leave any required fields blank. Incomplete forms may be returned or may delay processing times.

- Don't file the form late. It should be submitted to the organization before or by the last day of the organization’s taxable year to avoid West Virginia income tax withholding.

Remember, filling out the WV/NRW-4 form accurately and on time is important for any nonresident looking to avoid withholding of West Virginia source income. Taking the time to follow these guidelines can streamline the process, ensuring compliance with West Virginia's tax laws.

Misconceptions

Understanding the WV/NRW-4 form can often lead to confusion. Here are five common misconceptions about this form and the truths behind them:

- Only individuals need to file the WV/NRW-4. Actually, both individuals and C corporations that are nonresidents but earn income from a West Virginia source through a partnership, S corporation, estate, trust, or LLC must file this form. The key is having West Virginia source income, regardless of the entity type.

- Filing the WV/NRW-4 exempts you from all WV state taxes. The truth is that by filing WV/NRW-4, nonresidents agree to file West Virginia state income tax returns and pay any taxes due on West Virginia source income. The form simply allows income to be reported and taxed directly to the nonresident, avoiding withholding at the source.

- The WV/NRW-4 needs to be filed annually. Once filed, the WV/NRW-4 remains effective until the nonresident or the Tax Commissioner revokes it. It's not an annual filing requirement but rather a one-time submission that continues to apply until formally revoked.

- Any nonresident can file the WV/NRW-4 to stop withholdings on all their income. This form specifically relates to income from pass-through entities like partnerships, S corporations, estates, trusts, or LLCs. It does not apply to wages or salaries earned from employment in West Virginia, which are subject to separate withholding requirements.

- If the form is not filed on time, there are no options to avoid withholding. While the form must ideally be filed before the last day of the organization’s taxable year to avoid withholding for that year, nonresidents can still file the form for subsequent years to stop future withholdings. Plus, the withheld amount acts as a credit against the income tax liability when filing the state return.

Understanding these aspects of the WV/NRW-4 can help ensure that nonresidents comply with West Virginia’s tax regulations while optimizing their tax liabilities.

Key takeaways

Understanding the West Virginia Nonresident Income Tax Agreement (WV/NRW-4 form) is crucial for nonresidents who earn income from sources within the state and wish to avoid automatic withholding of state income taxes. Here are seven key takeaways to guide you through the process:

- Filing this form allows nonresident individuals and entities, such as C corporations, that earn income through organizations like partnerships, S corporations, estates, trusts, or limited liability companies in West Virginia, to not have West Virginia income tax withheld by those organizations.

- The form must be completed and filed with the relevant organization or entities from which the nonresident earns income before the last day of the organization's taxable year to prevent income tax withholding.

- If a nonresident is receiving West Virginia source income from more than one organization, they must file a separate WV/NRW-4 form with each organization to ensure withholding is not applied.

- Upon filing, the form ensures that the organization will not withhold West Virginia income tax from distributions (actual or deemed) made to the nonresident. The organization is then required to attach a copy of the agreement to its West Virginia income tax return.

- Once filed, the agreement remains in effect for all succeeding taxable years and applies starting with the taxable year during which the organization receives the properly executed form from the nonresident.

- A nonresident can revoke this agreement at any time by submitting a new form indicating the revocation. The revocation will apply to taxable years of the organization that begin after the revocation notice is filed.

- The Tax Commissioner has the authority to revoke this agreement if the nonresident fails to file a West Virginia income tax return or to pay any tax due within 60 days of the return’s due date (including extensions), for any taxable year covered by the agreement.

Completing and submitting the WV/NRW-4 form is thus an essential step for nonresidents with West Virginia source income who wish to manage their tax obligations proactively. Complying with these stipulations ensures that nonresidents can avoid unnecessary withholding and can streamline their tax reporting and payment responsibilities in West Virginia.

Popular PDF Forms

Wv Sales and Use Tax Form - By outlining specific steps and documentation, the WV/CST-AF2 form aids in mitigating errors in tax refund or credit claims for businesses.

How to Become a Resident of West Virginia - Inclusion of a perjury statement ensures the integrity of the information submitted, emphasizing the serious legal obligation of the employer in the reporting process.

Wv Division of Forestry - Part of a statewide initiative to ensure that loggers are equipped with the necessary skills and knowledge for sustainable operations.