Free Wv Spf 100 Form

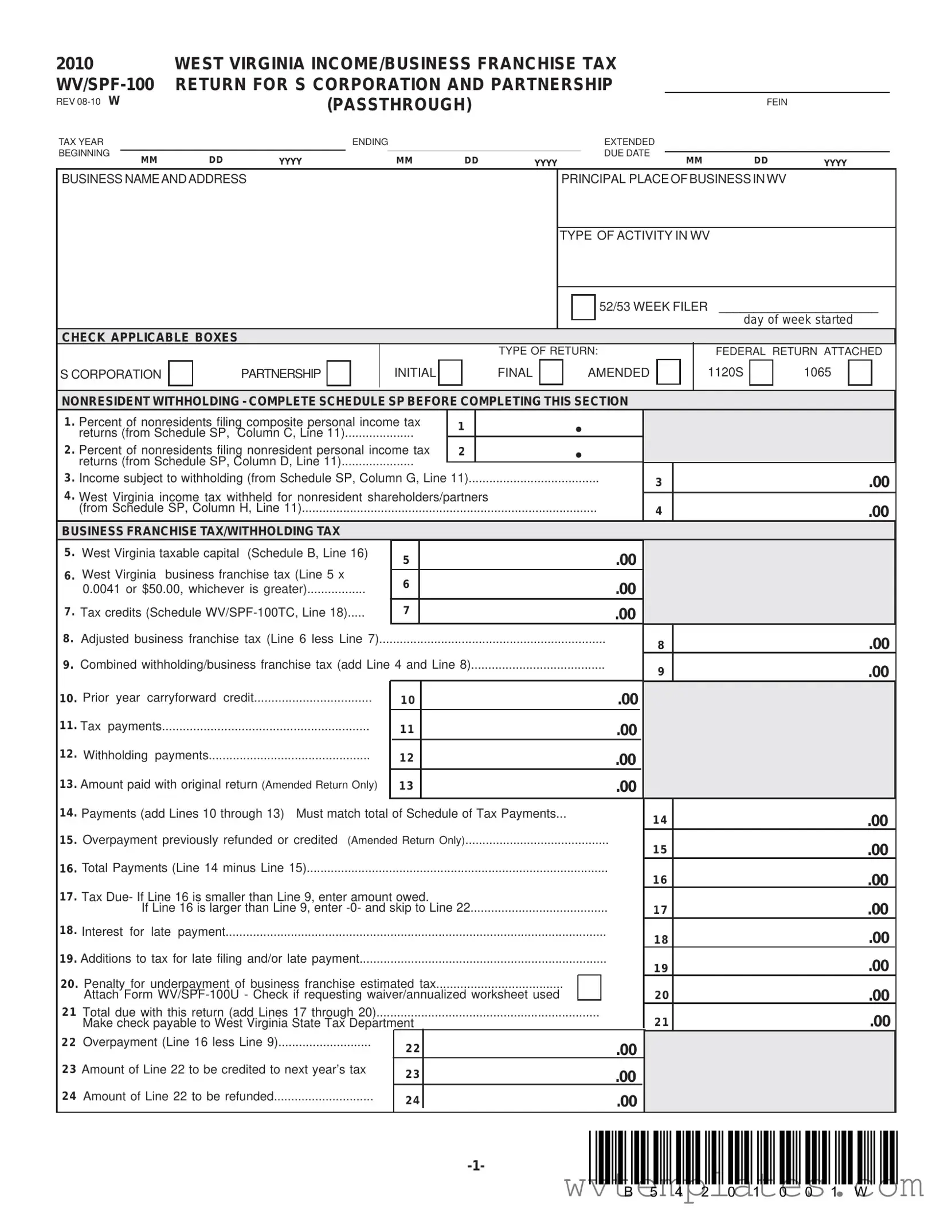

Navigating the complexities of tax documentation can often feel like an insurmountable challenge, particularly when dealing with nuanced forms like the WV SPF-100. Designed specifically for S corporations and partnerships operating within West Virginia, this form encapsulates the essential details required for filing income and business franchise taxes effectively for the tax year 2010. It outlines various critical sections including business and personal information, details regarding the business's operations in West Virginia, and specific financial metrics crucial for accurate tax calculation. This extended document meticulously guides entities through reporting their income or loss, modifications to federal income, and apportionment factors, ensuring a comprehensive overview of their fiscal responsibilities to the state. Additionally, it mandates the disclosure of adjustments to federal S corporation and partnership income, catering to an exhaustive approach towards taxable income calculation. Entities are required to report their West Virginia taxable capital and calculate the respective business franchise tax due, integrating allowances for certain obligations and investments. Furthermore, the form provides a realm for reporting tax credits, underscoring West Virginia’s efforts to accommodate business growth and sustainability within its jurisdiction. A notable feature includes the provision for direct deposit of refunds, simplifying the reimbursement process for overpaid taxes. By signing the form, the responsible officer or partner attests to the completeness and accuracy of the information, underscoring the legal implications of the document. The WV SPF-100 form, thus, stands as a testament to the intricate balance between regulatory compliance and the sustenance of commercial endeavors in West Virginia.

Wv Spf 100 Example

2010 |

|

WEST VIRGINIA INCOME/BUSINESS FRANCHISE TAX |

|

|

||||||||

|

|

|||||||||||

REV |

|

|

(PASSTHROUGH) |

|

|

|

FEIN |

|

||||

TAX YEAR |

|

|

|

ENDING |

|

|

EXTENDED |

|

|

|||

BEGINNING |

|

|

|

|

|

|

|

|

DUE DATE |

|

|

|

MM |

DD |

YYYY |

|

|

MM |

DD |

YYYY |

MM |

DD |

YYYY |

||

|

|

|

|

|||||||||

BUSINESS NAME AND ADDRESS

PRINCIPAL PLACE OF BUSINESS IN WV

TYPE OF ACTIVITY IN WV

52/53 WEEK FILER _______________________

day of week started

CHECK APPLICABLE BOXES

S CORPORATION

PARTNERSHIP

INITIAL

TYPE OF RETURN:

FINAL |

|

AMENDED |

|

|

|

FEDERAL RETURN ATTACHED

1120S |

|

1065 |

|

|

|

NONRESIDENT WITHHOLDING - COMPLETE SCHEDULE SP BEFORE COMPLETING THIS SECTION

1 |

. Percent of nonresidents filing composite personal income tax |

1 |

|

• |

|

|||

|

|

returns (from Schedule SP, Column C, Line 11) |

|

|

|

|

||

|

|

|

|

|

|

|

||

2 |

. Percent of nonresidents filing nonresident personal income tax |

2 |

|

• |

|

|||

|

|

returns (from Schedule SP, Column D, Line 11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3 |

. Income subject to withholding (from Schedule SP, Column G, Line 11) |

3 |

||||||

4 |

. West Virginia income tax withheld for nonresident shareholders/partners |

|

||||||

|

|

|||||||

|

|

(from Schedule SP, Column H, Line 11) |

|

|

|

|

|

4 |

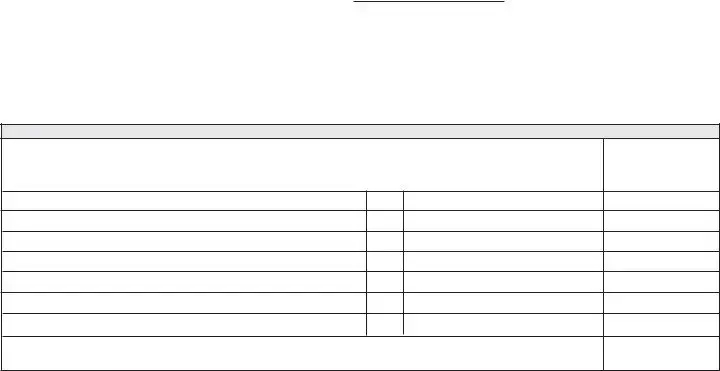

BUSINESS FRANCHISE TAX/WITHHOLDING TAX |

|

|

|

|

|

|

||

5 |

. |

West Virginia taxable capital (Schedule B, Line 16) |

5 |

|

|

|

.00 |

|

6 |

. |

|

|

|

|

|

||

West Virginia business franchise tax (Line 5 x |

6 |

|

|

|

.00 |

|

||

|

|

0.0041 or $50.00, whichever is greater) |

|

|

|

|

||

|

|

|

|

|

|

|

||

7 |

. Tax credits (Schedule |

7 |

|

|

|

.00 |

|

|

.00

.00

..................................................................8 . Adjusted business franchise tax (Line 6 less Line 7) |

|

|

|

|

|

|

|

9 . Combined withholding/business franchise tax (add Line 4 and Line 8) |

|

|

|

||||

|

|

|

|

|

|

|

|

10 |

. Prior year carryforward credit |

1 0 |

|

.00 |

|

||

11 |

. Tax payments |

1 1 |

|

.00 |

|

||

12 |

. Withholding payments |

1 2 |

|

.00 |

|

||

13 |

. Amount paid with original return (Amended Return Only) |

1 3 |

|

.00 |

|

||

|

|

|

|

|

|

|

|

14 |

. Payments (add Lines 10 through 13) Must match total of Schedule of Tax Payments... |

|

|

|

|||

15 |

. Overpayment previously refunded or credited (Amended Return Only) |

|

|

|

|||

16 |

. Total Payments (Line 14 minus Line 15) |

|

|

|

|

|

|

17 |

. Tax Due- If Line 16 is smaller than Line 9, enter amount owed. |

|

|

|

|||

|

If Line 16 is larger than Line 9, enter |

|

|

|

|||

18 |

. Interest for late payment |

|

|

|

|

|

|

19 |

. Additions to tax for late filing and/or late payment |

|

|

|

|

|

|

20. Penalty for underpayment of business franchise estimated tax |

|

|

|

||||

|

|

|

|||||

|

Attach Form |

|

|

|

|||

.................................................................2 1 Total due with this return (add Lines 17 through 20) |

|

|

|

|

|

|

|

|

Make check payable to West Virginia State Tax Department |

|

|

|

|||

...........................2 2 Overpayment (Line 16 less Line 9) |

|

2 2 |

|

.00 |

|

||

|

|

|

|

|

|||

2 3 Amount of Line 22 to be credited to next year’s tax |

|

2 3 |

|

.00 |

|

||

|

|

|

|

|

|||

.............................2 4 Amount of Line 22 to be refunded |

|

2 4 |

|

.00 |

|

||

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

8 |

.00 |

9 |

.00 |

1 4 |

.00 |

1 5 |

.00 |

1 6 |

.00 |

1 7 |

.00 |

1 8 |

.00 |

1 9 |

.00 |

2 0 |

.00 |

2 1 |

.00 |

REV |

RETURN FOR S CORPORATION AND PARTNERSHIP |

SCHEDULE A - INCOME/LOSS

1 |

............................... Income/Loss: S Corporation use Federal Form 1120S; Partnership use Federal Form 1065 |

1 |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

2 |

.Other income: S Corporation use Federal Form 1120S, Schedule K and |

2 |

|||||||||||||

|

Partnership use Federal Form 1065, Schedule K and |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|||||||||

3 |

. Other expenses/deductions: S Corporation use Federal form 1120S, Schedule K; Partnership use Federal |

3 |

|||||||||||||

|

Form 1065, Schedule K |

|

|

|

|

|

|

|

|

|

|||||

4 |

. TOTAL FEDERAL INCOME: Add Lines 1 and 2 minus Line 3 - Attach federal return |

|

|

4 |

|||||||||||

5 |

. Net modifications to federal income (from Schedule |

5 |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

6 |

. Modified federal income (sum of Lines 4 and 5). Wholly WV business go to Line 12; Multistate Corporation |

6 |

|||||||||||||

|

go to Line 7. Modified federal Partnership income (sum of Lines 4 and 5), go to Line 8 |

|

............................. |

||||||||||||

7 |

.Total nonbusiness income allocated everywhere: S CORPORATION ONLY use Form |

7 |

|||||||||||||

|

Schedule A1, Column 3, Line 8 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

||||||||

8 |

. Income subject to apportionment (Line 6 less Line 7) |

|

|

|

|

|

|

8 |

|||||||

9 |

. West Virginia apportionment factor: (Round to 6 decimal places) from |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

||||||||

|

|

9 |

|

• |

|

|

|||||||||

|

or Part 3, Column 3; Partnership use Schedule B, Line 8 |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|||||||||

10 |

. West Virginia apportioned income (Line 8 multiplied by Line 9) If Line 10 shows a loss, omit Page 1, |

|

|||||||||||||

|

Lines 1 through 4. However you must complete Schedule SP. S Corporations complete Lines 11 and 12 |

1 0 |

|||||||||||||

11 |

. Nonbusiness income allocated to West Virginia; S CORPORATION ONLY. Use Form |

|

|||||||||||||

|

Schedule A2, Line 12 |

|

|

|

|

|

|

|

|

1 1 |

|||||

12 |

. West Virginia income (wholly WV |

|

|||||||||||||

|

If Line 12 shows a loss, omit Page 1, Lines 1 through 4. However, you must complete Schedule SP |

1 2 |

|||||||||||||

SCHEDULE |

|

|

|

|

|

|

|

||||||||

INCREASING |

|

|

|

|

|

|

|

|

|

|

1 3 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

13 |

. Interest income from obligations or securities of any state, or political subdivision other than this state |

||||||||||||||

|

|||||||||||||||

14 |

. US Government obligation interest or dividends exempt from federal but not exempt from state tax, less |

1 4 |

|||||||||||||

|

related expenses not deducted on federal return |

|

|

|

|

|

|

|

|||||||

15 |

. Interest expenses deducted on your federal return on indebtedness to purchase or carry |

securities |

1 5 |

||||||||||||

|

exempt from West Virginia income tax |

|

|

|

|

|

|

|

|||||||

16 |

. Total increasing modifications - Add Lines 13 through 15 |

|

|

|

|

|

|

1 6 |

|||||||

DECREASING |

|

|

|

|

|

|

|

|

|

|

|

||||

17 |

. Interest or dividends from US government obligations, included on your federal return |

|

|

1 7 |

|||||||||||

18 |

. US Government obligation interest or dividends subject to federal but exempt from state tax, less related |

1 8 |

|||||||||||||

|

expenses |

deducted on your federal return |

|

|

|

|

|

|

|||||||

19 |

. Refund or credit of income taxes or taxes based upon income, imposed by this state or any other jurisdiction, |

1 9 |

|||||||||||||

|

included |

on your federal |

return |

|

|

|

|

|

|

||||||

20 |

. Total decreasing modifications - Add Lines 17 through 19 |

|

|

|

|

|

|

2 0 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

NET |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

21 |

. Net modifications to federal partnership income - Line 16 less Line 20. |

Enter here and on Schedule A, Line 5 |

2 1 |

||||||||||||

|

|

|

|

TYPE |

|

|

|

|

|

|

|

|

|

|

|

DIRECT |

|

|

CHECKING |

ROUTING |

|

|

ACCOUNT |

|

|

|

|

||||

DEPOSIT |

|

|

|

NUMBER |

|

|

|

|

|

|

|||||

|

|

|

|

|

NUMBER |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||||

OF REFUND |

|

|

SAVINGS |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

Under penalties of perjury, I declare that I have examined this return (including accompanying schedules and statements) and to the best of my knowledge and belief it is true and complete. All appropriate sections of the return must be completed. An incomplete return will not be accepted as timely filed. Checking this box indicates waiver of my/our rights of confidentiality for the purpose of contacting the preparer regarding this return.

Signature of Officer/Partner or Member |

Name of Officer/Partner or |

Title |

Date |

Business Phone Number |

|

|

|

|

|

|

|

|

|

|

Paid preparer's signature |

Firm's name and address |

MAIL TO:

WEST VIRGINIA STATE TAX DEPARTMENT

TAX ACCOUNT ADMINISTRATION DIVISION

PO BOX 11751

CHARLESTON, WV

Date |

Preparer phone number |

*b54201002W*

REV |

RETURN FOR S CORPORATION AND PARTNERSHIP |

|

SCHEDULE

FEIN

S CORPORATION INCOME TAX - CALCULATION OF WEST VIRGINIA TAXABLE INCOME

1.Interest or dividends from any state or local bonds or securities..............................................

2.U.S. Government obligation interest or dividends not exempt from state tax, less related expenses not deducted on federal return................................................................................

3.Income taxes or taxes based upon net income, imposed by this state or any other jurisdiction, deducted on your federal return...............................................................................................

4.Federal depreciation/amortization for WV water/air pollution control facilities -

wholly WV corporations only....................................................................................................

5. Unrelated business taxable income of a corporation exempt from federal tax (IRC 512)..........

6. Federal net operating loss deduction..........................................................................................

7. Federal deduction for charitable contributions to Neighborhood Investment Programs if

claiming the WV Neighborhood Investment Programs Tax credit.............................................

8. Net operating loss from sources outside the United States........................................................

9. Foreign taxes deducted on your federal return.........................................................................

10. Deduction taken under IRC 199 (WV Code

11. Add back for expenses related to certain REIT’s and Regulated Investment

Companies (WV Code

12. TOTAL INCREASING ADJUSTMENTS - add Lines 1 through 11.......................................

13. Refund or credit of income taxes or taxes based upon net income, imposed by this state or any

other jurisdiction, included in federal taxable income..................................................................

14. Interest expense on obligations or securities of any state or its political subdivisions,

disallowed in determining federal taxable income.....................................................................

15. Salary expense not allowed on federal return due to claiming the federal jobs credit............

16. Foreign dividend

17. Subpart F income (IRC Section 951)..........................................................................................

18. Taxable income from sources outside the United States...........................................................

19. Cost of West Virginia water/air pollution control facilities - wholly WV only.............................

20. Employer contributions to medical savings accounts (WV Code

taxable income less amounts withdrawn for

21. SUBTOTAL of decreasing adjustments - add Lines 13 through 20..........................................

22. Allowance for governmental obligations/obligations secured by residential property

(from Schedule

1 |

.00 |

|

|

2 |

.00 |

|

|

3 |

.00 |

|

|

4 |

.00 |

|

|

5 |

.00 |

6 |

.00 |

7 |

.00 |

8 |

.00 |

|

|

9 |

.00 |

|

|

10 |

.00 |

|

|

11 |

.00 |

12 |

.00 |

13 |

.00 |

14 |

.00 |

15 |

.00 |

16 |

.00 |

17 |

.00 |

18 |

.00 |

19 |

.00 |

20 |

.00 |

21 |

.00 |

22 |

.00 |

*b54201003W*

2010 |

|

|

||||||||

REV |

RETURN FOR S CORPORATION AND PARTNERSHIP |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEIN |

|

23. TOTAL DECREASING ADJUSTMENTS - add Lines 21 and 22 |

|

22 |

.00 |

|||||||

24. Net modifications to Federal S Corporation Income - Line 12 less Line 23. Enter here and |

|

|

|

.00 |

||||||

|

on Schedule A, Line 5 |

|

|

|

|

23 |

||||

|

|

|

|

|

|

|||||

SCHEDULE |

BY |

RESIDENTIAL PROPERTY |

||||||||

|

|

|

|

|

|

|

|

|

||

1. |

Federal obligations and securities |

|

|

|

|

1 |

|

.00 |

||

2. |

Obligations of WV and any political subdivision of WV |

|

|

............... |

|

2 |

|

.00 |

||

3. |

Investments or loans primarily secured by mortgages or deeds of trust on residential property |

|

|

|

|

|

||||

|

|

|

.00 |

|||||||

|

located in WV |

|

|

|

|

3 |

|

|||

4. |

Loans primarily secured by a lien or security agreement on a mobile home or |

|

|

|

|

|

||||

|

located in WV |

|

|

|

|

4 |

|

.00 |

||

5. |

......................................................................................................TOTAL - add Lines 1 through 4 |

|

|

|

|

5 |

|

.00 |

||

|

|

|

|

|

|

|

|

|||

6. |

........................................................Total assets as shown on Schedule L, Federal Form 1120S |

|

|

|

|

6 |

|

.00 |

||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

COMPLETED SCHEDULE B |

|

7. |

Line 5 divided by Line 6 (round to six (6) decimal places) |

7 |

|

• |

|

|

|

MUST BE ATTACHED |

||

|

|

|

|

|

|

|

|

|

|

|

8. |

Adjusted income - Add Schedule A, Line 4 and Schedule |

|

|

|

|

|

||||

|

21 plus total from Form |

|

8 |

|

.00 |

|||||

9. |

ALLOWANCE - Line 7 x Line 8, disregard sign - enter here and on Schedule |

|

9 |

|

.00 |

|||||

SCHEDULE OF TAX PAYMENTS

|

Identification Number |

MM |

DD YEAR |

Indicate EFTif |

Type: withholding, |

|

year credit |

||||

Name of business |

West Virginia Account |

|

Date of Payment |

|

estimated,extension, |

|

|

other pmts or prior |

|||

|

|

|

|

|

|

TOTAL - This amount must agree with the amount on Line 14, on front of return........................................................

Amount of payment

.00

.00

.00

.00

.00

.00

.00

.00

*b54201004W*

|

|

RETURN FOR S CORPORATION AND PARTNERSHIP |

FEIN |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE B - BUSINESS FRANCHISE TAX - CALCULATION OF WEST VIRGINIA TAXABLE CAPITAL |

|

||||||||||

|

|

|

|

|

Column 1 |

|

|

|

Column 2 |

|

Column 3 - Average |

|

|

|

|

|

|

Beginning Balance |

|

|

|

Ending Balance |

|

(Col 1 + Col 2) divided by 2 |

|

|

1. Dollar amount of common stock & preferred stock |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

2. |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

3. Retained earnings appropriated & unappropriated |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|||

|

4. Adjustments to shareholders equity |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

5. Shareholders undistributed taxable income |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

6. Accumulated adjustments account |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

7. Other adjustments account |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

...................8. Add Lines 1 through 7 of Column 3 |

|

|

|

|

|

|

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. Less: Cost of Treasury Stock |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

10. Dollar amount of partner’s capital accounts |

|

.00 |

|

|

|

.00 |

.00 |

|

|||

|

11. Capital - Column 3, Line 8 less Column 3, Line 9 |

|

|

|

|

|

|

.00 |

|

|||

|

12. Multiplier for allowance for certain obligations/investments - |

|

• |

|

|

|

|

|||||

|

Schedule |

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

.00 |

|

||||

|

13. Allowance - Line 10 or 11 multiplied by Line 12 |

|

|

|

|

|

|

|

||||

|

14. Adjusted capital - subtract Line 13 from Line 10, or 11. If taxable only in West Virginia check here |

|

.00 |

|

||||||||

|

and enter this amount on Line 16 |

|

|

|

|

|

|

|

||||

|

15. Apportionment factor - Form |

|

• |

|

|

COMPLETED FORM |

|

|||||

|

Part 3, Column 3 |

|

|

|

|

MUST BE ATTACHED |

|

|||||

|

16. TAXABLE CAPITAL - Line 14 multiplied by Line 15 - Enter on front of return, Line 5 |

.00 |

|

|||||||||

|

BUSINESS FRANCHISE TAX - SUBSIDIARY CREDIT |

|

|

|

|

|

|

|

||||

|

|

Column 1 |

|

Column 2 |

|

|

|

Column 3 |

Column 4 |

|||

|

|

Account number and name |

|

Recomputed Business |

|

Percentage |

Allowable Credit |

|||||

|

|

of Subsidiary or Partnership |

|

Franchise Tax Liability |

|

of Ownership |

(Column 2 x Column 3) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

NAME |

|

|

.00 |

|

• |

|

.00 |

|

|||

|

FEIN |

|

|

|

|

.00 |

|

• |

|

.00 |

|

|

|

NAME |

|

|

|

|

|

||||||

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

NAME |

|

|

.00 |

|

• |

|

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

|

17. TOTAL - (Enter here and on Schedule |

.00 |

|

|||||||||

BUSINESS FRANCHISE TAX - TAX CREDIT FOR PUBLIC UTILITIES AND ELECTRIC POWER GENERATORS

18.Gross income in West Virginia subject to the STATE Business and Occupation Tax...............................................

19.Total gross income of taxpayer from all activity in West Virginia..............................................................................

20. Line 18 divided by Line 19 (Round to 6 decimal places) |

• |

21.Business Franchise liability - From front of return, Line 6, reduced by any Subsidiary Credit..................................

22.Allowable credit - Line 21 multiplied by line 20 - Enter here and on Schedule

.00

.00

.00

.00

**IMPORTANT NOTE REGARDING LINE 15**

FORM

FAILURE TO ATTACH COMPLETED FORM

WILL RESULT IN 100% APPORTIONMENT TO WEST VIRGINIA

*b54201005W*

Form Specifications

| Fact | Detail |

|---|---|

| Form Designation | WV/SPF-100 is designated for S Corporation and Partnership Income/Business Franchise Tax Return in West Virginia for the year 2010. |

| Governing Laws | This form is governed by West Virginia State Tax laws, specifically referencing West Virginia Code §§ 11-23-3(b)(2) for Business Franchise Tax and 11-24-6, 6a for S Corporation Income Tax Adjustments. |

| Key Components | Includes sections for reporting income, modifications to federal income, business franchise tax calculations, and nonresident shareholder/partner withholding tax. |

| Submission Requirements | The form requires the inclusion of federal returns (1120S for S Corporations, 1065 for Partnerships), and detailed schedules for income modifications, tax payments, and withholding details. An incomplete return will not be accepted as timely filed. |

Guide to Filling Out Wv Spf 100

Filling out the WV SPF-100 form requires thorough attention to detail and accuracy to ensure that S Corporations and Partnerships comply with the West Virginia Income and Business Franchise Tax requirements. This process involves reporting income, losses, tax withheld for nonresidents, and computing the business franchise tax. Careful preparation will ensure the company meets its tax obligations effectively.

- Begin by entering the Federal Employer Identification Number (FEIN) in the designated space.

- Fill out the tax year-end, the extended due date if applicable, and the beginning date of the fiscal year in the "MM DD YYYY" format.

- Provide the business name and address, including the principal place of business in West Virginia.

- Specify the type of activity the business conducts in West Virginia.

- Indicate if the business is a 52/53 week filer by stating the day of the week started.

- Check the applicable boxes to identify if the form is for an S Corporation or a Partnership and specify if the return is initial, final, or amended. Also, indicate if the federal return is attached.

- Complete the nonresident withholding section as per instructions, based on the information derived from Schedule SP.

- Calculate and enter the West Virginia taxable capital in the Business Franchise Tax/Withholding Tax section, and compute the West Virginia business franchise tax.

- Record any applicable tax credits, adjust the business franchise tax accordingly, and compute the combined withholding/business franchise tax.

- Detail prior year carryforward credit, tax payments, and withholding payments. If it's an amended return, indicate the amount paid with the original return.

- For amended returns, note any overpayment previously refunded or credited. Total the payments and calculate the tax due or overpayment.

- Fill out the Schedule A - Income/Loss section according to the type of entity and the awarded instructions, attaching the federal return if required.

- Complete Schedules A-1 and A-2 for modifications to Federal Partnership or S Corporation income and detail decreasing and increasing adjustments as applicable.

- For direct deposit of refund, provide the type of account, routing number, and account number.

- Review the declaration, and have an officer/partner or member sign and date the form. Provide the business's contact number.

- If a paid preparer completed the form, they should sign and provide their contact details.

- Mail the completed form and any required attachments to the West Virginia State Tax Department at the address provided in the form instructions.

Ensuring all sections of the WV SPF-100 form are correctly filled out and all necessary documents are attached is crucial for timely processing. This step-by-step guide is designed to assist S Corporations and Partnerships in navigating the filling process, contributing to the smooth handling of their tax responsibilities.

Things You Should Know About Wv Spf 100

What is the purpose of the WV SPF-100 form?

The WV SPF-100 form is designed for S Corporations and Partnerships to file their annual income and business franchise tax returns in West Virginia. It captures details about income, losses, tax deductions, and credits specific to these business entities, facilitating the accurate calculation and payment of taxes owed to the state. By reporting this financial information, businesses comply with state tax regulations and contribute to the public funding that supports state services and infrastructure.

Who needs to file the WV SPF-100 form?

S Corporations and Partnerships operating in West Virginia must file the WV SPF-100 form. This requirement applies to entities that earn income, incur losses, or conduct business activities within the state. The form serves as a comprehensive report of the business's taxable capital and income, ensuring that these entities contribute to state tax revenues according to their financial operations in West Virginia.

When is the WV SPF-100 form due?

The due date for filing the WV SPF-100 form depends on the tax year end date of the business. Generally, it is due by the 15th day of the fourth month following the close of the business's tax year. For businesses operating on a calendar year, the due date would be April 15th of the following year. Entities can request an extension if more time to file is needed, but generally must adhere to this timeline to avoid penalties.

What information is needed to complete the WV SPF-100 form?

To accurately complete the WV SPF-100 form, S Corporations and Partnerships need to provide their Federal Employer Identification Number (FEIN), tax year information, business name and address, along with detailed financial data. This includes their total income or loss as reported on federal forms 1120S or 1065, modifications to federal taxable income specific to West Virginia, business franchise tax calculations, withholding tax information for nonresident members, and any applicable tax credits. Detailed schedules within the form guide the reporting of adjustments, with a need for meticulous record-keeping to ensure precise tax liability computation.

How are modifications to federal taxable income reported on the WV SPF-100 form?

Modifications to federal taxable income on the WV SPF-100 form include adjustments specific to West Virginia tax laws. These modifications can be either increases or decreases to the income reported on federal tax returns. Increases may include items like interest income from non-West Virginia state obligations, dividends exempt from federal tax but not state, and other specified add-backs. Decreases can include interest from U.S. government obligations, state or local bond interest that's exempt in West Virginia, refunds of income or franchise taxes, among others. Entities must review the detailed instructions for Schedule A-1 or A-2 to accurately report these adjustments, which affect the calculation of state taxable income and ultimately, the tax due to West Virginia.

Common mistakes

Completing the WV/SPF-100 form, which pertains to West Virginia Income/Business Franchise Tax Return for S Corporation and Partnership, can be a challenging task. There are common mistakes made during the process that can affect the outcome of your tax obligations. Understanding these missteps will facilitate a smoother filing experience and potentially reduce errors that could lead to penalties.

One of the typical mistakes includes not checking the correct status box. The form requires you to mark whether you are filing as an S Corporation or a Partnership. Failing to check the appropriate box or checking the wrong one can lead to incorrect processing of your form.

Inaccurate reporting of income and deductions is another area where errors frequently occur. On Schedule A of the WV/SPF-100 form, you must report your income and deductions accurately. Misreporting can not only delay the processing of your return but also potentially trigger an audit from the state tax department.

- Not attaching the required federal return copies. Feeding into the comprehensive nature of the WV/SPF-100 form, the IRS forms 1120S or 1065 are necessary attachments. Overlooking this requirement can render your submission incomplete.

- Failing to accurately calculate and report the West Virginia taxable capital on Schedule B can also be problematic. This calculation is crucial for the business franchise tax portion and requires precise data entry.

- Misunderstanding the tax credits or deductions you’re eligible for and incorrectly filling out Schedule WV/SPF-100TC can lead to missed opportunities for reducing your tax liability.

- Inaccurate calculation of nonresident withholding sections can lead to under or overpaying tax obligations, hence why precise attention to Schedule SP is paramount.

- Direct deposit information errors can cause delays in receiving any refund owed. Ensure the routing and account numbers are accurately entered.

Other miscellaneous errors include incorrect reporting of the tax year and due dates, misunderstanding the apportionment factor instructions, and failing to sign and date the form. These minor yet significant details, if overlooked, can result in the form being returned or, worse, the imposition of penalties and interest for late filing.

Ensuring accurate completion of the WV/SPF-100 form demands a careful reading of the instructions and meticulous attention to detail. Taking the time to review your form thoroughly before submission can save you the headache of dealing with errors down the line. If unsure about how to proceed in any section, consulting with a tax professional can provide clarity and peace of mind.

Documents used along the form

The WV SPF-100 form is critical for S corporations and partnerships in West Virginia to report their income and business franchise taxes. However, this form does not work in isolation. To accurately complete the WV SPF-100, several additional documents and forms are usually needed to provide comprehensive tax information. These accompanying documents ensure compliance with tax regulations and help in detailed financial reporting.

- Federal Form 1120S - This form is used by S corporations to report their income, gains, losses, deductions, credits, and other information to the federal government.

- Federal Form 1065 - Required for partnerships, this form is used to report the income, deductions, gains, losses, etc., of a partnership business to the IRS.

- Form WV/SPF-100APT - A form specifically for apportioning income among various states. It is essential for S corporations and partnerships operating in multiple states.

- Form WV/SPF-100TC - This form is used to claim tax credits that can reduce the amount of business franchise tax payable by the corporation or partnership.

- Form WV/SPF-100U - Utilized for calculating underpayment of estimated business franchise tax and any associated penalties.

- Schedule SP - A schedule for nonresident withholding information, necessary for S corporations and partnerships with nonresident members.

- Schedule A-1 and A-2 - These schedules are used for modifications to federal income for partnerships and S corporations respectively, adjusting specific items for West Virginia tax purposes.

- Schedule A-3 - Allows for adjustments based on government obligations or obligations secured by residential property in West Virginia.

- Schedule L (Federal Form 1120S) - A balance sheet form that provides information on the corporation's assets, liabilities, and equity at the beginning and end of the year.

- Schedule B - Part of the WV SPF-100 package, this schedule is used for calculating West Virginia taxable capital for business franchise tax purposes.

Each of these documents plays a critical role in the preparation and completion of the WV SPF-100 form. Properly filled and submitted, they provide the West Virginia State Tax Department with a detailed and accurate account of an entity's financial dealings within the state. This guarantees a fair tax assessment and fulfills legal obligations under state and federal law.

Similar forms

The Internal Revenue Service (IRS) Form 1120S closely resembles the WV/SPF-100 form as it serves as the U.S. Income Tax Return for an S Corporation. Both documents are intended for entities that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. The IRS Form 1120S is required at the federal level, while the WV/SPF-100 form addresses the specific reporting requirements for S Corporations and Partnerships in West Virginia, emphasizing state tax obligations and adjustments connected to federal taxable income.

Another similar document is the IRS Form 1065, U.S. Return of Partnership Income. This form is akin to the WV/SPF-100 in its purpose for partnerships, outlining the income, gains, losses, deductions, and credits of the business. Both forms are essential for reporting the financial standings of pass-through entities like partnerships and S corporations, designed to detail the distributive shares of each entity's income, which are then reported by the partners or shareholders on their personal tax returns.

Form WV/SPF-100TC, mentioned within the WV/SPF-100 document, is for detailing tax credits that S corporations and partnerships might claim to lower their business franchise tax or income tax obligations in West Virginia. The concept of this form parallels the various federal tax credit forms such as Form 3800, General Business Credit. Both types of forms are instrumental in calculating credits that apply to a business entity, albeit on different tax jurisdiction levels (state vs. federal), thereby affecting the overall tax liabilities.

The Schedule K-1 forms, both for IRS Form 1120S and IRS Form 1065, share similarities with portions of the WV/SPF-100. These schedules report each shareholder's or partner's share of income, deductions, credits, etc., from the entity. The documented information on Schedule K-1 is used by shareholders or partners to complete their own tax returns and is mirrored in the flow-through reporting process highlighted in the WV/SPF-100, where pass-through entities allocate the tax responsibilities to their members accordingly.

Form WV/SPF-100APT, as required within the WV/SPF-100 instructions, is designed for apportioning multi-state business income for S corporations and partnerships in West Virginia. It is similar to Form apportionment schedules used in other states where businesses operate in multiple jurisdictions. This form allows entities to calculate the portion of income attributable to West Virginia, paralleling the objective of other state-specific forms that seek to fairly distribute tax obligations based on the location of business operation and income generation.

Form WV/SPF-100U, tied to the WV/SPF-100, is for computing underpayment of estimated business franchise tax. It serves a similar purpose to the IRS Form 2210, Underpayment of Estimated Tax by Individuals, Estates, and Trusts, which calculates penalties for underpayments. Although these documents cater to different types of taxpayers (individuals versus businesses) and tax authorities (federal versus state), both are critical in identifying and correcting discrepancies in tax payments anticipated during a tax period.

Lastly, the Schedule of Tax Payments section of the WV/SPF-100 resembles federal payment vouchers, such as the 1040-ES vouchers used by individuals to submit estimated tax payments. Both the Schedule of Tax Payments and the 1040-ES vouchers facilitate the organized submission of tax payments during the year, ensuring taxpayers or entities comply with regulations regarding payment timelines and avoid potential underpayment penalties.

Dos and Don'ts

Filling out the WV SPF-100 form, which is essential for S Corporations and Partnerships in West Virginia, requires attention to detail and understanding of your business's finances. Here are eight dos and don'ts to help you navigate the process successfully:

- Do ensure all the information is accurate before submitting. Mistakes can cause delays or adjustments in your tax obligations.

- Don't rush through filling out the form. Take your time to understand each section and what is required.

- Do use the correct tax year dates. This includes the beginning, ending, and due dates for the tax year you are reporting.

- Don't leave sections blank if they apply to your business. Not completing applicable sections can lead to incomplete filing status.

- Do attach the federal return if indicated. For S Corporations, attach Form 1120S; for Partnerships, attach Form 1065.

- Don't guess on figures. Use your financial records to fill out income, adjustments, and tax calculations accurately.

- Do take advantage of direct deposit for refunds by accurately filling out your bank's routing and account numbers.

- Don't forget to sign the form. An unsigned form is not valid and will not be processed, possibly leading to penalties.

By following these dos and don'ts, you can ensure a smoother process for filing your WV SPF-100 form, avoid common mistakes, and meet your tax obligations with confidence.

Misconceptions

When it comes to tax forms like the WV/SPF-100, used by S corporations and partnerships in West Virginia for income and business franchise tax reporting, misconceptions abound. Let’s clarify four common misunderstandings:

- It’s only for S corporations: One common misconception is that the WV/SPF-100 form is exclusively for S corporations. While it's true that S corporations use this form, it's equally important for partnerships. Both types of entities must navigate this document to accurately report and calculate their respective tax obligations, ensuring they comply with state tax regulations.

- The form is self-explanatory: Another myth is that completing the WV/SPF-100 form is straightforward and doesn't require a deep understanding of tax laws. In reality, the form requires detailed financial information, understanding of specific tax laws, and careful calculation of taxable income, modifications, and credits. Misinterpreting the requirements can lead to errors with significant implications, making it advisable for taxpayers to seek expert guidance or thorough review of instructions.

- No need to attach the federal return: A common misunderstanding is that there’s no requirement to attach one's federal tax return when submitting the WV/SPF-100. However, the form explicitly requires attaching the federal return. For S corporations, this would be form 1120S, and for partnerships, form 1065. Including these federal documents is vital, as it provides a baseline for the state to verify income, deductions, and credits reported on the WV/SPF-100.

- Nonresident withholding isn’t mandatory: There's a mistaken belief that nonresident withholding details are optional or applicable to a subset of businesses. In truth, this section is compulsory for entities with nonresident members and involves calculating the income subject to withholding, along with the actual withholding amounts. This ensures that nonresident members are meeting their state tax obligations, safeguarding the business from potential penalties.

By debunking these misconceptions, entities operating as S corporations or partnerships in West Virginia can approach their WV/SPF-100 form with the knowledge and attention it demands. Optimally handling this crucial document not only ensures compliance with tax laws but also positions businesses for a smoother tax process. When in doubt, consulting a tax professional can provide clarity and confidence in fulfilling one’s tax responsibilities accurately.

Key takeaways

When filling out the WV SPF-100 form for either an S Corporation or Partnership in West Virginia, there are several key takeaways to keep in mind to ensure accuracy and compliance:

- Correct identification and tax year dates are crucial, including the Federal Employer Identification Number (FEIN), and the beginning and ending dates of the tax year.

- Proper selection of the entity type (S Corporation or Partnership) and specifying the type of return (initial, final, or amended) at the outset is important.

- Understanding the specifics around nonresident withholding tax obligations is necessary, particularly for entities with nonresident members, involving completing Schedule SP accurately.

- The calculation of the West Virginia taxable capital for business franchise tax purposes involves detailed financial information including stock amounts, capital surplus, and retained earnings.

- Attachments are often required, including federal return documents, Schedule B for Business Franchise Tax calculation, and potentially other schedules for accurate reporting of income, modifications, and tax credits.

- Knowing when and how to apply tax payments and credits against the calculated tax, including withholding for nonresidents, business franchise tax, tax credits, and any payments made towards the estimated tax.

Ensuring all sections of the WV SPF-100 are completed thoroughly and accurately can prevent processing delays or errors in tax calculations. Moreover, companies must attach all required documents and schedules to support their tax return information.

The declaration under penalties of perjury at the end of the form emphasizes the need for honesty and completeness in the submission. Additionally, opting for direct deposit for any refund requires careful input of banking details to avoid transaction issues.

Lastly, it is important for S Corporations and Partnerships to remain aware of the deadlines and ensure timely filing to avoid any late filing penalties, interest, or fines.

Popular PDF Forms

Wv Sales and Use Tax Form - Businesses must use the WV/CST-AF2 to assert claims for mistaken tax payments specific to Consumers Sales and Service or Use Tax, distinct from other tax types.

Courtswv - Encourages the employment of veterans by providing tax credits to West Virginia employers, as facilitated by the MIP-31 form.